Introduction

Luxury Goods Statistics: Luxury goods encompass high-quality, exclusive products like fashion items, automobiles, and fine wines, appealing primarily to affluent consumers seeking status and superior experiences.

This market relies heavily on brand prestige, craftsmanship, and a sense of exclusivity to attract and retain customers with high disposable incomes.

Distribution channels typically include company-owned boutiques, upscale retailers, and, increasingly, online platforms.

Challenges such as economic fluctuations and shifting consumer values towards sustainability are balanced by opportunities in digital innovation and expanding global markets.

Understanding these dynamics is crucial for navigating the competitive landscape and maintaining brand relevance in the evolving luxury goods sector.

Editor’s Choice

- The global luxury goods market revenue is projected to reach USD 418.89 billion in 2028.

- The forecast for 2027 shows online sales continuing to rise to 18.2%. While offline sales further declined to 81.8%. Reflecting an ongoing shift towards digital channels in the luxury goods market.

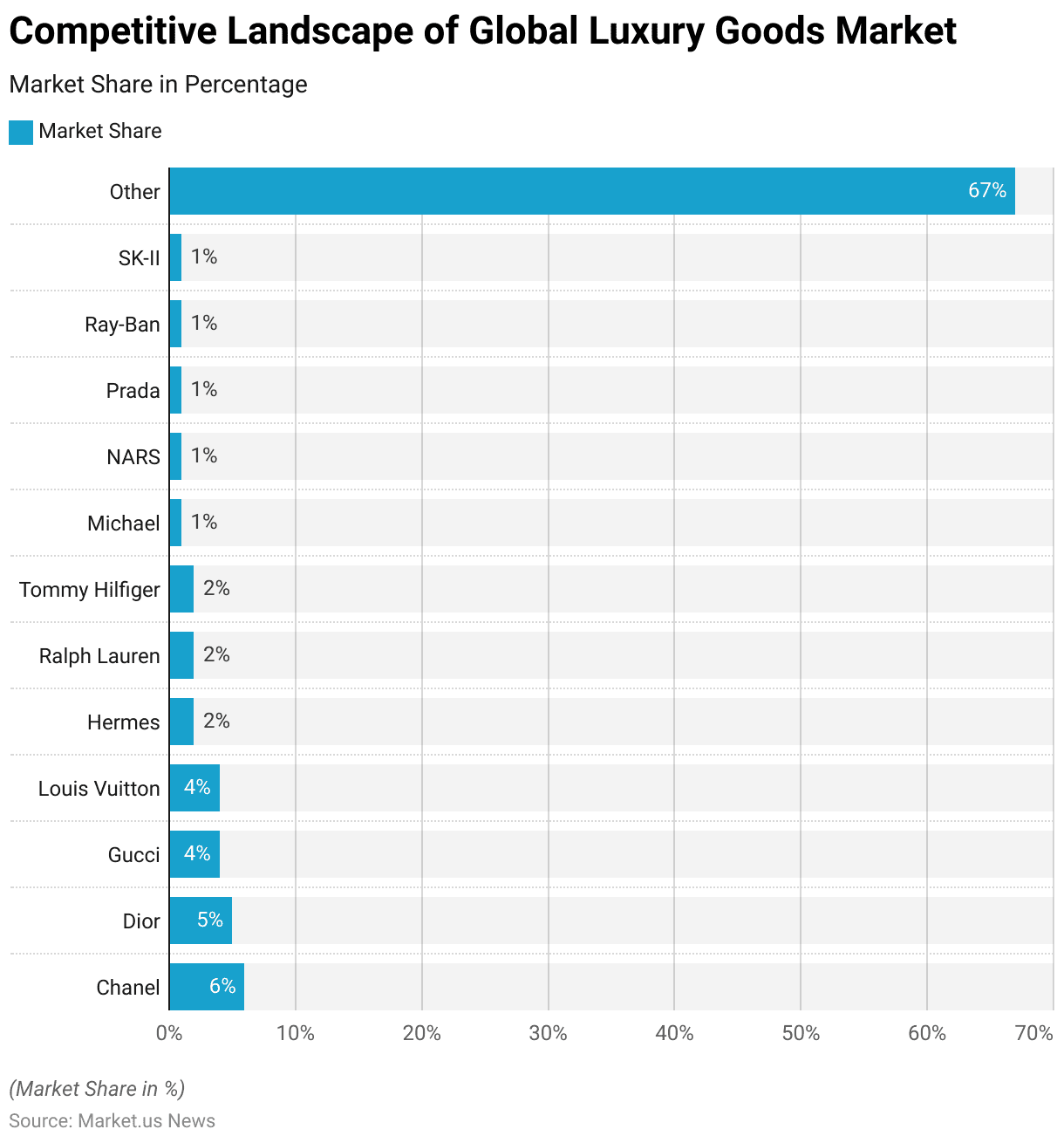

- The global luxury goods market is characterized by the presence of several prominent brands, each holding varying market shares. Leading the market is Chanel, with a 6% share.

- In 2022, the leading luxury brands worldwide were valued at significant figures. Reflecting their dominant market positions and strong consumer appeal. Louis Vuitton, originating from France, topped the list with a brand value of USD 124,273 million.

- When conducting online research before purchasing luxury goods, consumers exhibit a preference for various sources. Multi-brand full-price websites are the most favored, with 39% of respondents indicating they use these platforms for their research.

- In 2020, luxury companies in France faced several key challenges, as identified by industry professionals. The most significant challenge was the commitment to corporate social responsibility (CSR), highlighted by 63% of respondents.

Luxury Goods Market Statistics

Global Luxury Goods Market Size Statistics

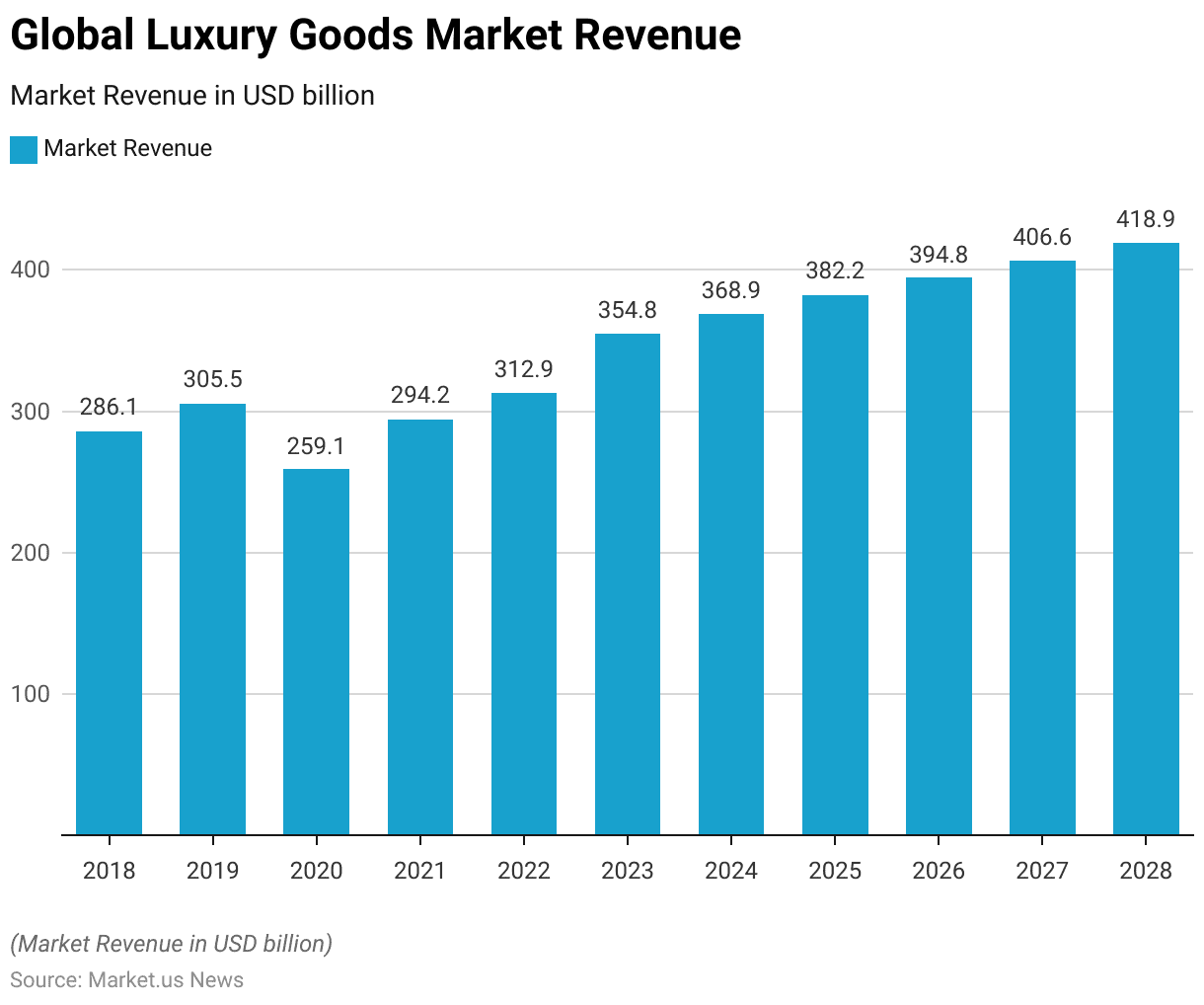

- The global luxury goods market has demonstrated a dynamic pattern of growth and resilience over the past several years at a CAGR of 3.22%.

- In 2018, the market generated revenues of USD 286.11 billion, which increased to USD 305.46 billion in 2019.

- However, 2020 saw a decline to USD 259.14 billion, likely due to the impacts of the COVID-19 pandemic.

- Recovery was evident in 2021, with revenues rising to USD 294.24 billion.

- This upward trajectory continued in 2022, with the market reaching USD 312.91 billion.

- The positive trend persists into 2023, with projected revenues of USD 354.81 billion, and further growth is anticipated in the coming years.

- By 2024, the market is expected to generate USD 368.94 billion, increasing to USD 382.20 billion in 2025.

- The market’s expansion is forecasted to continue. With revenues reaching USD 394.75 billion in 2026, USD 406.55 billion in 2027, and USD 418.89 billion in 2028.

- This consistent growth underscores the resilience and expanding consumer base for luxury goods globally.

