Market Overview

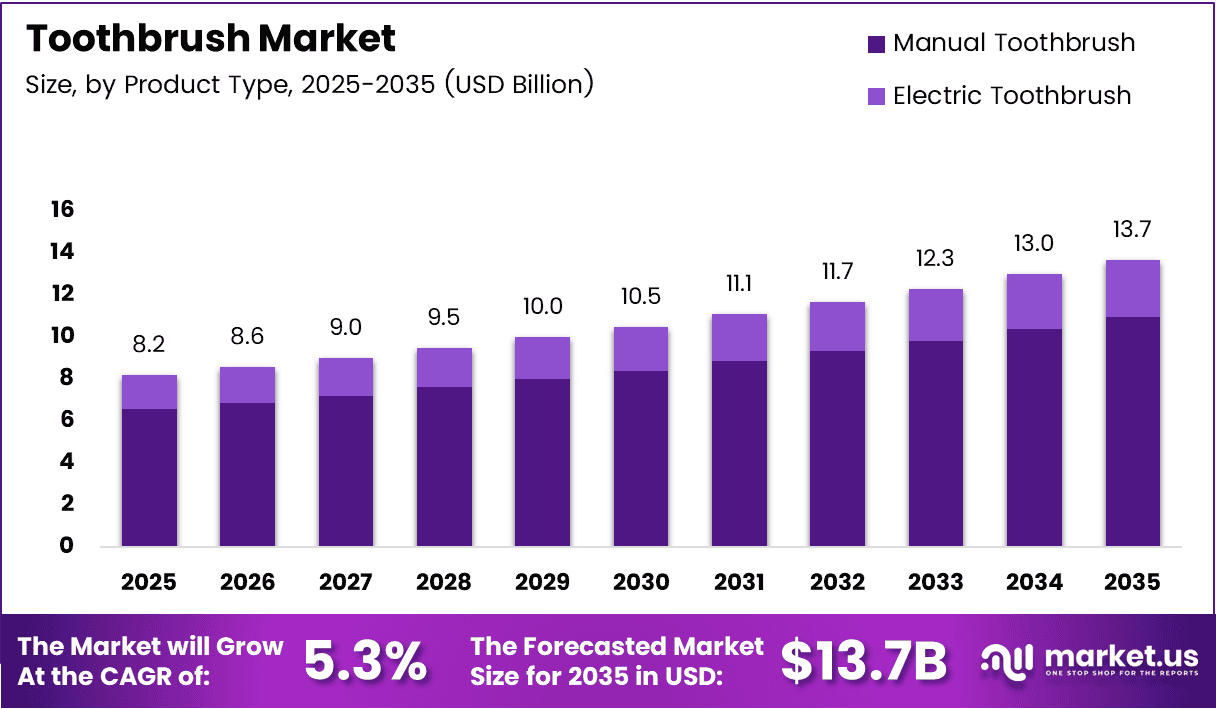

The global toothbrush market is valued at USD 8.2 billion in 2025. Forecasts indicate the market will reach USD 13.7 billion by 2035. This expansion represents a compound annual growth rate (CAGR) of 5.3% during the forecast period from 2026 to 2035. Manufacturers and retailers across the oral care industry drive this steady value growth.

A toothbrush serves as the primary tool for personal oral hygiene maintenance. Consumers use these devices daily to remove dental plaque and prevent gum disease. The product range includes manual brushes, electric toothbrushes, and app-connected smart devices sold through pharmacy, retail, and online channels worldwide. This variety supports diverse consumer needs across all income levels.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Preventive dental care drives consistent repurchase demand across all geographies. Public health guidance from leading health authorities reinforces daily brushing as the baseline standard of oral hygiene. Moreover, this institutional backing creates a structural demand floor that few consumer product categories can match. Consequently, the toothbrush market remains relatively resilient to economic downturns.

Technology improvements transform how consumers interact with oral care products. Electric and smart toothbrushes integrate pressure sensors, timers, and Bluetooth connectivity to provide real-time brushing feedback. Furthermore, artificial intelligence powers personalized coaching through mobile applications. These innovations upgrade the user experience from a routine task to an outcome-driven health behavior.

Regulations also enable market growth by setting safety and efficacy standards for oral care devices. Health authorities worldwide mandate quality controls for bristle materials, electronic components, and battery safety in electric models. Additionally, environmental regulations push manufacturers toward sustainable material sourcing and reduced plastic packaging. These requirements shape product development priorities across all price tiers.

