Table of Contents

Market Overview

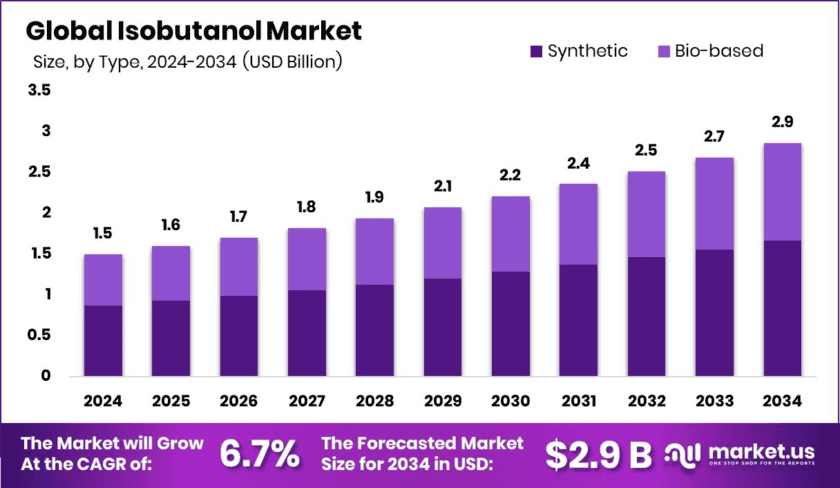

The Global Isobutanol Market reached a value of USD 1.5 billion in 2024. This market serves multiple sectors, including paints, coatings, fuels, and pharmaceuticals. Manufacturers rely on isobutanol for its excellent solvent properties and chemical stability.

Market analysts project the isobutanol market to grow at a compound annual growth rate of 6.7% from 2025 to 2034. Consequently, the market value will likely reach approximately USD 2.9 billion by the end of 2034. This steady growth reflects consistent industrial demand across multiple regions.

Isobutanol, also known as 2-methylpropan-1-ol, functions as a colorless, flammable organic compound. It carries a characteristic sweet and musty odor that makes it easily identifiable. Producers create this chemical through hydroformylation of allyl alcohol or carbonylation of propylene.

The chemical industry uses isobutanol primarily as a solvent for varnishes and as a precursor for other esters. Its applications extend to coatings, flavors, fragrances, pharmaceuticals, and pesticides. Therefore, isobutanol serves as a versatile building block for many products.

Global demand for efficient fuels drives one major application of isobutanol in the fuel industry. The chemical offers a high octane rating that improves fuel performance significantly. Additionally, manufacturers face increasing pressure to shift toward sustainable and bio-based chemical solutions.

Despite these advantages, environmental concerns pose challenges for market expansion. Isobutanol exhibits toxic properties that affect aquatic ecosystems negatively. The industry must therefore balance industrial utility with environmental responsibility moving forward.

Key Takeaways

- The Global Isobutanol Market value reached USD 1.5 billion in 2024 projects to grow at a CAGR of 6.7%, reaching USD 2.9 billion by 2034.

- Synthetic isobutanol dominated the market with a share of 58.1% in 2024.

- Isobutanol with purity above 99% led the market, capturing 48.1% share.

- Asia Pacific led global consumption with approximately 41.6% market share in 2024.

➤ Download Exclusive Sample Of This Premium Report (Including Full TOC, Table & Figures)- https://market.us/report/isobutanol-market/request-sample/

Market Segmentation Overview

Based on type, synthetic isobutanol captured the largest market share of 58.1% in 2024. This dominance stems from cost-effectiveness and well-established production processes using petrochemical feedstocks. Moreover, mature infrastructure and economies of scale make synthetic isobutanol more affordable and widely available for industrial users.

Bio-based isobutanol faces scalability limitations due to complex fermentation processes and higher operational costs. Consequently, synthetic isobutanol offers more reliable performance in solvents, coatings, and fuels. Price stability and consistent supply remain critical factors for industrial buyers choosing between these options.

Regarding purity, isobutanol, exceeding 99% purity, dominated the market with a 48.1% share in 2024. High-purity isobutanol ensures better performance and consistency while reducing impurities that could interfere with chemical processes. Sensitive applications such as pharmaceuticals, coatings, and electronics demand this higher purity level.