(Source: Statista)

Global Luxury Goods Market Size – By Type Statistics

2018-2023

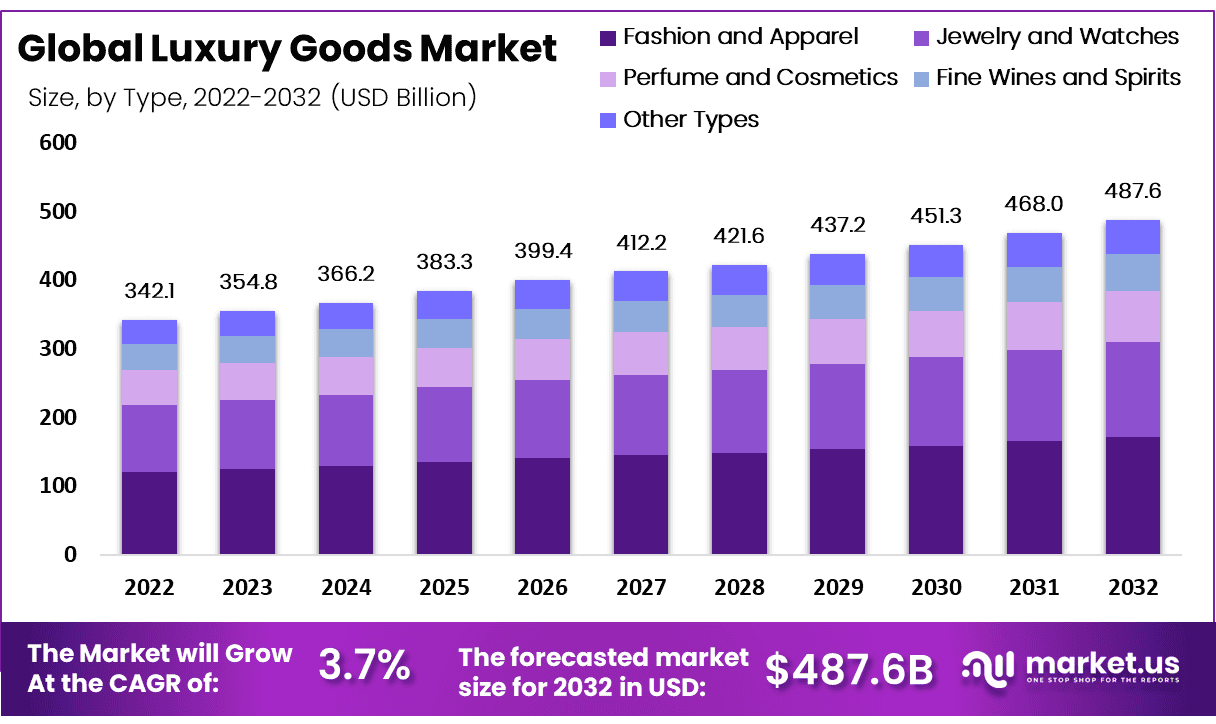

- The global luxury goods market, segmented by type, has exhibited notable trends and growth across various categories from 2018 to 2028.

- In 2018, luxury eyewear accounted for USD 19.0 billion. Luxury fashion is USD 90.58 billion, and luxury leather goods is USD 56.67 billion. Luxury watches and jewelry are USD 62.57 billion, and prestige cosmetics and fragrances are USD 57.32 billion.

- By 2019, these figures had increased to USD 19.6 billion, USD 95.82 billion, USD 62.15 billion, USD 66.82 billion, and USD 61.11 billion, respectively.

- The market faced a downturn in 2020, with all categories experiencing declines. Notably luxury eyewear dropped to USD 15.6 billion and luxury fashion to USD 85.56 billion.

- However, recovery was evident in 2021, with luxury eyewear reaching USD 17.6 billion and luxury leather goods reaching USD 62.74 billion.

- The growth trajectory continued into 2022. With luxury fashion reaching USD 97.33 billion and prestige cosmetics and fragrances USD 62.39 billion.

- The upward trend accelerated in 2023, with luxury eyewear at USD 21.2 billion and luxury watches and jewelry at USD 74.97 billion.

2024-2028

- Projections for 2024 anticipate further increases. Luxury fashion is expected to reach USD 115.9 billion and luxury leather goods USD 79.36 billion.

- By 2025, these categories are projected to grow to USD 22.2 billion for luxury eyewear, USD 120.1 billion for luxury fashion, and USD 82.71 billion for luxury leather goods.

- The market is forecasted to continue expanding through 2026 and beyond. With luxury fashion reaching USD 124 billion, luxury leather goods USD 85.92 billion, and prestige cosmetics and fragrances USD 80.97 billion.

- By 2028, the luxury goods market is anticipated to see luxury eyewear at USD 23.3 billion, luxury fashion at USD 131.7 billion, and luxury leather goods at USD 92.37 billion. Luxury watches and spiritual jewelry at USD 84.82 billion. Prestige cosmetics and fragrances at USD 86.69 billion, demonstrating robust and sustained growth across all segments.

(Source: Statista)

Global Luxury Goods Market Share – By Sales Channel Statistics

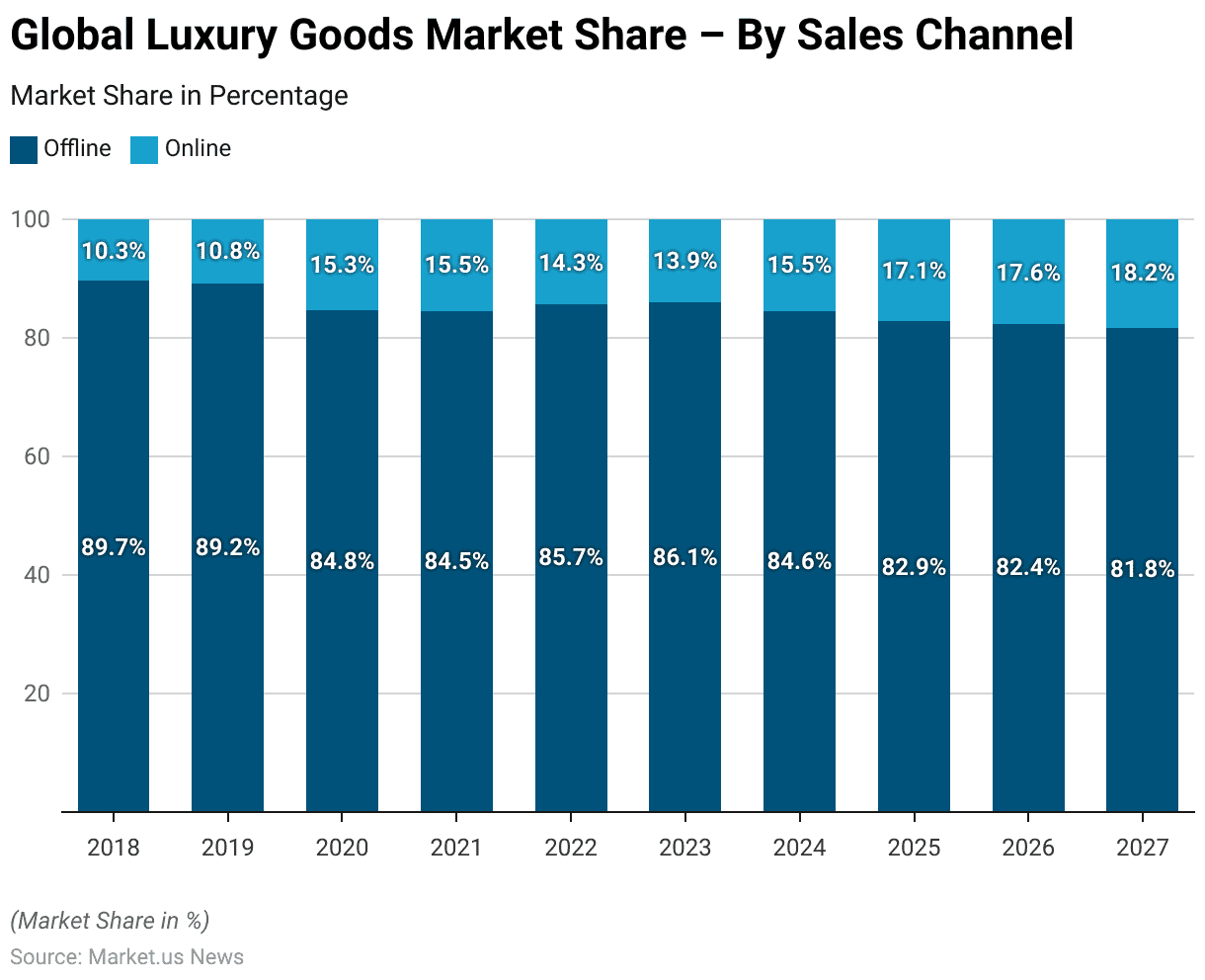

- The global luxury goods market share by sales channel has exhibited significant shifts between offline and online channels from 2018 to 2027.

- In 2018, offline sales dominated the market with an 89.7% share, while online sales accounted for 10.3%. This trend continued in 2019, with offline sales at 89.2% and online sales slightly increasing to 10.8%.

- The year 2020 marked a notable change, as offline sales decreased to 84.8%, and online sales surged to 15.3%. Likely influenced by the global pandemic and the resultant shift in consumer behavior. This trend persisted into 2021, with offline sales at 84.5% and online sales at 15.5%.

- In 2022, offline sales rebounded slightly to 85.7%, while online sales decreased to 14.3%. However, by 2023, the market saw a minor decline in offline sales to 86.1%, and online sales rose to 13.9%.

- Projections for 2024 indicate a further increase in online sales, reaching 15.5%, as offline sales drop to 84.6%.

- This trend is expected to continue, with online sales growing to 17.1% in 2025 and offline sales declining to 82.9%.

- By 2026, online sales are projected to reach 17.6%, with offline sales at 82.4%.

- The forecast for 2027 shows online sales continuing to rise to 18.2%. While offline sales further declined to 81.8%. Reflecting an ongoing shift towards digital channels in the luxury goods market.

(Source: Statista)

Competitive Landscape of Global Luxury Goods Market Statistics

- The global luxury goods market is characterized by the presence of several prominent brands, each holding varying market shares.

- Leading the market is Chanel, with a 6% share, followed by Dior at 5%.

- Gucci and Louis Vuitton each capture 4% of the market.

- Hermes, Ralph Lauren, and Tommy Hilfiger each hold a 2% share.

- Several other brands, including Michael, NARS, Prada, Ray-Ban, and SK-II, each account for 1% of the market.

- Collectively, these well-known brands comprise a significant portion of the market. However, a substantial 67% of the market is occupied by other brands, indicating a highly fragmented and competitive landscape in the luxury goods sector.

(Source: Statista)