According to the Centers for Disease Control and Prevention, brushing twice daily with fluoride toothpaste prevents cavities and gum disease. According to the American Dental Association, consumers must replace toothbrushes every 3 to 4 months due to bristle wear. These clinical guidelines translate directly into predictable household purchase patterns. Consequently, brands that align product messaging with clinical authority gain meaningful credibility advantages.

Key Takeaways

- The global toothbrush market is valued at USD 8.2 Billion in 2025.

- Market revenue is forecast to reach USD 13.7 Billion by 2035.

- The market expands at a CAGR of 5.3% during 2026 to 2035.

- Manual Toothbrush leads the product segment with a 79.5% share in 2025.

- Soft bristle toothbrushes dominate the bristle type segment with 63.6% share.

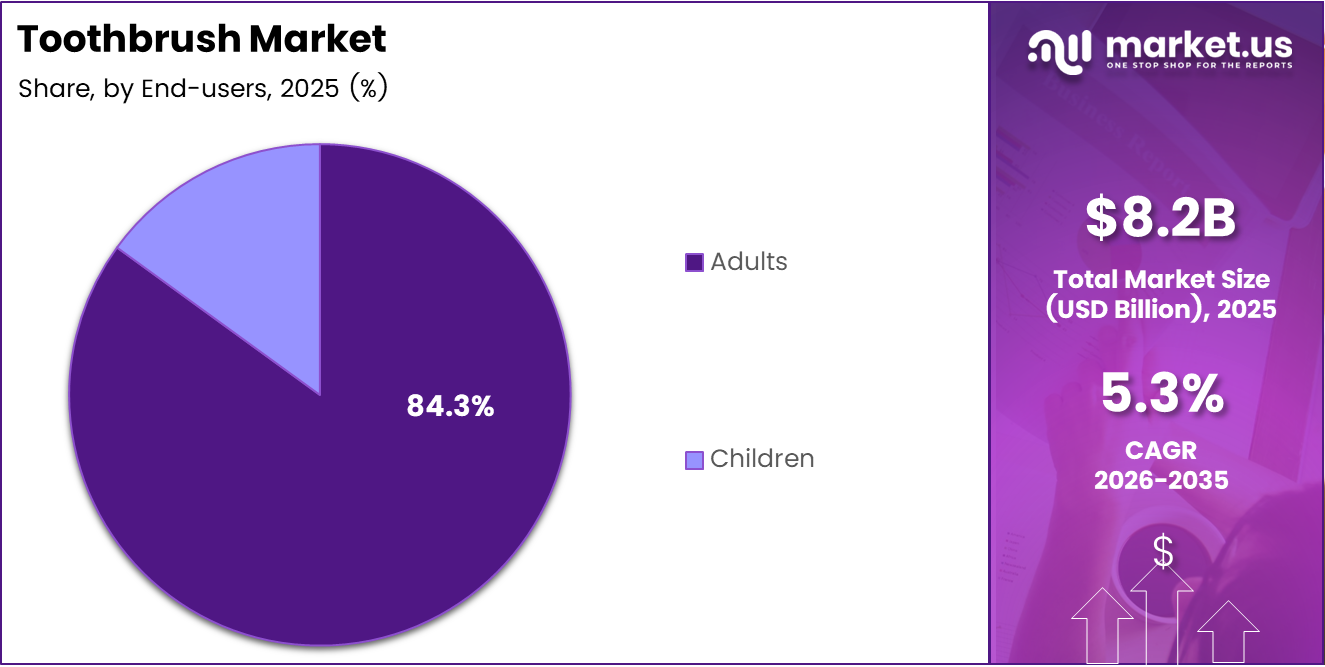

- Adults account for 84.3% of total end-user demand in 2025.

