Market Overview

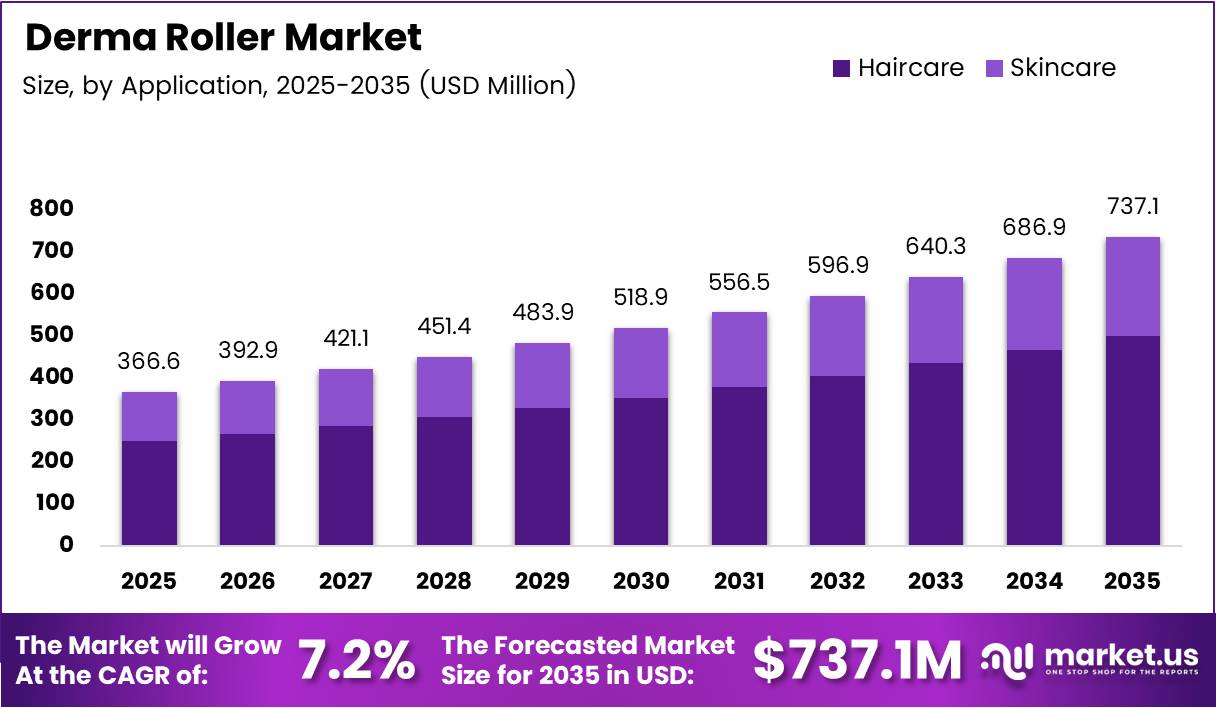

The global Derma Roller Market reached USD 366.6 million in 2025 and will hit USD 737.1 million by 2035. This growth represents a compound annual growth rate (CAGR) of 7.2% from 2026 to 2035. Rising consumer demand for non-invasive skin and hair treatments drives the market forward.

A derma roller is a handheld micro needling device with tiny needles that puncture the skin’s surface. These micro-injuries stimulate collagen production and improve absorption of serums and topical products. Both consumers and dermatologists use these tools for skin rejuvenation and hair restoration.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Haircare and skincare industries lead adoption of derma rollers worldwide. Professional clinics use them for scar treatment, anti-aging procedures, and hair loss therapy. At-home users rely on smaller needle sizes for routine product delivery and maintenance of healthy skin.

Manufacturers now use titanium needles instead of standard stainless steel for better durability and hygiene. Titanium resists corrosion, maintains sharper tips, and supports medical-grade sterilization. Consequently, device quality directly affects clinical outcomes, raising buyer expectations for premium materials.

European regulatory frameworks governing cosmetic device safety build consumer trust in microneedling products. Germany, France, and the UK benefit from established aesthetic medicine cultures and high per-capita spending. These regulations encourage manufacturers to meet safety standards, enabling broader market access.

According to a 2025 study on PubMed, microneedling alone increased hair count by 88.4% and thickness by 51.3%. Another 2025 study showed 80.0% of patients using microneedling with cetirizine achieved enhanced hair density versus 25.0% in the control group. These statistics validate consumer investment and strengthen retailer confidence in the category.