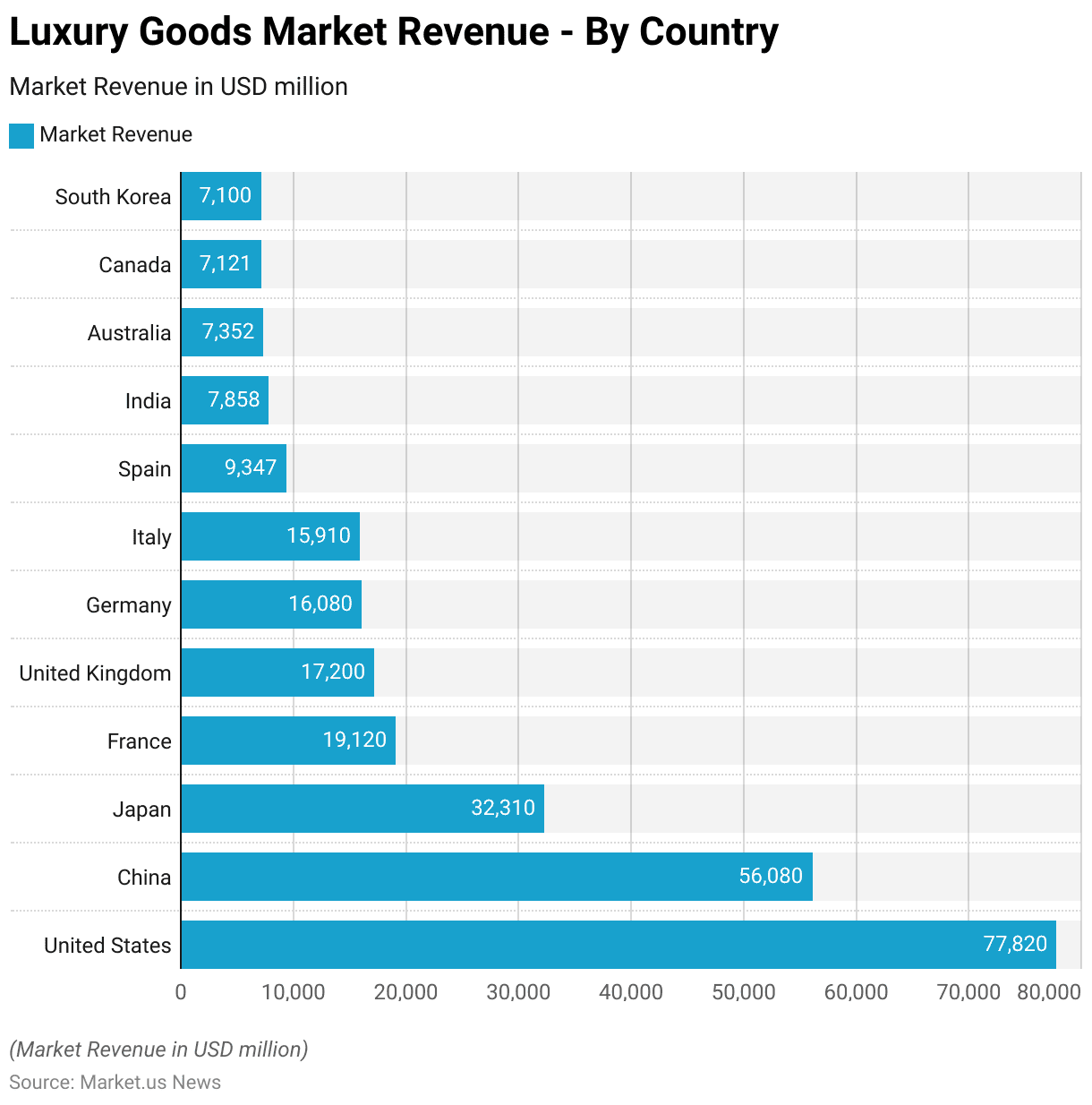

Global Luxury Goods Market Revenue – By Country Statistics

- The global luxury goods market exhibits significant revenue contributions from various countries.

- The United States leads the market with a substantial revenue of USD 77,820 million, followed by China with USD 56,080 million.

- Japan contributes USD 32,310 million to the market, while France generates USD 19,120 million.

- The United Kingdom and Germany follow closely with revenues of USD 17,200 million and USD 16,080 million, respectively.

- Italy also makes a notable contribution of USD 15,910 million.

- In Spain, the luxury goods market revenue stands at USD 9,347 million.

- India, Australia, and Canada contribute USD 7,858 million, USD 7,352 million, and USD 7,121 million, respectively. South Korea also holds a significant share with a revenue of USD 7,100 million.

- This distribution underscores the diverse and expansive nature of the luxury goods market across these leading countries.

(Source: Statista)

Revenue Generation Through Luxury Goods Statistics

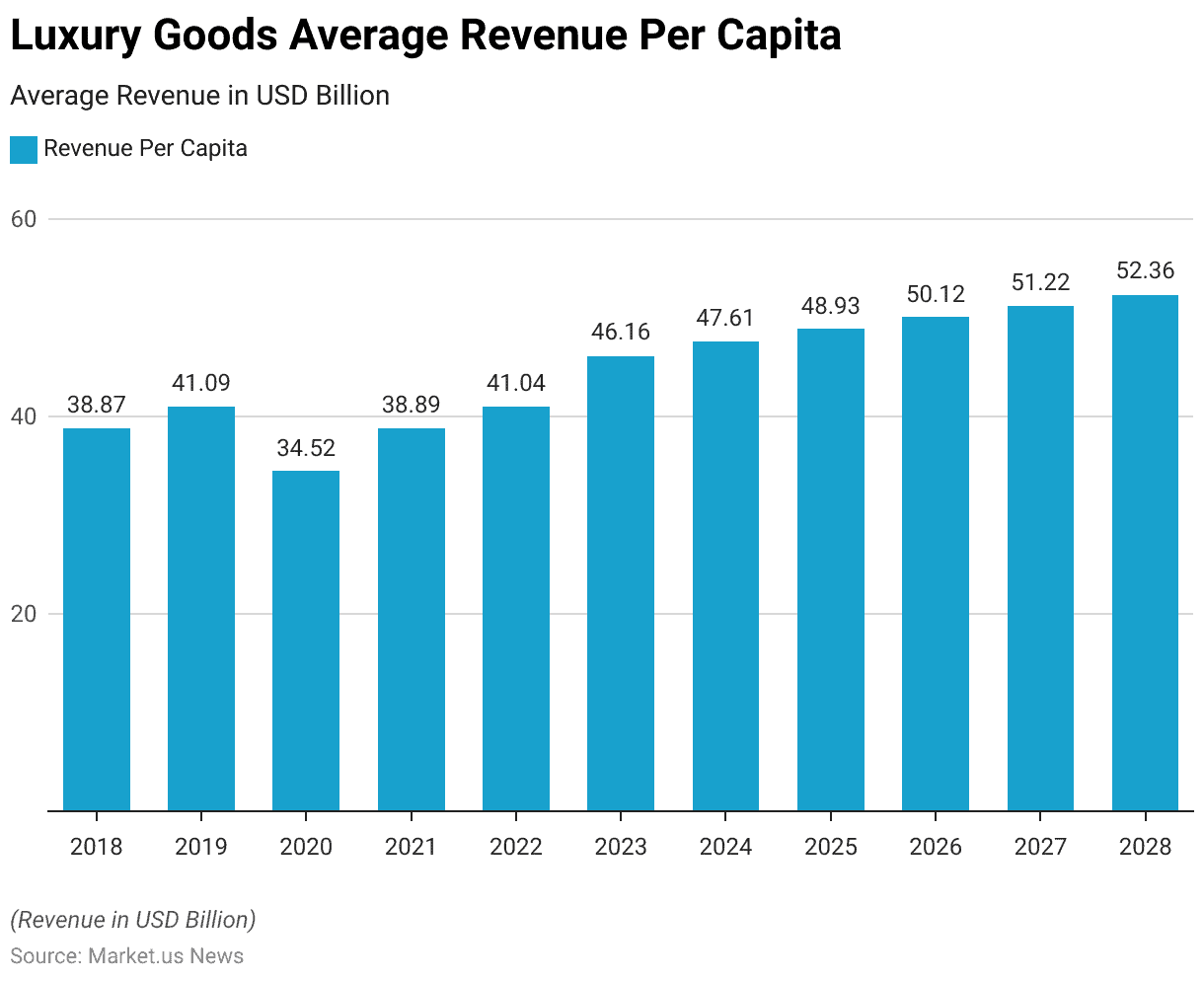

Luxury Goods Average Revenue Per Capita Statistics

- The average revenue per capita in the global luxury goods market has fluctuated, yet there has been a generally upward trend from 2018 to 2028.

- In 2018, the average revenue per capita stood at USD 38.87, increasing to USD 41.09 in 2019.

- The year 2020 saw a dip to USD 34.52, likely due to the economic impacts of the COVID-19 pandemic.

- However, a recovery was evident in 2021, with the average revenue per capita rising to USD 38.89.

- This positive trend continued in 2022, reaching USD 41.04, and further accelerated in 2023, climbing to USD 46.16.

- Projections for the coming years indicate continued growth, with the average revenue per capita expected to reach USD 47.61 in 2024 and USD 48.93 in 2025.

- By 2026, it is anticipated to rise to USD 50.12, followed by USD 51.22 in 2027 and USD 52.36 in 2028.

- This progression reflects a robust and increasing consumer spending on luxury goods over the forecast period.

(Source: Statista)

Luxury Goods Average Revenue Per Capita – By Type Statistics

2018-2022

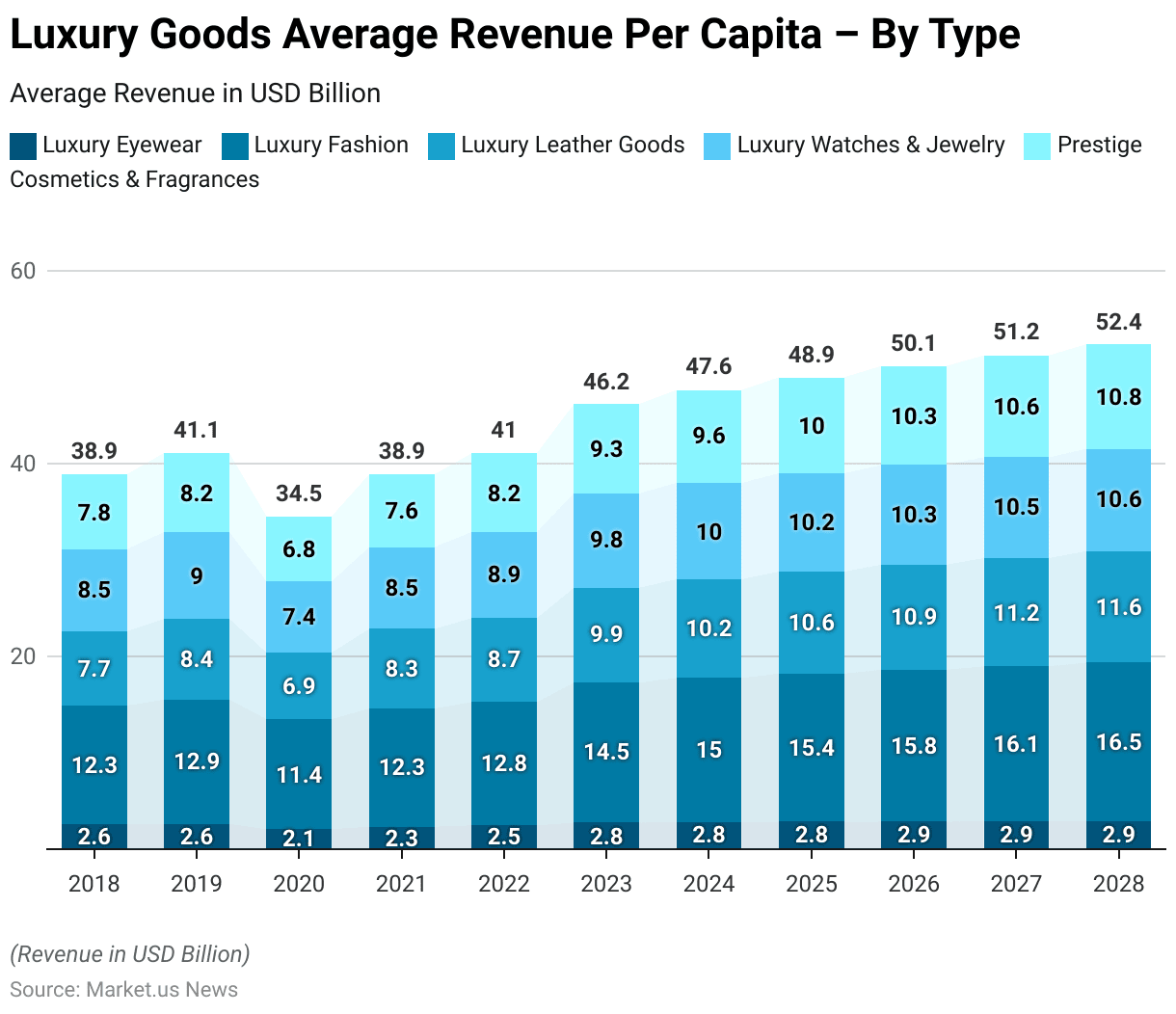

- The average revenue per capita in the luxury goods market, segmented by type, has shown notable trends from 2018 to 2028.

