Table of Contents

Market Overview

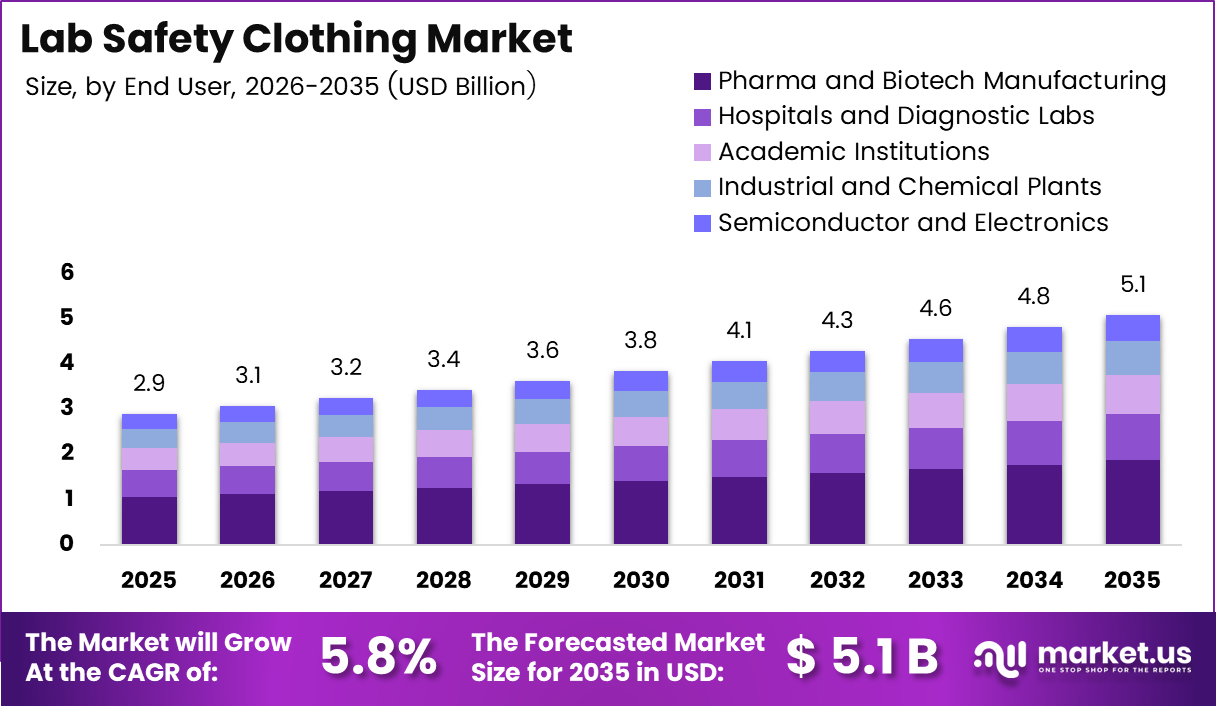

The global laboratory protective clothing market size is expected to reach USD 5.1 billion by 2035. This growth starts from a base value of USD 2.9 billion in 2025. Consequently, the market will expand at a compound annual growth rate (CAGR) of 5.8% during the forecast period 2026 to 2035. Laboratory protective clothing forms a critical safety layer for research personnel worldwide.

Laboratory protective clothing includes specialized garments such as lab coats, coveralls, and chemical-resistant suits. These products shield workers from chemical, biological, thermal, and physical hazards in research environments. Moreover, industrial laboratories and cleanrooms rely on these garments for daily operations. The clothing serves as the first defense against workplace accidents and contamination incidents.

Pharmaceutical labs, biotechnology research centers, and academic institutions drive primary adoption. Healthcare diagnostic facilities and semiconductor cleanrooms also demand high-performance protective apparel. Each sector requires specific barrier properties tailored to unique hazard profiles. Therefore, manufacturers develop specialized product lines for distinct industry requirements and safety standards.

Data-Driven Insights for Smarter Business Decisions:Explore the Full Report

Advanced fabric technologies now integrate antimicrobial treatments and fluid-repellent finishes into protective garments. Smart textile innovations enable real-time contamination monitoring and exposure tracking for enhanced worker safety. Additionally, breathable barrier materials reduce heat stress during extended wear periods. These technological improvements directly increase user comfort and protocol compliance rates across laboratory settings.

