Table of Contents

Market Overview

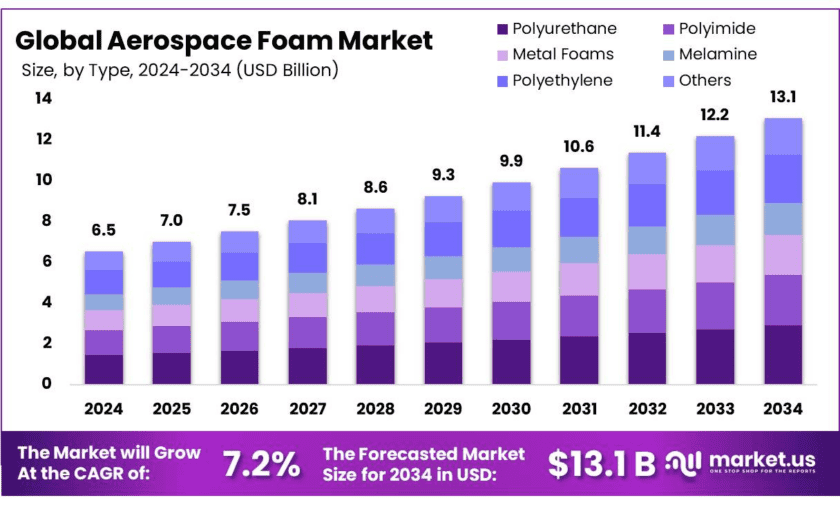

The Global Aerospace Foam Market will grow from USD 6.5 billion in 2024 to USD 13.1 billion by 2034. This expansion represents a compound annual growth rate of 7.2% during the forecast period. Airlines and manufacturers increasingly demand lightweight materials to reduce fuel consumption and operating costs.

Aerospace foam provides low-density cellular structures for thermal insulation, soundproofing, and vibration damping. Moreover, these materials enhance passenger comfort and aircraft safety. Manufacturers produce these foams from polyurethane, polyimide, metal, melamine, and polyethylene raw materials.

Asia Pacific dominated the global market in 2024 with a 38.5% revenue share. The region generated approximately USD 2.5 billion in aerospace foam sales. Rapid aerospace manufacturing expansion and rising air travel demand drive this regional leadership position.

Environmental concerns around petroleum-based foam production present market challenges. Consequently, regulatory bodies like the EPA enforce stricter sustainability standards. However, emerging recycling technologies and circular economy models address these environmental pressures effectively.

Key Takeaways

- The Global Aerospace Foam Market was valued at USD 6.5 billion in 2024 at a CAGR of 7.2% to reach USD 13.1 billion by 2034.

- Polyurethane aerospace foam captured a 22.1% market share in 2024 by type.

- Commercial aviation applications led the market with a 42.5% share in 2024.

- Asia Pacific dominated the market with a 38.5% revenue share in 2024.

➤ Preview Key Insights with an Exclusive Sample Report Download – https://market.us/report/global-aerospace-foam-market/request-sample/

Market Segmentation Overview

Type Analysis

Polyurethane foam dominated the aerospace foam market in 2024 with a 22.1% share. This material offers an optimal balance of lightweight properties, durability, and cost-effectiveness. Unlike specialized, expensive foams, polyurethane provides excellent mechanical strength and versatility at lower costs.

Manufacturers widely use polyurethane foam in aircraft seating, armrests, and insulation panels. Additionally, this material delivers superior cushioning and noise reduction compared to metal or polyethylene foams. Its ease of fabrication further drives adoption across commercial and military aviation applications.

Application Analysis

Commercial aviation led the aerospace foam application market with a 42.5% share in 2024. The sheer volume of commercial aircraft production drives this dominance. Boeing and Airbus manufacture far more commercial jets than military or business aircraft producers.

Each commercial aircraft requires large quantities of foam for seating, insulation, and cabin interiors. For instance, a single Boeing 777 seats over 300 passengers. Consequently, extensive polyurethane foam usage ensures passenger comfort, safety, and noise reduction across commercial fleets.

Drivers

Demand for lightweight materials to improve fuel efficiency drives the aerospace foam market significantly. Airlines face pressure to reduce both operating costs and carbon emissions. Therefore, manufacturers shift toward materials like polyurethane and melamine foams that reduce overall aircraft weight.

A foam core with brushed metal coating can replace aluminum trim around seatback screens. This substitution decreases weight by over 66% and reduces price by 33%. Additionally, every 1 kg of weight reduction saves approximately 0.03 kg of fuel per 1,000 km flown. Consequently, long-haul flights achieve substantial fuel savings through lightweight foam adoption.

Use Cases

Aircraft seating represents the largest use case for aerospace foams in commercial aviation. Polyurethane foam cushions provide passenger comfort while meeting stringent flammability standards. Moreover, these materials reduce noise transmission between seats, enhancing the overall cabin experience for travelers.

Thermal insulation panels in aircraft cabins utilize advanced polyimide and melamine foams. These materials withstand temperatures above 200°C and meet aviation fire safety regulations. Consequently, airlines achieve better temperature control and reduced energy consumption during flights across varying climate zones.

Major Challenges

Environmental concerns around petroleum-based foam production hinder market growth significantly. Many foams use hazardous blowing agents like hydrofluorocarbons (HFCs). HFCs have a global warming potential thousands of times higher than carbon dioxide, prompting stricter environmental regulations worldwide.

Traditional foams are not biodegradable and persist in landfills for decades. Furthermore, foam waste incineration releases toxic fumes, including isocyanates and dioxins. Consequently, manufacturers face pressure from EPA and ECHA regulations to develop greener alternatives or risk production limitations.

Business Opportunities

Technological advancements in raw materials create significant business opportunities for foam manufacturers. Innovations in polymer chemistry produce foams with improved thermal resistance and fire retardancy. Additionally, high-performance polyimide foams now enable demanding applications like ducting and cabin linings.

Integration of nanomaterials such as carbon nanotubes into foam structures enhances conductivity and impact resistance. These advanced foams can reduce cabin vibration and noise levels by up to 40%. Therefore, manufacturers offering nanotechnology-enhanced foams can command premium pricing and capture market share.

Regional Analysis

Asia Pacific led the global aerospace foam market with USD 2.5 billion in revenue during 2024. The region captured 38.5% of the total market share. Rapid aerospace manufacturing growth in China, India, and Japan, combined with expanding low-cost carrier fleets, drives this regional dominance.

The Asia Pacific accounted for a 33.6% share of global passenger traffic in 2024. Year-on-year demand increased by 8.7% in the region. Consequently, local foam manufacturers benefit from strong demand for seating, insulation, and interior components across expanding airline fleets.

The major Players in The Industry

- BASF SE

- Boyd

- Diab Group

- DuPont

- 3A Composites

- Aerofoam Industries, LLC

- ARMACELL

- ERG Aerospace Corporation

- Evonik Industries AG

- General Plastics Manufacturing Company

- Grand Rapids Foam Technologies

- Greiner Aerospace

- Rogers Corporation

- Technifab, Inc.

- UFP Technologies, Inc.

- Zotefoams plc

- Recticel NV/SA

- Other Key Players

Conclusion

The global aerospace foam market continues its steady growth trajectory driven by fuel efficiency demands. Manufacturers increasingly adopt lightweight polyurethane and advanced polyimide foams across commercial and military applications. Moreover, technological innovations in raw materials and recycling processes address environmental concerns while expanding use cases.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)