- In 2018, luxury eyewear generated average revenue of USD 2.58 per capita, luxury fashion USD 12.30, luxury leather goods USD 7.70, luxury watches and jewelry USD 8.50, and prestige cosmetics and fragrances USD 7.79.

- By 2019, these figures had increased to USD 2.63, USD 12.89, USD 8.36, USD 8.99, and USD 8.22, respectively.

- The year 2020 saw a decline across all categories, with luxury eyewear dropping to USD 2.08, luxury fashion to USD 11.40, luxury leather goods to USD 6.92, luxury watches and jewelry to USD 7.36, and prestige cosmetics and fragrances to USD 6.76.

- Recovery was observed in 2021, with luxury eyewear increasing to USD 2.33 and luxury fashion to USD 12.25. This upward trend continued in 2022, with luxury leather goods reaching USD 8.69 and prestige cosmetics and fragrances at USD 8.18.

2023-2028

- In 2023, significant growth was noted, particularly in luxury fashion at USD 14.50 and luxury leather goods at USD 9.86.

- Projections for 2024 indicate further increases, with luxury eyewear at USD 2.81 and luxury watches and jewelry at USD 9.97.

- By 2025, the average revenue per capita is expected to reach USD 2.84 for luxury eyewear, USD 15.37 for luxury fashion, USD 10.59 for luxury leather goods, USD 10.16 for luxury watches and jewelry, and USD 9.97 for prestige cosmetics and fragrances.

- This growth trajectory is anticipated to continue through 2026 and 2027, with all categories showing incremental increases.

- By 2028, the market is projected to see luxury eyewear at USD 2.91, luxury fashion at USD 16.46, luxury leather goods at USD 11.55, luxury watches and jewelry at USD 10.60, and prestige cosmetics and fragrances at USD 10.84. Reflecting a steady and robust expansion in consumer spending across all luxury goods segments.

(Source: Statista)

Luxury Goods Sales Statistics

Luxury Goods Sales Growth, Net Profit Margin, And Return On Assets Statistics

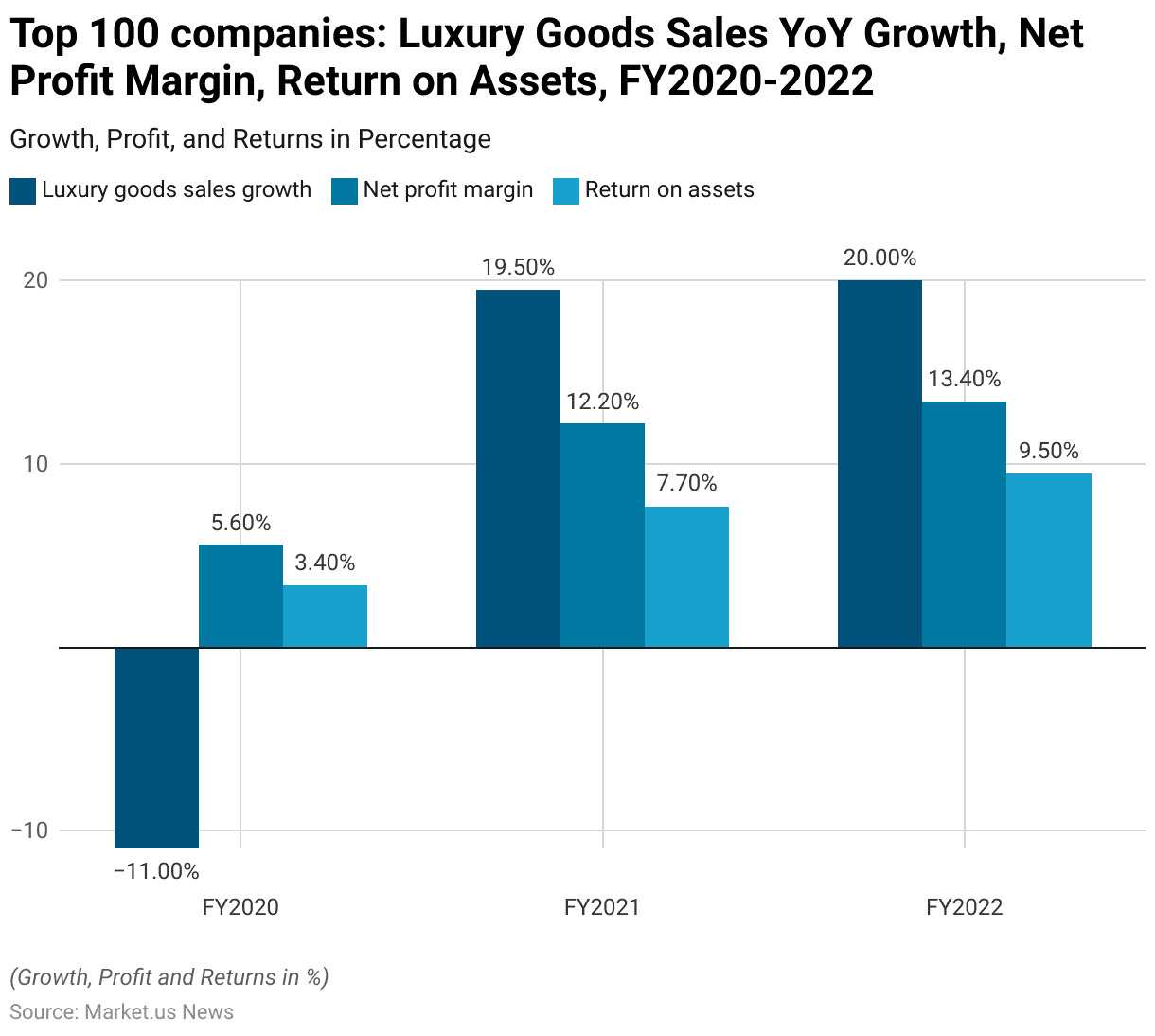

- The top 100 companies in the luxury goods sector have exhibited significant fluctuations in key financial metrics from FY2020 to FY2022.

- In FY2020, the sector experienced a decline in luxury goods sales growth, recording a negative growth rate of -11%, largely attributable to the global disruptions caused by the COVID-19 pandemic.

- However, a strong recovery was observed in FY2021. With luxury goods sales growth rebounding to 19.50%, this positive trend continued into FY2022 with a further increase of 20%.

- Net profit margins also demonstrated substantial improvement over this period. In FY2020, the net profit margin stood at 5.60%, but this figure more than doubled by FY2021, reaching 12.20%, and continued to rise to 13.40% in FY2022, reflecting enhanced profitability and operational efficiency within the sector.

- Similarly, the return on assets (ROA) saw a marked increase. In FY2020, the ROA was 3.40%, indicating modest returns relative to the assets employed. This metric improved significantly in FY2021, climbing to 7.70%, and further increased to 9.50% in FY2022.

- These trends underscore the sector’s robust recovery and growing financial health post-pandemic, highlighting the resilience and strong performance of the top luxury goods companies.

(Source: Deloitte)

Top 10 Luxury Goods Companies by Sales in FY2022 Statistics

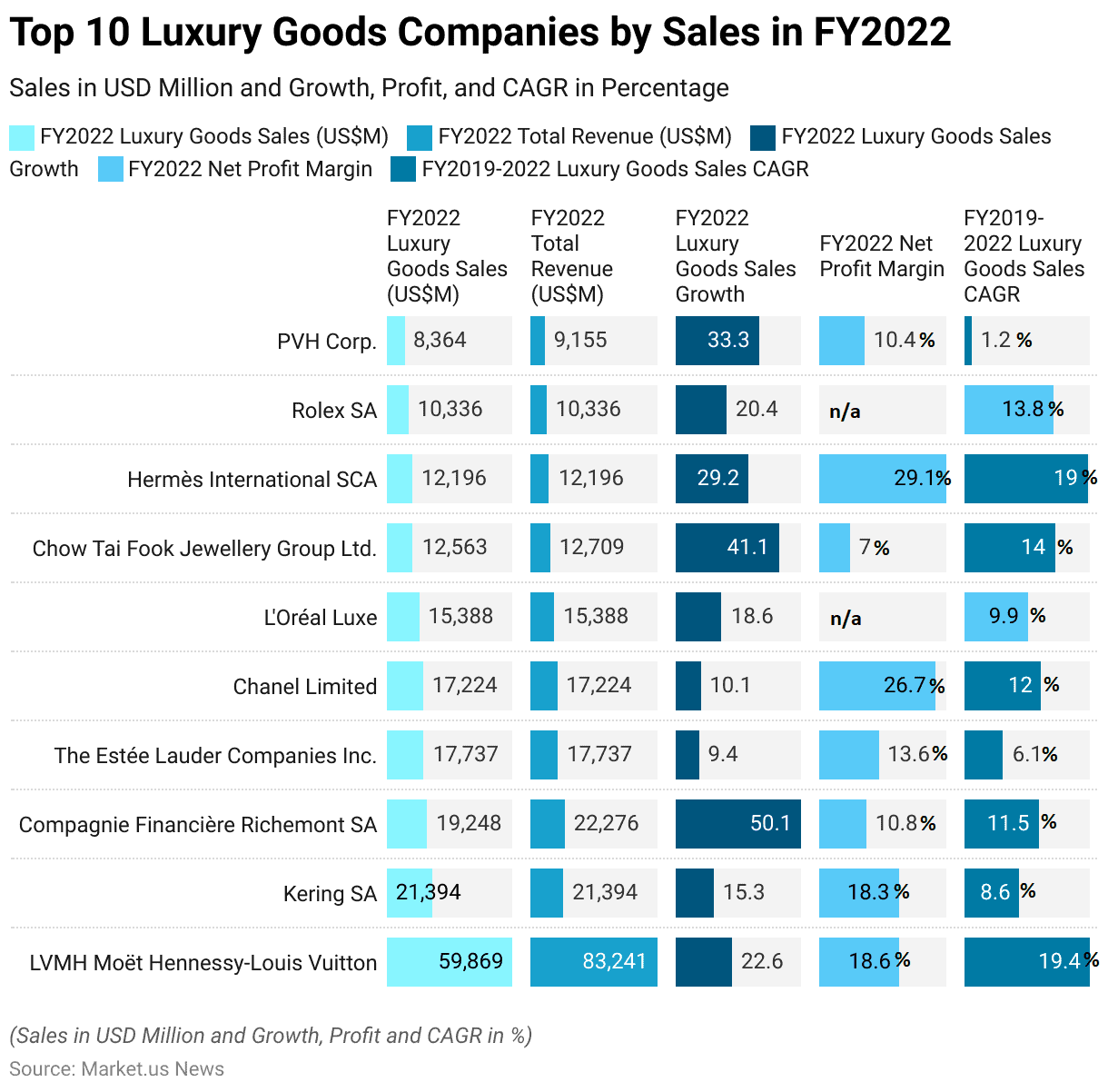

- In FY2022, the luxury goods sector was dominated by several key players demonstrating impressive financial performance.

- LVMH Moët Hennessy-Louis Vuitton led the market with luxury goods sales of USD 59,869 million out of a total revenue of USD 83,241 million, achieving a sales growth of 22.60% and a net profit margin of 18.60%. Kering SA followed with luxury goods sales of USD 21,394 million, matching its total revenue, and posted a 15.30% sales growth and an 18.30% net profit margin.