Key Takeaways

- Global Derma Roller Market valued at USD 366.6 million in 2025, forecast to reach USD 737.1 million by 2035.

- Market advances at a CAGR of 7.2% from 2026 to 2035.

- By application, Haircare leads with a 67.3% share in 2025.

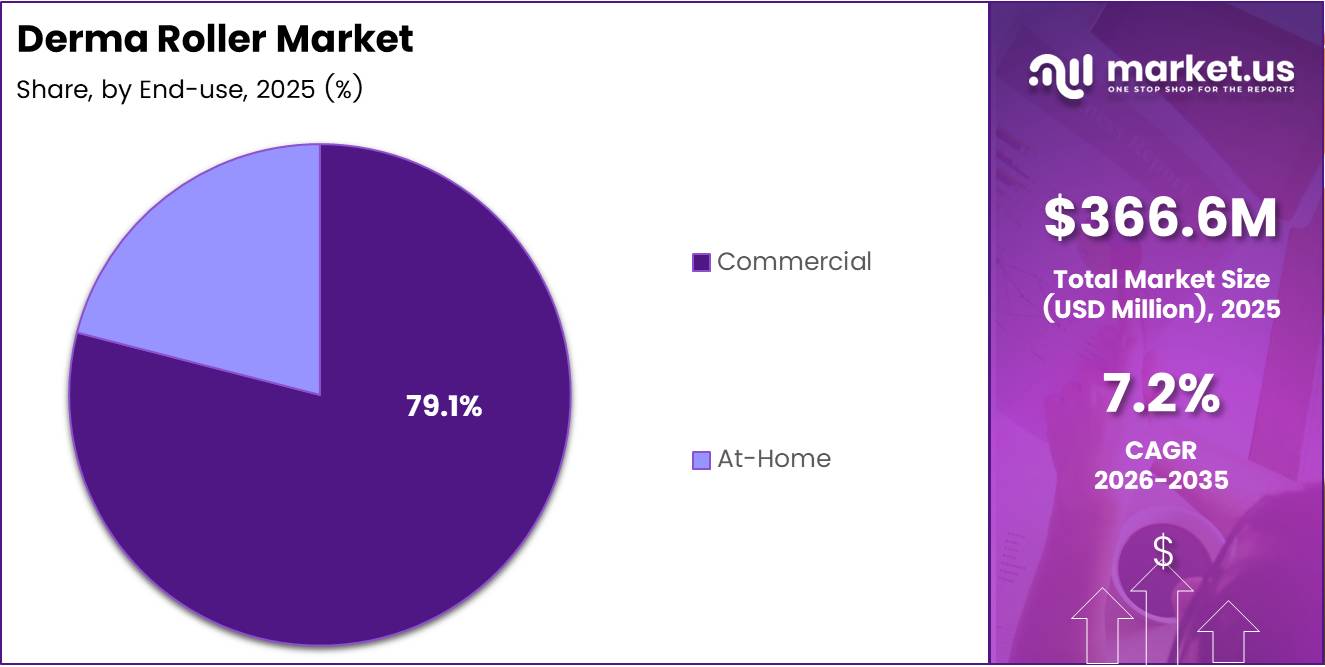

- By end-use, Commercial holds dominant position with 79.1% market share.

- By distribution channel, Supermarket/Hypermarket accounts for 36.9% share.

- By needle size, the 0.5 mm segment captures 32.7% of market share.