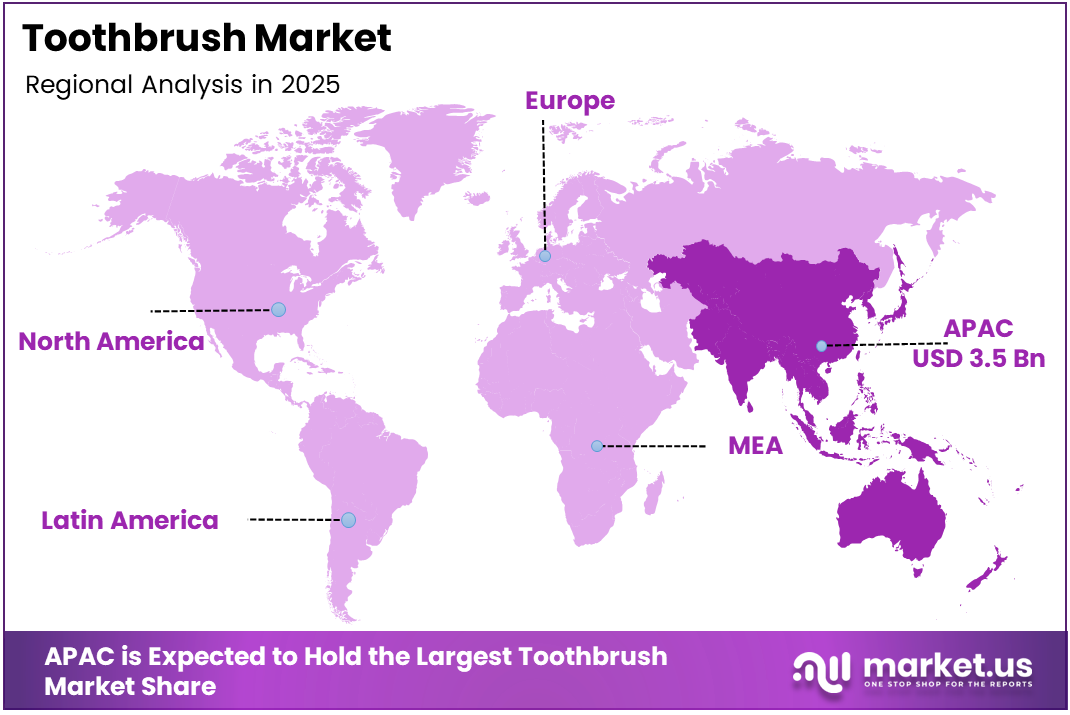

- Asia Pacific leads all regions with a 43.70% market share valued at USD 3.5 Billion.

Market Segmentation Overview

Product Type Analysis: Manual Toothbrush dominates with 79.5% of the market in 2025. This dominance reflects universal price accessibility and retail availability across all geographies. According to a cross-sectional oral hygiene survey of 600 participants published in PMC, 89% used manual toothbrushes. This near-universal reliance confirms that manual brushes will retain volume leadership even as electric penetration rises.

Electric Toothbrush carries the highest margin within the product segment. It serves as the primary premiumization lever for oral care brands. According to the UK Government’s Adult Oral Health Survey 2023, 51% of adults in England reported using an electric toothbrush while 60% used a manual brush. This overlap suggests electric brushes supplement rather than replace manual ones, effectively expanding household spend rather than displacing it.

Bristle Type Analysis: Soft Bristle holds a dominant 63.6% market share in 2025. Dental professionals consistently recommend soft bristles to prevent enamel abrasion and gum damage. This professional alignment drives purchase decisions at the point of sale, particularly among health-conscious adult buyers who follow clinical guidance. Medium Bristle serves as a transitional choice, while Firm Bristle faces structural headwinds from clinical evidence linking high-abrasion brushes to gum recession.

End-User Analysis: Adults dominate with 84.3% of total market demand in 2025. Adults control household purchasing decisions and respond directly to dentist recommendations, clinical data, and brand positioning. Consequently, the adult segment serves as the primary battleground for electric upgrade conversion and premium bristle positioning. Children represent a strategically distinct sub-segment where parents make purchase decisions, and early brand loyalty converts directly into adult purchasing behavior.

Drivers

Preventive dental care awareness directly raises toothbrush usage frequency and shortens replacement cycles. Health authorities from the CDC to national dental associations set twice-daily brushing as the standard of care. According to the International Federation of Dental Hygienists, 96% of dental hygienists surveyed across 36 countries recommend electric toothbrushes to their patients. This near-universal professional endorsement functions as a top-of-funnel conversion engine for the premium segment.

Research published in BMC Oral Health found plaque remained on about 40% of gingival margin areas even after daily toothbrushing. This data point gives brands a scientifically grounded argument for upgrading from manual to electric devices. Moreover, e-commerce expansion and modern retail channel growth place oral care products within reach of buyer populations that previously relied on informal trade. These forces collectively broaden the addressable market for all product tiers.

Use Cases

Daily preventive oral care represents the most fundamental application for toothbrushes across all demographics. Consumers use manual and electric devices each morning and evening to remove plaque, prevent cavities, and maintain gum health. This routine creates a structural demand floor with predictable replacement cycles every three to four months. Consequently, manufacturers build subscription models around this consistent consumer behavior.

Clinical dental recovery and post-surgical care represent a specialized use case for ultra-soft and electric toothbrushes. Patients recovering from oral surgery, gum treatments, or orthodontic procedures require gentle yet effective cleaning tools that standard brushes cannot provide. Moreover, smart toothbrushes with pressure sensors help these users avoid damaging sensitive tissues. This clinical application commands premium pricing and professional channel distribution advantages.