- Compagnie Financière Richemont SA reported luxury goods sales of USD 19,248 million and a total revenue of USD 22,276 million, with a remarkable sales growth of 50.10% and a net profit margin of 10.80%.

- The Estée Lauder Companies Inc. generated luxury goods sales of USD 17,737 million, reflecting a 9.40% growth rate and a net profit margin of 13.60%. Chanel Limited reported sales of USD 17,224 million, with a 10.10% growth rate and an outstanding net profit margin of 26.70%.

More Insights

- L’Oréal Luxe achieved luxury goods sales of USD 15,388 million, growing at 18.60%, while Chow Tai Fook Jewellery Group Ltd. posted sales of USD 12,563 million, with a notable growth rate of 41.10% and a net profit margin of 7.00%.

- Hermès International SCA recorded luxury goods sales of USD 12,196 million, showing a strong growth rate of 29.20% and a net profit margin of 29.10%. Rolex SA’s sales stood at USD 10,336 million, growing at 20.40%.

- PVH Corp. reported luxury goods sales of USD 8,364 million out of a total revenue of USD 9,155 million, with a significant sales growth rate of 33.30% and a net profit margin of 10.40%. These figures highlight the robust performance and growth trajectories of leading luxury goods companies in FY2022.

(Source: Deloitte)

Luxury Goods Brands Statistics

Brand Value of the Leading 10 Most Valuable Luxury Brands Worldwide

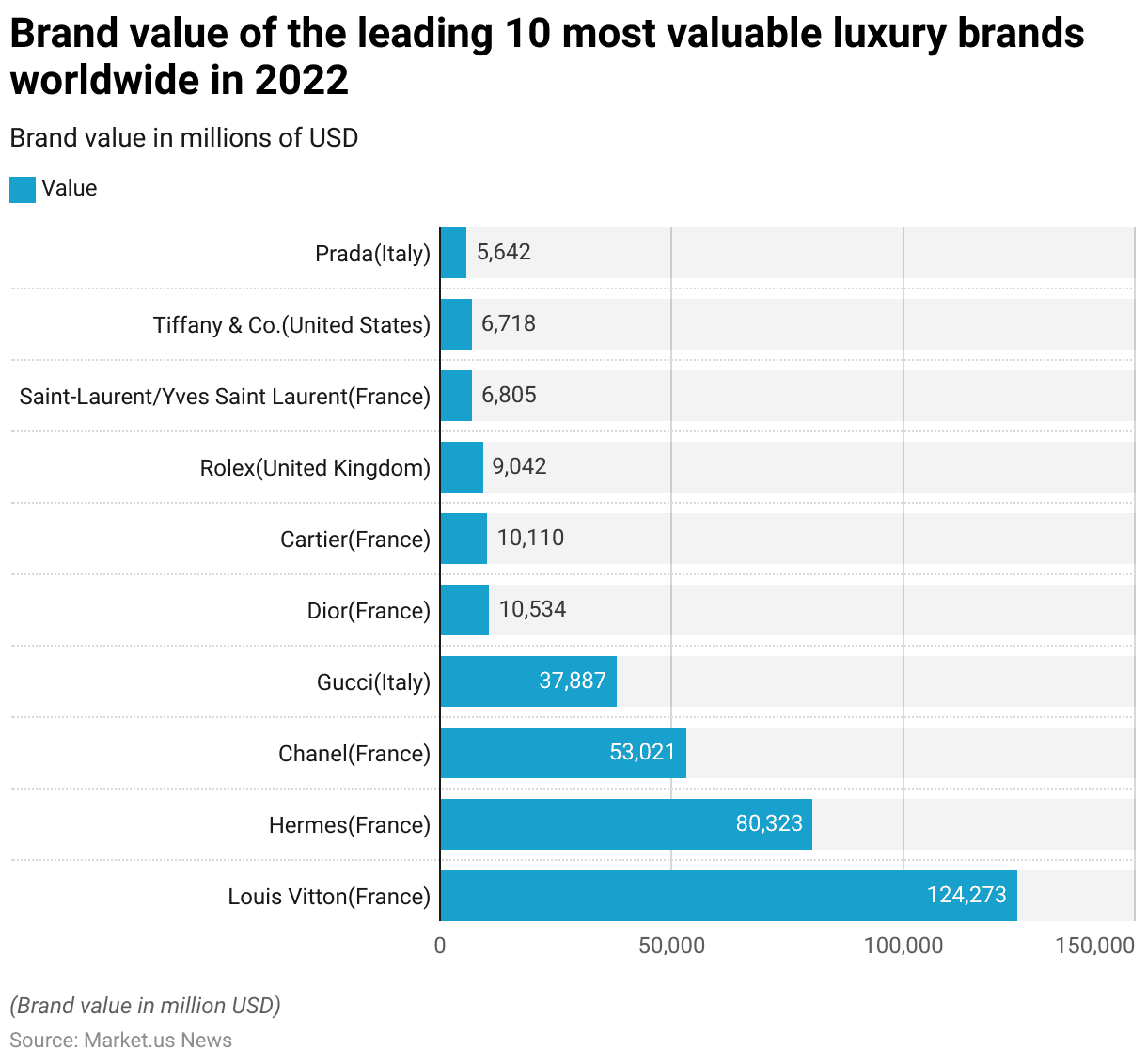

- In 2022, the leading luxury brands worldwide were valued at significant figures, reflecting their dominant market positions and strong consumer appeal.

- Louis Vuitton, originating from France, topped the list with a brand value of USD 124,273 million.

- Another French brand, Hermès, followed with a value of USD 80,323 million.

- Chanel, also from France, held the third position with a brand value of USD 53,021 million. Italian brand Gucci was valued at USD 37,887 million.

- Other notable French brands included Dior, valued at USD 10,534 million, and Cartier, with a brand value of USD 10,110 million.

- Rolex, from the United Kingdom, had a brand value of USD 9,042 million. Saint Laurent, also known as Yves Saint Laurent and originating from France, was valued at USD 6,805 million.

- Tiffany & Co., from the United States, held a brand value of USD 6,718 million, while Italian brand Prada was valued at USD 5,642 million.

- These valuations underscore the significant economic impact and prestigious status of these leading luxury brands in the global market.

(Source: Statista)

Leading 10 Luxury Brands Most Trusted by Consumers Worldwide

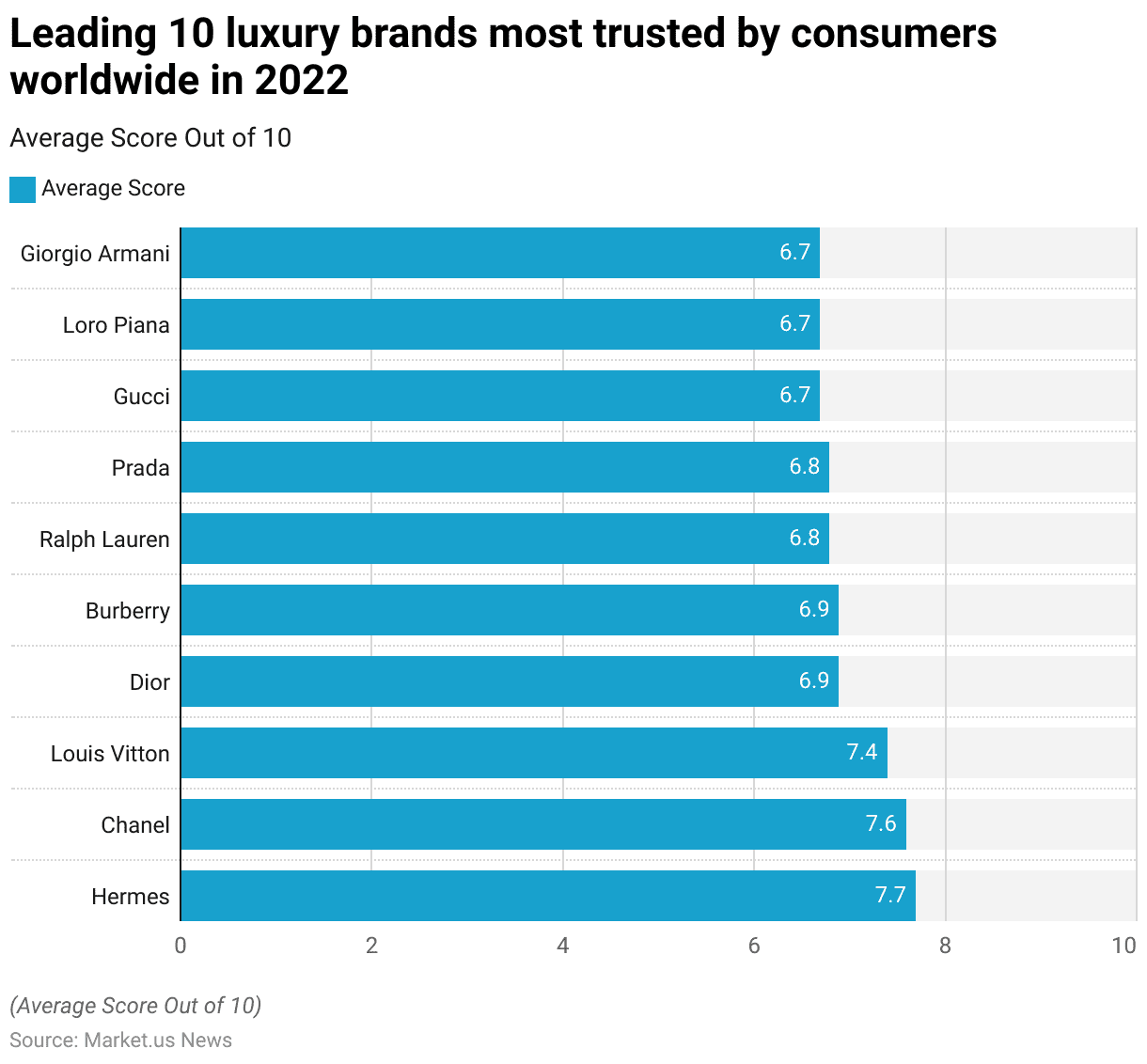

- In 2022, the most trusted luxury brands worldwide were ranked based on consumer trust, with scores reflecting their reliability and reputation.

- Hermès led the list with an average score of 7.7 out of 10, followed closely by Chanel with a score of 7.6.

- Louis Vuitton secured the third position with a score of 7.4.

- Dior and Burberry both achieved a score of 6.9, indicating strong consumer confidence.

- Ralph Lauren and Prada each garnered a score of 6.8, while Gucci, Loro Piana, and Giorgio Armani all received a score of 6.7.

- These scores highlight the high level of trust consumers place in these leading luxury brands, underscoring their esteemed positions in the global market.