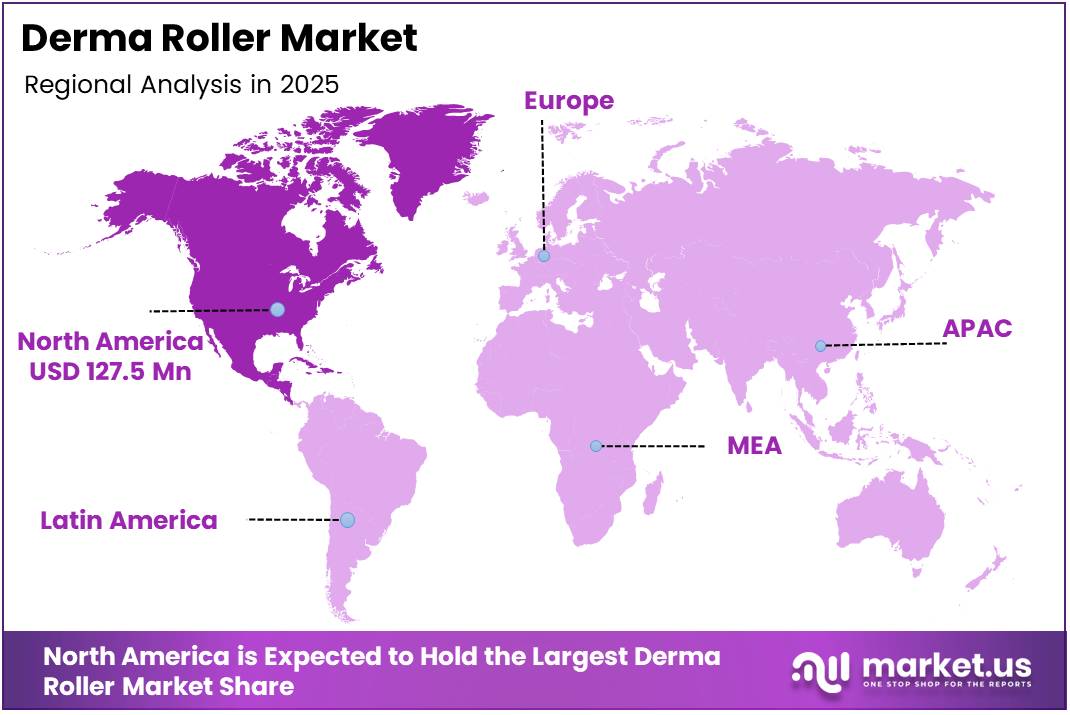

- North America dominates regional markets with 34.8% share, valued at USD 127.5 million.

Market Segmentation Overview

The 0.5 mm needle size dominated with a 32.7% share in 2025. This depth penetrates the dermis sufficiently to trigger collagen synthesis while remaining safe for unsupervised at-home use. Buyers seeking visible results without professional oversight consistently select this size as their entry point.

The 1 mm size differentiates through deeper collagen induction suited for mild scarring and hair follicle stimulation. This size sits between at-home and professional use, creating a premium tier with higher price points. Buyers in this range tend to be repeat purchasers who have graduated from smaller needles.

Haircare applications led the market with a striking 67.3% share in 2025. Clinical research consistently confirms microneedling’s effectiveness in hair restoration, driving consumer trust and professional recommendation. A 2025 study demonstrated cumulative lidocaine permeation of 48.62 ± 6.73 μg/cm², proving strong transdermal delivery for hair growth actives.

Skincare represents the second application pillar, covering anti-aging, scar reduction, and hyperpigmentation treatment. Consumer interest in non-invasive facial rejuvenation positions skincare rollers as accessible alternatives to chemical peels. This application benefits from strong social media visibility that connects device use to visible complexion improvements.

The commercial end-use segment held a dominant 79.1% market share in 2025. Dermatology clinics and aesthetic centers use professional-grade devices with deeper needle depths, justifying premium service pricing. This channel also drives serum and combination treatment revenue, making commercial adoption a strong revenue multiplier.

Supermarkets and hypermarkets accounted for 36.9% of distribution channel share in 2025. Mass retail placements benefit from consumer trust, trial-enabling packaging, and proximity to complementary personal care products. This channel sustains volume sales of entry-level devices and drives brand awareness among casual shoppers.

Drivers

Clinical validation of hair restoration pushes derma roller adoption beyond traditional clinic boundaries. A 2025 study showed microneedling achieved a standardized mean difference of 1.32 versus minoxidil monotherapy for hair count improvement. This margin confirms derma rollers outperform a category-leading pharmaceutical benchmark, giving consumers an evidence-backed at-home response to hair loss and skin aging.

Multi-channel access and e-commerce platforms lower the discovery-to-purchase barrier significantly. Consumers in markets with limited specialty retail can now buy professional-grade devices through online channels. In July 2024, Vegamour introduced the GRO+ Advanced System, a dermatologist-co-developed dermaroller collection. This launch directly responds to consumer appetite for evidence-backed at-home solutions and expands the addressable buyer base well beyond urban centers.

Use Cases

Hair restoration represents the largest real-world application for derma rollers. Consumers with age-related thinning or pattern baldness use 0.5 mm to 1.5 mm devices on the scalp to stimulate follicles and improve topical minoxidil or serum absorption. Clinical studies show this method increases hair density by 30.5% when combined with active ingredients, making it a first-line home treatment for millions.