Major Challenges

High price sensitivity in developing regions limits electric toothbrush adoption precisely where population size offers the greatest volume opportunity. Consumers in price-driven markets across Asia, Africa, and Latin America default to low-cost manual brushes. According to the UK Government’s Adult Oral Health Survey 2023, electric toothbrush use in England rises with income — from 32% in the lowest income group to 66% in the highest. This income gradient confirms that electric adoption is primarily an affordability function.

Environmental concerns around disposable plastic toothbrushes add a second layer of structural friction. Consumer pressure and tightening regulations push brands to reformulate materials and reduce plastic use. However, sustainable alternatives typically carry higher production costs, creating direct tension between affordability requirements in price-sensitive markets and sustainability demands in eco-conscious developed markets. Brands cannot close this gap through marketing alone; reformulation and pricing strategy are the only credible levers available.

Business Opportunities

Sustainable materials including bamboo and biodegradable plastics address plastic waste concerns while unlocking a premium eco-segment that commands higher margins. Brands entering this space differentiate on material sourcing and sustainability credentials rather than price competition. According to PMC, analysis of approximately 16.7 million brushing sessions recorded by connected electric toothbrushes showed gingival bleeding reports decreased from 28.8% to 17.1% within two weeks. This clinical outcome gives smart toothbrush brands measurable health proof points that justify premium pricing.

Subscription-based brush head replacement services and emerging market distribution expansion represent two additional revenue pathways with distinct economics. Subscription models convert single-transaction buyers into recurring revenue accounts. Simultaneously, organized retail and e-commerce penetration in Africa, Southeast Asia, and Latin America brings branded oral care products to buyer populations that previously had limited access to formal channel distribution. Brands that execute across both pathways simultaneously capture share from legacy competitors locked into single-channel strategies.

Regional Analysis

Asia Pacific holds 43.70% of the global toothbrush market, valued at USD 3.5 Billion in 2025. This regional dominance reflects the combined weight of China, India, Japan, and South Korea — four of the world’s most populous consumer markets. Moreover, rising urban middle-class income and expanding oral health awareness programs drive volume growth. High-volume local manufacturing further reduces distribution costs and reinforces price competitiveness across both premium and value product tiers.

Europe presents a split market pattern offering distinct opportunities. Western European countries including the UK and Germany show comparatively high electric toothbrush penetration. According to UK Government survey data, electric adoption climbs sharply with income and age, from 36% among adults aged 16–24 to 62% among those aged 65–74. Conversely, Eastern European markets remain predominantly manual. This bifurcation means Western Europe offers premium product headroom while Eastern Europe sustains volume demand for accessible manual products.

Recent Developments

- July 2024 — Quip launched the 360 Oscillating Toothbrush, its first oscillating electric model featuring a pressure sensor and replaceable brush head system, marking a strategic move into performance-oriented electric oral care.

- September 2024 — Xiaomi introduced new Mijia electric toothbrush models offering multiple brushing modes and extended battery life, reinforcing its position in Asia Pacific’s value-tier electric segment.

- January 2025 — Beurer introduced two new sonic toothbrush models, the SC 30 and SC 50, at Arab Health 2025, signaling a deliberate push to expand its oral care footprint across Middle East markets.

Conclusion

The global toothbrush market is on a steady growth trajectory from USD 8.2 billion in 2025 to USD 13.7 billion by 2035. Professional oral care mandates and rising consumer health awareness drive this expansion. Moreover, technology integration through smart sensors and AI-powered feedback creates upgrade pathways from commodity manual brushes to premium connected devices. These forces collectively raise average revenue per user across all major regions.

Manual toothbrushes maintain volume dominance with 79.5% share, while soft bristle designs lead the bristle segment at 63.6%. Asia Pacific commands regional leadership with 43.70% share valued at USD 3.5 billion. Additionally, adults represent 84.3% of end-user demand, making this demographic the primary target for electric conversion strategies. Professional endorsement and clinical data continue to shape purchasing decisions across all segments.

Companies must act on three parallel opportunities to capture maximum market value. First, develop entry-level electric products for price-sensitive emerging markets. Second, build subscription models around replacement cycles to convert transaction buyers into recurring revenue accounts. Third, invest in sustainable materials to address regulatory pressure and eco-conscious consumer demand. The toothbrush market will reach USD 13.7 billion by 2035, rewarding manufacturers that balance volume accessibility with premium innovation.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)