(Source: Statista)

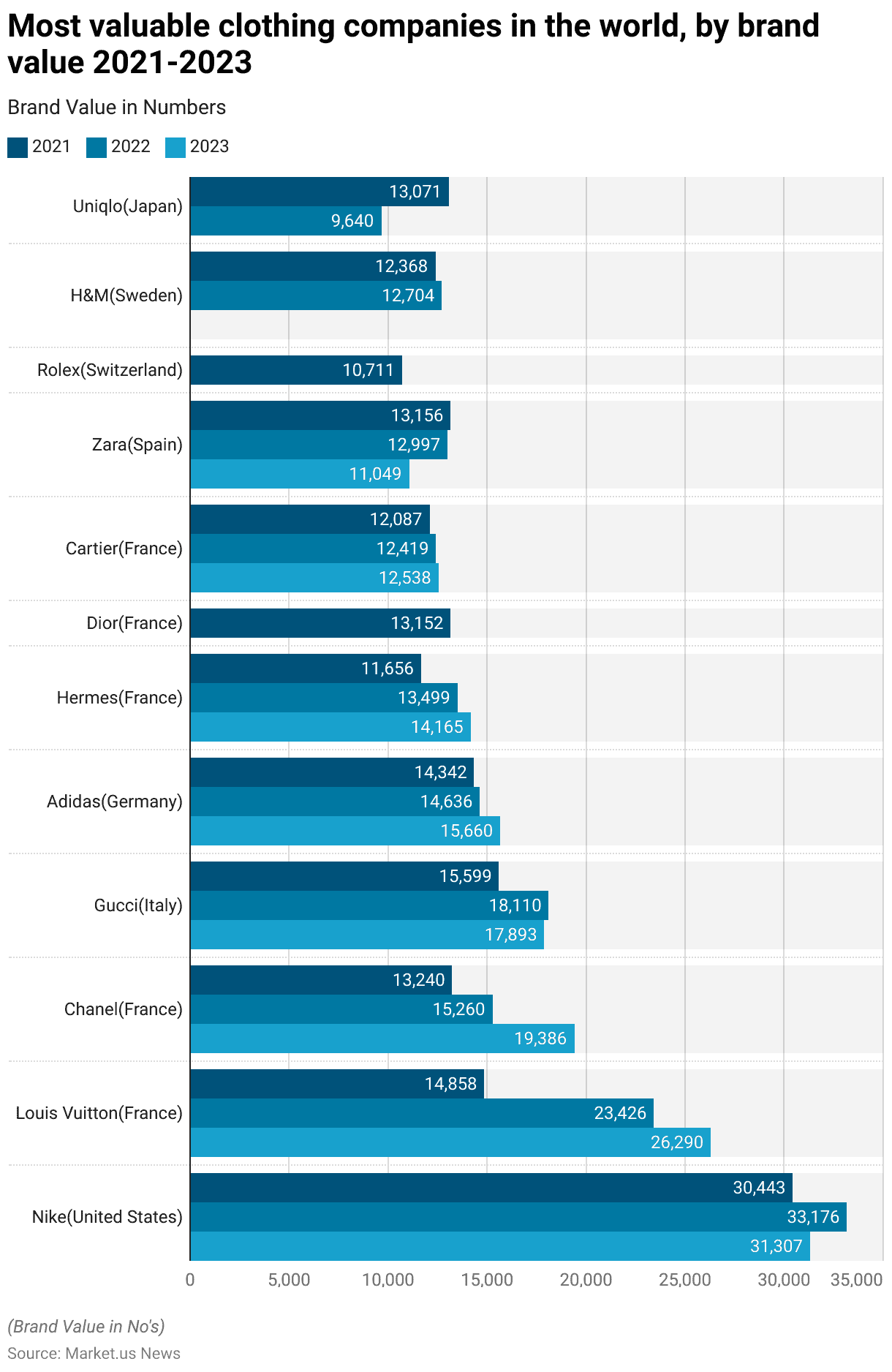

Most Valuable Clothing Companies in The World – By Brand Value

Major Brands

- Between 2021 and 2023, the ranking of the most valuable clothing and decorated apparel brands globally, based on brand value, highlighted significant fluctuations and growth.

- Nike, originating from the United States, consistently held the top position, with its brand value increasing from USD 30,443 million in 2021 to USD 33,176 million in 2022 before slightly declining to USD 31,307 million in 2023.

- Louis Vuitton from France demonstrated remarkable growth, with its brand value rising from USD 14,858 million in 2021 to USD 23,426 million in 2022 and further to USD 26,290 million in 2023.

- Chanel, also from France, saw its brand value increase from USD 13,240 million in 2021 to USD 15,260 million in 2022 and significantly to USD 19,386 million in 2023. Italy’s Gucci experienced growth from USD 15,599 million in 2021 to USD 18,110 million in 2022, with a slight decrease to USD 17,893 million in 2023.

- German brand Adidas showed a steady rise in brand value, from USD 14,342 million in 2021 to USD 14,636 million in 2022, reaching USD 15,660 million in 2023.

- Hermès, another French brand, increased its brand value from USD 11,656 million in 2021 to USD 13,499 million in 2022 and further to USD 14,165 million in 2023.

Other Brands

- Dior, also from France, had a brand value of USD 13,152 million in 2023.

- Cartier, yet another French brand, saw minor fluctuations with values of USD 12,087 million in 2021, USD 12,419 million in 2022, and USD 12,538 million in 2023.

- Spanish brand Zara experienced a decrease in brand value from USD 13,156 million in 2021 to USD 12,997 million in 2022 and significantly to USD 11,049 million in 2023.

- Swiss brand Rolex had a brand value of USD 10,711 million in 2023.

- Swedish brand H&M’s brand value remained relatively stable, from USD 12,368 million in 2021 to USD 12,704 million in 2022.

- Japanese brand Uniqlo saw a significant decrease in brand value from USD 13,071 million in 2021 to USD 9,640 million in 2022.

- These figures reflect the dynamic nature of the global apparel market and the varying fortunes of leading brands over the three years.

(Source: Statista)

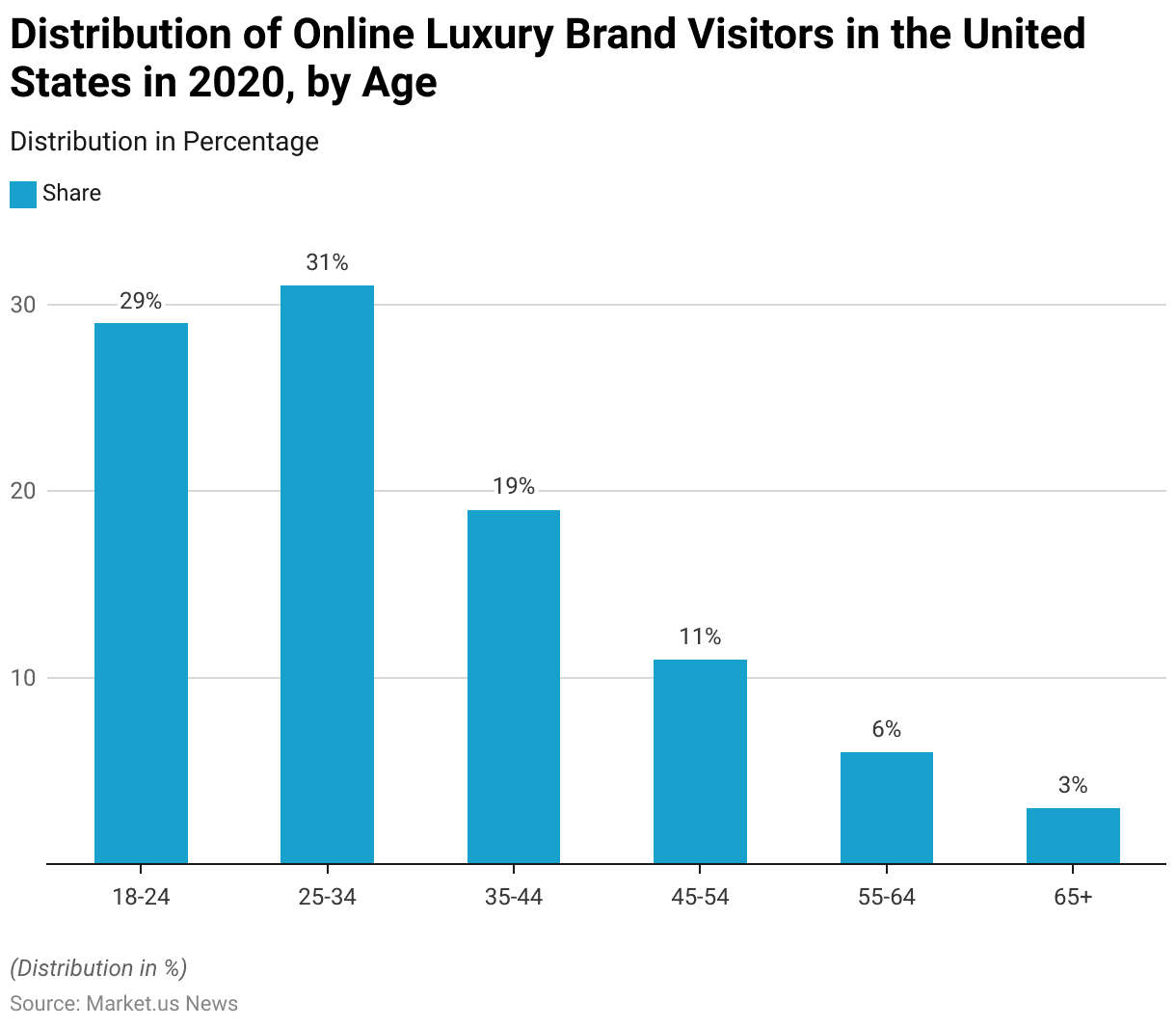

Demographic Insights of Luxury Goods Consumers Statistics

By Age

- In 2020, the distribution of online luxury brand visitors in the United States varied significantly across different age groups.

- The largest share of visitors came from the 25-34 age group, accounting for 31% of the total online audience.

- This was closely followed by the 18-24 age group, which comprised 29% of visitors.

- The 35-44 age group represented 19% of online luxury brand visitors.

- Those aged 45-54 accounted for 11%, while the 55-64 age group made up 6% of the audience.

- The smallest share of visitors, 3%, was from the 65 and older age group.

- This distribution indicates a strong preference for online luxury shopping among younger consumers.

(Source: Statista)

By Gender

- Women are increasingly embracing luxury purchases as symbols of personal and professional achievement, with a significant portion spending £50k+ annually, surpassing their male counterparts by 10%.

- Motivations such as signaling success (35%) and self-reward (33%) drive these purchases.

- Nearly two-thirds (62%) buy luxury items primarily for themselves, driven by the desire for self-indulgence and moments of happiness.

- Quality, craftsmanship, and durability define luxury for over 40% of women, who are also drawn to special promotions (40%), overseas luxury travel shopping (35%), and commemorating milestones (31%).

- Despite fewer personal purchases, men are 13% more likely to boast about their buys. At the same time, women favor the marketing strategies of Gucci and Chanel over competitors like Dior, Louis Vuitton, and Rolex.