Skincare and scar reduction form the second major use case, particularly for post-acne atrophic scars and fine lines. Users apply 0.25 mm or 0.5 mm rollers on the face to break down scar tissue and boost collagen production. A 2025 study reported mean improvement in scar grading of 40.69%, with 80% of patients achieving over 30% improvement. This outcome rivals professional laser treatments at a fraction of the cost.

Major Challenges

Safety risks from improper at-home use constrain market expansion significantly. Users frequently select incorrect needle depths or apply devices on compromised skin, leading to infections, scarring, and post-inflammatory hyperpigmentation. These adverse outcomes generate negative consumer reviews, regulatory scrutiny, and media coverage that discourages trial among undecided buyers, particularly harming the at-home segment’s reputation.

Competition from advanced dermatological alternatives limits derma roller adoption for moderate-to-severe conditions. Laser therapy and chemical peels remain benchmark treatments with professional credibility and insurance reimbursement in some markets. According to a 2025 study, investigator-rated hair quality improvement reached 97% with exosome regenerative complex combined with microneedling — results requiring professional administration, not at-home devices. This performance ceiling forces brands to communicate clear use-case boundaries to avoid buyer disappointment.

Business Opportunities

Professional clinic adoption of combination treatment protocols opens new revenue tiers for device makers. Dermatology centers are upgrading from basic needling to protocols that pair microneedling with PRP, serums, and LED therapy. A 2025 study showed mean hair density increased by 30.5% when microneedling combined with 2% chitosan versus control. This efficacy data creates a commercial rationale for clinics to invest in professional-grade devices and proprietary serum pairings, yielding higher per-unit margins.

Asia-Pacific presents the clearest volume expansion opportunity for derma roller manufacturers. Rising middle-class incomes, increasing dermatologist density, and growing e-commerce infrastructure in China, South Korea, India, and Japan replicate conditions that drove North America’s early leadership. South Korea’s influence as a global beauty innovation hub accelerates consumer familiarity with microneedling tools. Manufacturers that establish distribution now will capture scale as local confidence in personal dermatological devices matures.

Regional Analysis

North America dominates the global Derma Roller Market with a 34.8% share, valued at USD 127.5 million in 2025. High consumer awareness of dermatological self-care, a dense network of aesthetic clinics, and mature e-commerce infrastructure collectively sustain this lead. Moreover, favorable insurance-adjacent spending habits in the United States push consumers toward evidence-based personal care devices over cosmetic alternatives, creating a mature benchmark market.

Asia Pacific represents the highest structural growth potential for derma roller adoption. Rising disposable incomes, expanding dermatology clinic networks, and deep e-commerce penetration across China, South Korea, India, and Japan drive this momentum. South Korea’s influence as a global beauty innovation hub accelerates consumer familiarity with microneedling tools. Brands entering this region gain both volume scale and credibility by association with Korean skincare authority.

Recent Developments

- July 2024 — Dermaroller GmbH launched its New Natural Line, a skincare collection featuring cleansers, acids, and serums formulated with natural ingredients. The line directly complements microneedling treatments and targets clean beauty consumers seeking ingredient-transparent post-needling care.

- July 2024 — Vegamour introduced the GRO+ Advanced System, a dermatologist-co-developed dermaroller collection designed to combat severe hair shedding and optimize serum absorption. This launch responds directly to consumer demand for evidence-based at-home hair restoration solutions.

Conclusion

The global Derma Roller Market is on a steady growth trajectory, driven by clinical validation of microneedling for hair restoration and skincare applications. Consumers increasingly prefer non-invasive, at-home devices that deliver measurable results without clinic costs. Consequently, the market expands as e-commerce and mass retail channels lower barriers to entry for first-time buyers.

Haircare remains the dominant application with a 67.3% share, while commercial end-use accounts for 79.1% of revenue. North America leads regionally with 34.8% market share, but Asia Pacific offers the highest growth potential. Manufacturers that invest in combination treatment protocols and emerging market distribution will capture disproportionate value in this evolving landscape.

Companies must address safety risks through better user education and needle-size guidance to maintain category trust. Those that pair devices with proprietary serums, adopt titanium needle construction, and expand into Asia-Pacific will lead the next growth phase. The global Derma Roller Market is forecast to reach USD 737.1 million by 2035, rewarding brands that execute on these strategic priorities.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)