Lower-purity isobutanol can alter drying times or compromise finish quality in paint formulations. Therefore, manufacturers pursuing precision and high-quality output prefer high-purity isobutanol as their standard choice. This preference drives the continued dominance of the above 99% purity segment across multiple industries.

Among applications, paints and coatings dominated the isobutanol market with a 43.2% share in 2024. Excellent solvent properties, moderate evaporation rate, and compatibility with various resins make isobutanol essential for this sector. Additionally, coatings require large solvent volumes, which drives higher consumption compared to other applications.

Isobutanol improves flow, leveling, and film formation in automotive, industrial, and architectural coatings. Its widespread utility and lower cost compared to specialty chemicals explain its dominant position. Consequently, the paints and coatings sector remains the largest consumer of isobutanol globally.

Drivers

Isobutanol plays a crucial role in paints and coatings due to its low volatility and excellent solvency properties. Manufacturers use it to improve flow, leveling, and drying time in various formulations. Consequently, automotive and industrial coatings rely on isobutanol for consistent film formation and environmental resistance.

Environmental regulations tightening around volatile organic compounds favor the adoption. This chemical offers lower toxicity compared to traditional solvents such as toluene or xylene. Therefore, companies increasingly select isobutanol as a preferred alternative for high-performance and environmentally friendly coatings.

Use Cases

In the fuel industry, isobutanol serves as a promising biofuel additive and gasoline alternative. It contains approximately 21% more energy per volume than ethanol, making it more efficient for blending. Additionally, lower water absorption makes isobutanol compatible with existing pipelines and storage tanks without costly modifications.

Engine performance benefits from isobutanol’s higher octane rating and improved combustion properties. Manufacturers can blend isobutanol up to 16% with gasoline without requiring engine modifications. This flexibility makes isobutanol an attractive option for transportation fuels while reducing greenhouse gas emissions.

Major Challenges

Aquatic toxicity presents a significant concern for the isobutanol market, as demonstrated by the Minnesota chemical spill incident. When isobutanol leaks into water bodies, it reduces dissolved oxygen levels and harms fish populations. High concentration exposure leads to behavioral changes, inhibited growth, and mortality in aquatic species.

The Minnesota incident increased regulatory scrutiny regarding the storage, transportation, and handling of isobutanol. Spills during rail or truck transport can cause environmental damage and legal consequences for companies. Therefore, tighter environmental regulations and growing chemical safety awareness challenge industry expansion.

Business Opportunities

Bio-based isobutanol production from renewable feedstocks creates significant growth opportunities for chemical manufacturers. Corn, sugarcane, and agricultural waste serve as raw materials for fermentation-based production processes. Companies such as Gevo and Butamax actively develop bio-based isobutanol technologies to scale up sustainable supply.

The fuel industry’s shift toward cleaner alternatives opens new markets for bio-isobutanol as a gasoline blendstock. Higher energy content and lower volatility compared to ethanol make bio-isobutanol superior for many applications. Additionally, sustainability goals across multiple industries drive continued preference for bio-based isobutanol over petrochemical alternatives.

Regional Analysis

Asia Pacific led the global isobutanol market in 2024 with approximately USD 624 million in value, representing 41.6% of the total revenue share. Strong industrial base and growing chemical manufacturing sector drive this regional dominance. China, India, South Korea, and Japan serve as major consumers and producers of isobutanol.

China’s rapidly growing automotive and construction sectors fuel demand for coatings and resins using isobutanol. India’s rising chemical consumption for paints and agrochemicals similarly supports domestic isobutanol usage. Moreover, large petrochemical complexes and cost-effective production capabilities boost regional output significantly.

Top Key Players in the Market

- Mitsubishi Chemical Group Corporation

- Eastman Chemical Company

- KH Neochem Co., Ltd.

- BASF SE

- Gevo Inc.

- SABIC

- Tasnee

- Dow Inc.

- Grupa Azoty S.A.

- The Andhra Petrochemicals Limited

- Bharat Petroleum Corporation Limited

- Nan Ya Plastics Corporation

- Sasol

- INEOS Group

- Other Key Players

Conclusion

The global isobutanol market demonstrates steady growth. Synthetic isobutanol dominates current production, while bio-based variants gain traction for sustainability reasons. Paints and coatings remain the largest application sector, though fuel additives present strong growth opportunities. Asia Pacific leads regional consumption, driven by China and India’s industrial expansion.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)