(Source: Havas Media Network)

Consumer Purchasing Behavior and Trends

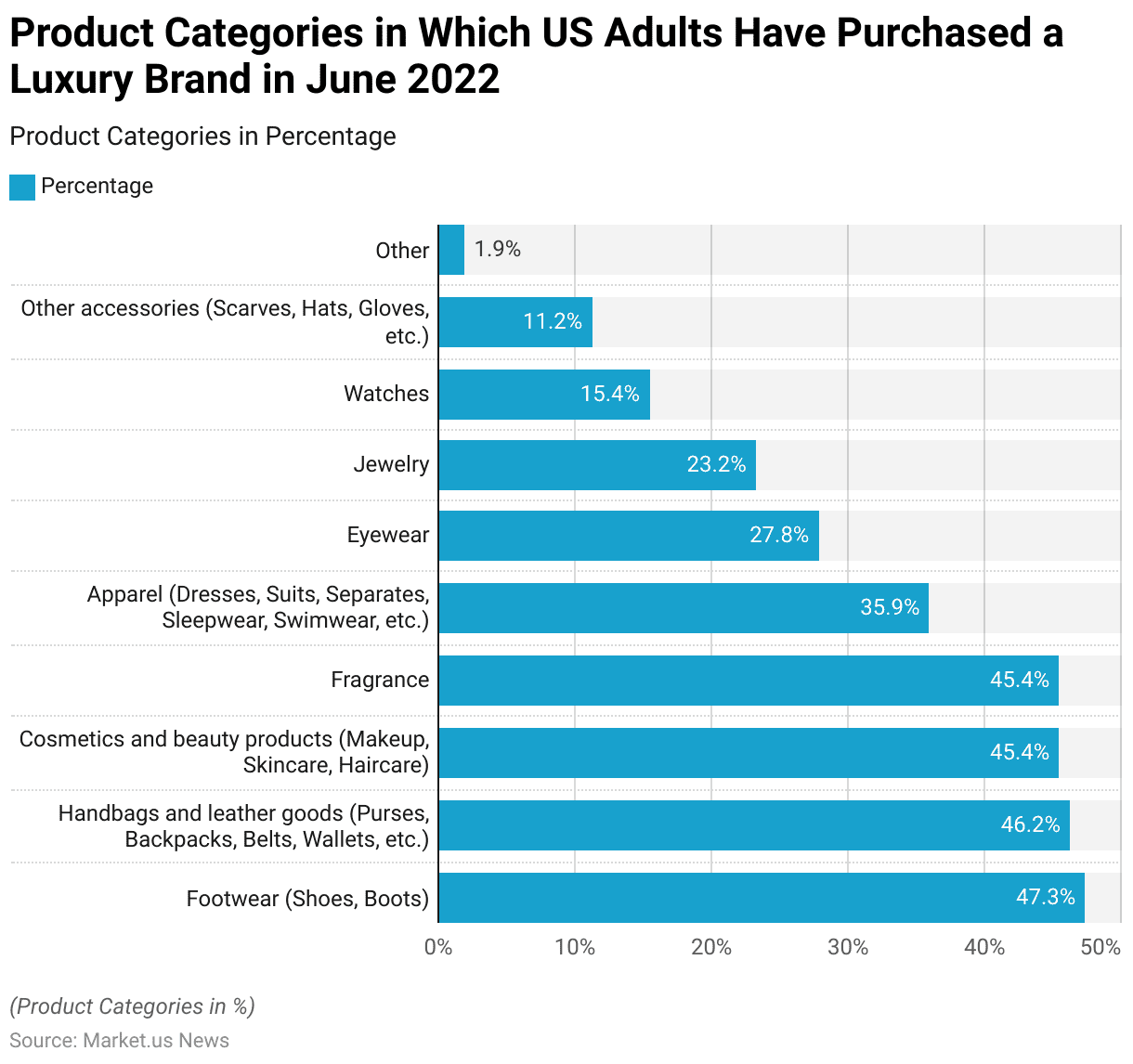

Popular Product Categories for Luxury Products

- In June 2022, US adults displayed a diverse range of preferences when purchasing luxury brands across various product categories.

- The most popular category was Luxury Footwear, including luxury shoes and boots, with 47.3% of respondents having made a purchase.

- Leather Handbags and leather goods, such as purses, backpacks, belts, and wallets, followed closely with 46.2%.

- Cosmetics and beauty products, encompassing makeup, skincare, and haircare, along with fragrances, each attracted 45.4% of respondents.

- Luxury apparel, which includes dresses, suits, separates, sleepwear, and swimwear, was purchased by 35.9% of luxury consumers.

- Eyewear was chosen by 27.8%, while jewelry was purchased by 23.2% of respondents.

- Watches were a less common luxury purchase, with 15.4% of respondents, followed by other accessories, such as scarves, hats, and gloves, at 11.2%.

- A small portion of respondents, 1.9%, indicated purchases in other unspecified categories.

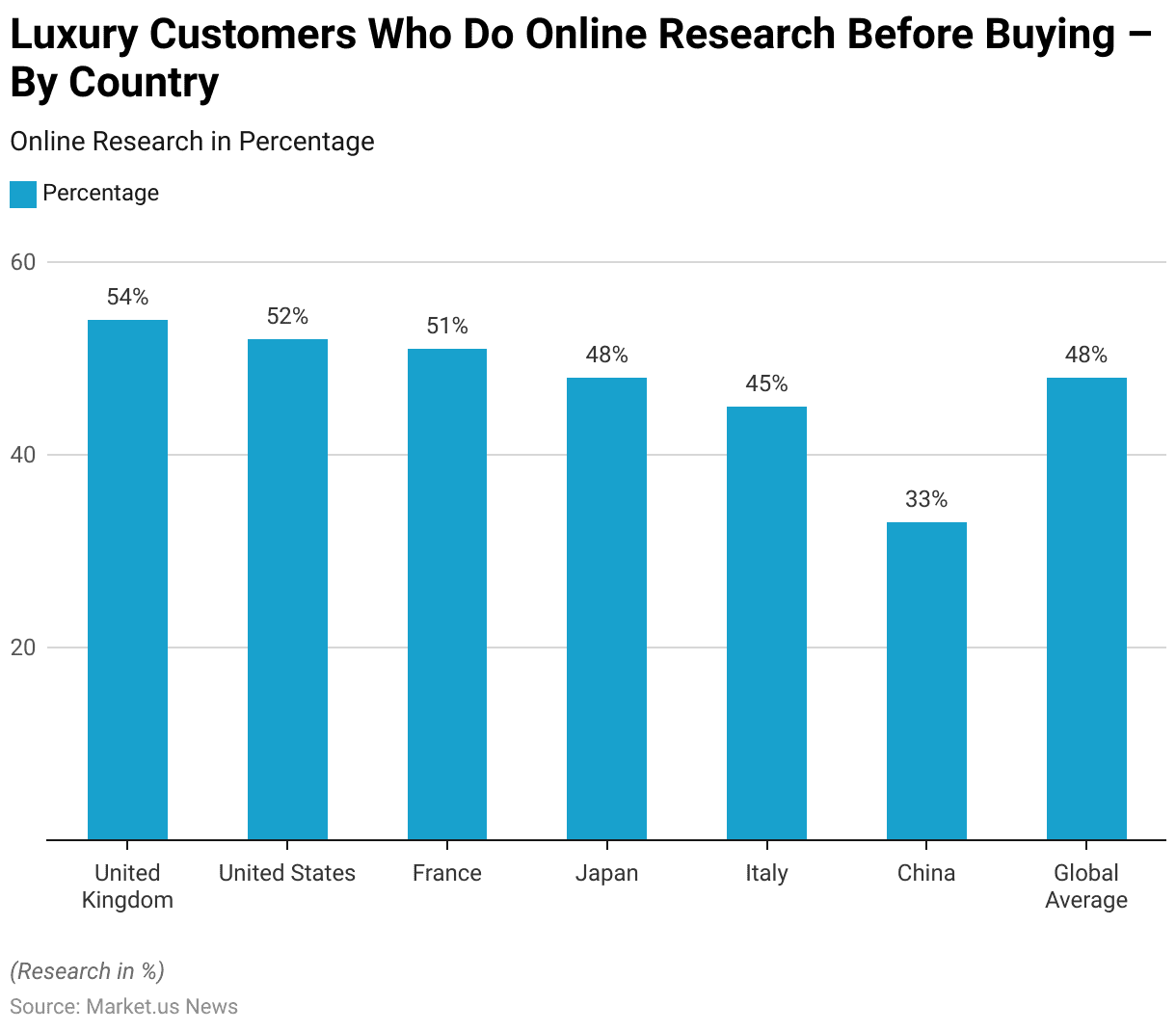

Luxury Customers Who Do Online Research Before Buying – By Country

- In the context of luxury shopping, a significant portion of customers engage in online research before making a purchase.

- In the United Kingdom, 54% of respondents indicated they conduct online research before buying luxury goods.

- This trend is closely mirrored in the United States, where 52% of luxury consumers research online before purchasing.

- In France, 51% of respondents follow this practice, while in Japan and Italy, the figures are 48% and 45%, respectively.

- China shows a lower percentage, with 33% of luxury customers conducting online research before buying.

- On a global scale, the average stands at 48%, highlighting the importance of online information and reviews in the luxury purchasing decision process.

(Source: Mckinsey)

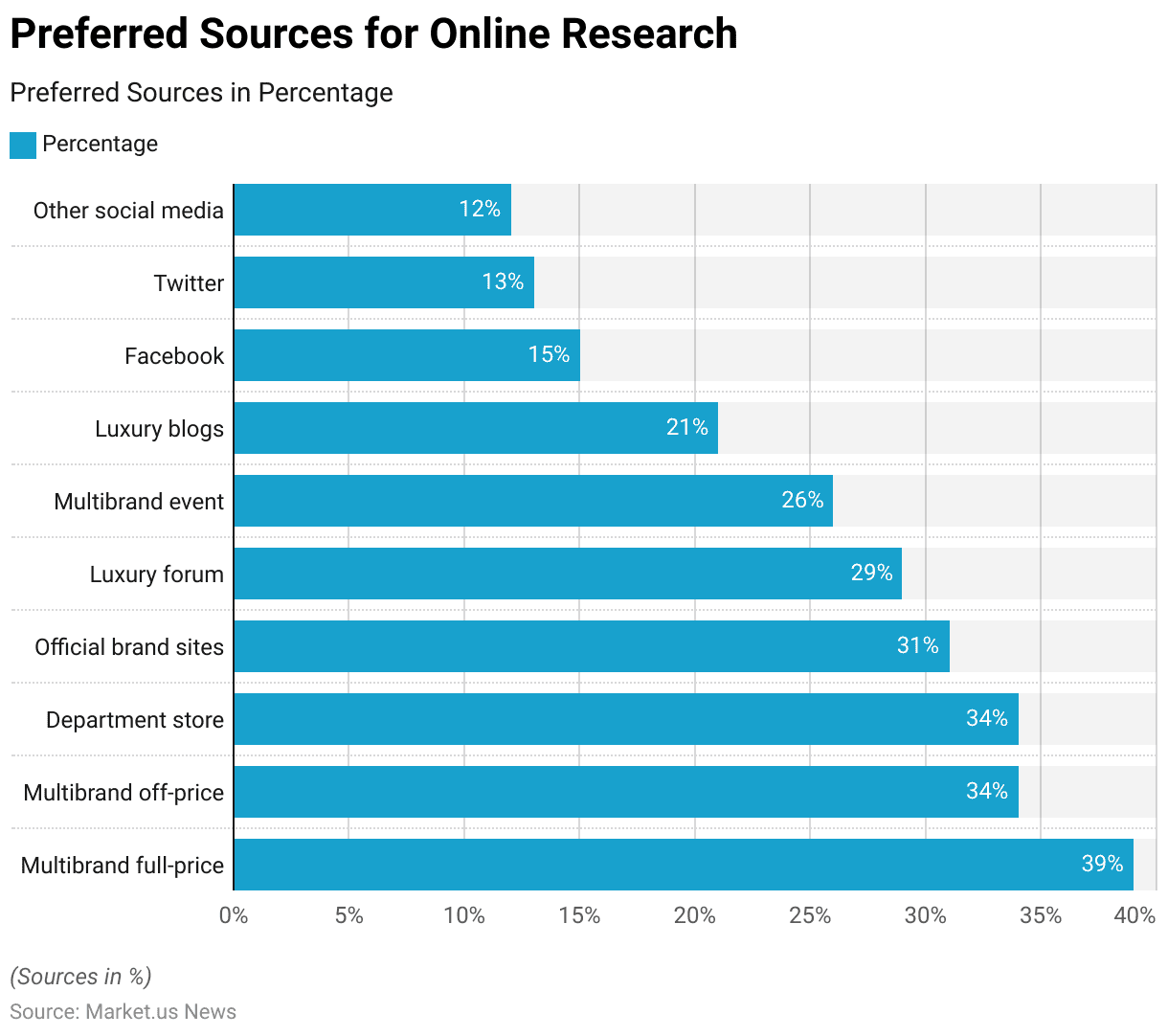

Preferred Sources for Online Research

- When conducting online research before purchasing luxury goods, consumers exhibit a preference for various sources.

- Multi-brand full-price websites are the most favored, with 39% of respondents indicating they use these platforms for their research.

- Multi-brand off-price websites and department stores are also popular, each preferred by 34% of respondents.

- Official brand sites attract 31% of luxury consumers for their research needs.

- Luxury forums are utilized by 29% of respondents, while multi-brand events are preferred by 26%.

- Luxury blogs serve as a research source for 21% of respondents.

- Social media platforms are less favored, with Facebook being used by 15%, Twitter by 13%, and other social media platforms by 12% of respondents.

- This distribution highlights the diverse range of sources luxury consumers rely on for information and insights before making a purchase.

(Source: Mckinsey)

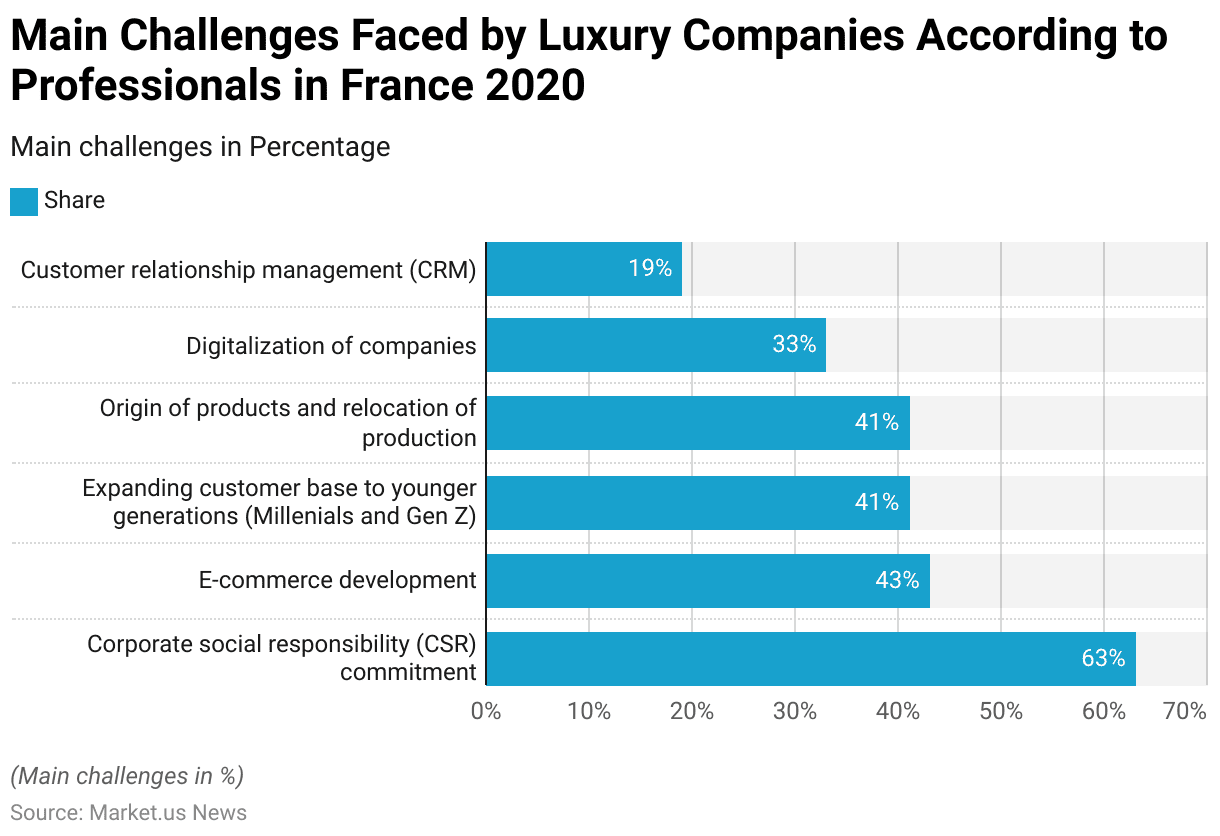

Challenges Faced by the Luxury Goods Industry Statistics

- In 2020, luxury companies in France faced several key challenges, as identified by industry professionals.

- The most significant challenge was the commitment to corporate social responsibility (CSR), highlighted by 63% of respondents.

- The development of e-commerce was also a major concern, with 43% of professionals recognizing it as a critical issue.

- Expanding the customer base to include younger generations, specifically Millennials and Gen Z, and addressing the origin of products and relocation of production were each cited by 41% of respondents.

- Digitalization of companies was noted as a challenge by 33% of respondents, while customer relationship management (CRM) was identified by 19% of professionals.

- These challenges underscore the evolving landscape and priorities within the luxury sector in France.

(Source: Statista)

Laws and Regulations for Luxury Goods Statistics

- The luxury goods industry is subject to various laws and regulations that differ by country. Impacting everything from import-export practices to sustainability commitments.

- In the United States, the Bureau of Industry and Security (BIS) has imposed strict export controls on luxury goods to countries such as Russia and Belarus. Requiring licenses for exports and re-exports to these nations due to geopolitical tensions.

- Similarly, the European Union has expanded its sanctions against Russia, banning the export of EU-made luxury items exceeding €300. Including high-value products like designer clothing, accessories, pet accessories and vehicles.

- In France, luxury brands must navigate stringent corporate social responsibility (CSR) requirements, emphasizing sustainability and ethical sourcing.

- These regulations aim to ensure transparency in the supply chain and reduce environmental impact. Reflecting growing consumer demand for responsible luxury. Additionally, digitalization and e-commerce development are critical areas. Companies are required to comply with data protection laws and online sales regulations.

- China, a significant market for luxury goods, has implemented strict import regulations. Including high tariffs and rigorous customs procedures, to protect domestic industries. The country also focuses on anti-counterfeiting measures to protect brand integrity and intellectual property rights.

- Overall, luxury goods companies must stay abreast of varying international laws and regulations. Which requires careful navigation to maintain compliance and sustain global operations. This complex regulatory landscape necessitates robust legal strategies and adaptive business practices to thrive in diverse markets.

(Source: Baker Mckenzie, Euro News, ICLG)

Recent Developments

Acquisitions and Mergers:

- LVMH acquires Tiffany & Co.: In early 2023, LVMH completed its $15.8 billion acquisition of Tiffany & Co. This acquisition is intended to enhance LVMH’s portfolio in the high-end jewelry market and expand its presence in the United States.

- Kering acquires Richard Mille: Kering acquired a 40% stake in Richard Mille, a luxury watchmaker, for $400 million in mid-2023. This strategic investment aims to strengthen Kering’s position in the luxury watch segment.

New Product Launches:

- Gucci’s Sustainable Collection: In late 2023, Gucci launched a new sustainable luxury collection made from eco-friendly materials and utilizing ethical production practices. This collection aims to appeal to environmentally conscious consumers.

- Louis Vuitton’s High Jewelry Collection: Louis Vuitton introduced a new high jewelry collection in early 2024, featuring unique designs and rare gemstones. This launch aims to solidify its position in the luxury jewelry market.

Funding:

- Chanel invests $1 billion in Sustainability: In 2023, Chanel committed $1 billion to sustainability initiatives over the next five years. This funding will support projects aimed at reducing the environmental impact of its production processes and sourcing sustainable materials.

- Hermès secures $500 million for Expansion: Hermès raised $500 million in early 2024 to expand its manufacturing facilities and increase production capacity to meet the growing demand for its luxury goods.

Technological Advancements:

- AI and Personalization: Luxury brands are increasingly using AI to personalize the shopping experience. AI-driven analytics help brands understand consumer preferences and tailor their marketing and product offerings accordingly.

- Virtual Reality (VR) Showrooms: Advances in VR are enabling luxury brands to create virtual showrooms, allowing customers to explore and purchase products from the comfort of their homes. This technology is enhancing the online shopping experience.

Market Dynamics:

- Growth in Luxury Goods Market: The global luxury goods market is projected to grow at a CAGR of 6.4% from 2023 to 2028, driven by increasing disposable incomes, the rise of digital luxury shopping, and growing demand from emerging markets.

- Rise of Second-Hand Luxury: The second-hand luxury market is growing rapidly, with consumers increasingly seeking sustainable and affordable luxury options. This trend is supported by platforms specializing in pre-owned luxury goods.

Regulatory and Strategic Developments:

- Ethical Sourcing Regulations: Governments and industry bodies are implementing stricter regulations around the ethical sourcing of materials, such as diamonds and exotic skins, to ensure transparency and sustainability in the luxury goods supply chain.

- Luxury Brands’ Sustainability Goals: Many luxury brands are setting ambitious sustainability goals. Such as carbon neutrality and zero waste, to align with consumer expectations and regulatory requirements.

Research and Development:

- Innovative Materials: R&D efforts are focusing on developing innovative materials for luxury goods, such as lab-grown diamonds and bio-fabricated leather, to meet the demand for sustainable and ethical products.

- Luxury Fashion and Technology Integration: Researchers are exploring the integration of technology with luxury fashion, such as wearable tech and smart fabrics, to create unique and functional luxury items.

Conclusion

Luxury Goods Statistics – The luxury goods market is a dynamic and evolving sector known for high-quality, exclusive products that command luxury and premium prices.

Despite challenges such as maintaining brand exclusivity, ensuring sustainability, and navigating complex international regulations, the industry continues to thrive.

Key brands like Louis Vuitton, Hermès, and Chanel lead in market value and consumer trust. The rise of e-commerce and the influence of younger generations, including Millennials and Gen Z, are transforming market dynamics.

Emphasizing corporate social responsibility and sustainable practices has become crucial. Aligning with the values of socially conscious consumers. The sector’s future success depends on innovation, adaptability, and strong consumer engagement.

FAQs

Luxury goods are high-end products that are often characterized by superior quality, exclusivity, and high price points. They include items such as designer clothing, high-end jewelry, luxury cars, and premium cosmetics.

Luxury goods are typically expensive due to their high-quality materials, craftsmanship, brand prestige, and limited production. The cost also reflects the brand’s marketing, exclusivity, and the perceived value associated with owning such items.

The luxury goods market has evolved significantly, especially with the rise of digital technology. E-commerce, social media marketing, and the importance of younger consumer demographics. Millennials and Gen Z have transformed how luxury brands operate and engage with customers.

Luxury goods companies face challenges such as maintaining brand exclusivity while expanding reach and adapting to digital transformation. Ensuring corporate social responsibility (CSR), combating counterfeiting, and navigating international trade regulations.

Regulations impact the luxury goods market by imposing standards on product quality, sustainability practices, and trade. For instance, the US and EU have strict export controls and sanctions affecting where luxury goods can be sold. Companies must also comply with CSR requirements and anti-counterfeiting laws to maintain brand integrity.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)