Stringent occupational safety regulations from agencies like OSHA and EU directives compel mandatory protective clothing adoption. Organizations face substantial penalties for non-compliance, driving consistent procurement cycles. Moreover, regular safety audits verify proper garment usage in accredited facilities. Consequently, regulatory pressure creates a stable, predictable demand foundation supporting long-term market growth trajectories globally.

According to the University of Washington’s Chemistry Department, 100% cotton lab coats provide superior flame protection compared to synthetic alternatives. Oregon State University confirms that barrier lab coats typically feature 100% polyester fronts with 65/32 polyester-cotton blend back panels. These material specifications directly influence purchasing decisions and product development strategies. Manufacturers prioritize certified fabrics that meet established academic safety research findings.

Key Takeaways

- Global Laboratory Protective Clothing Market projected to reach USD 5.1 Billion by 2035 from USD 2.9 Billion in 2025

- Market expected to grow at a CAGR of 5.8% during the forecast period 2026-2035

- Lab Coats and Jackets segment dominates with 32.7% market share in 2025

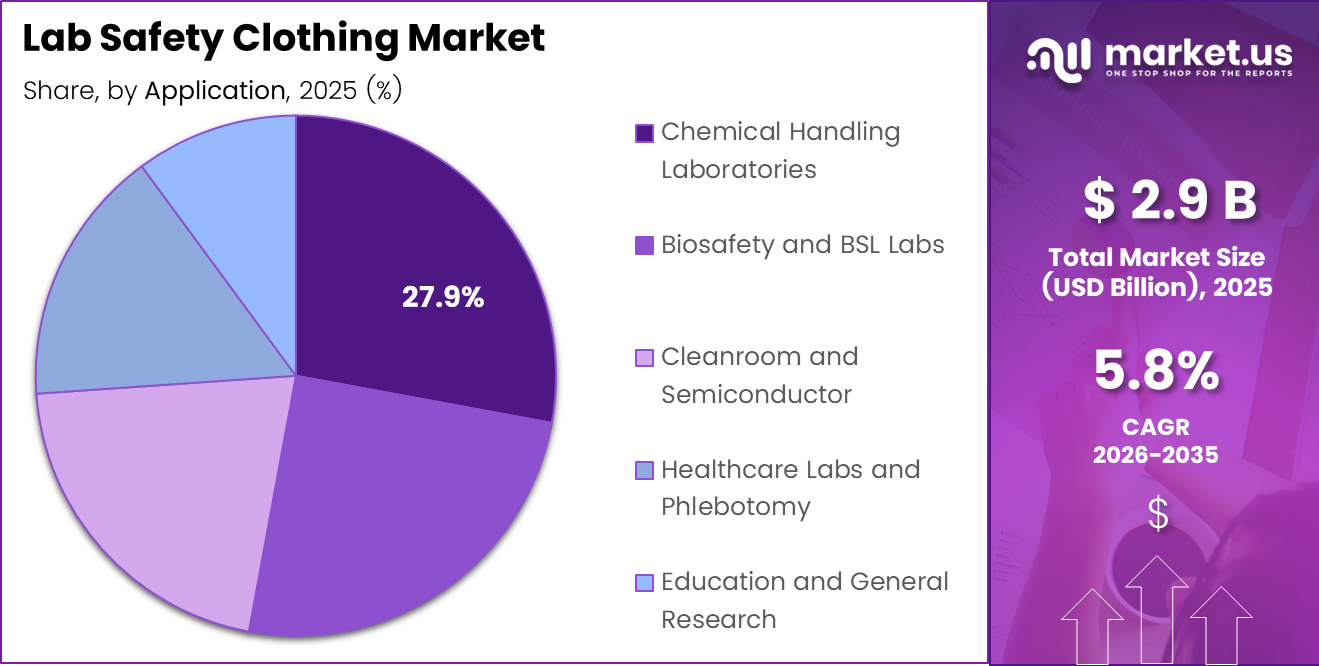

- Chemical Handling Laboratories application holds 27.9% market share

- Pharma and Biotech Manufacturing leads end-user segment with 36.8% share

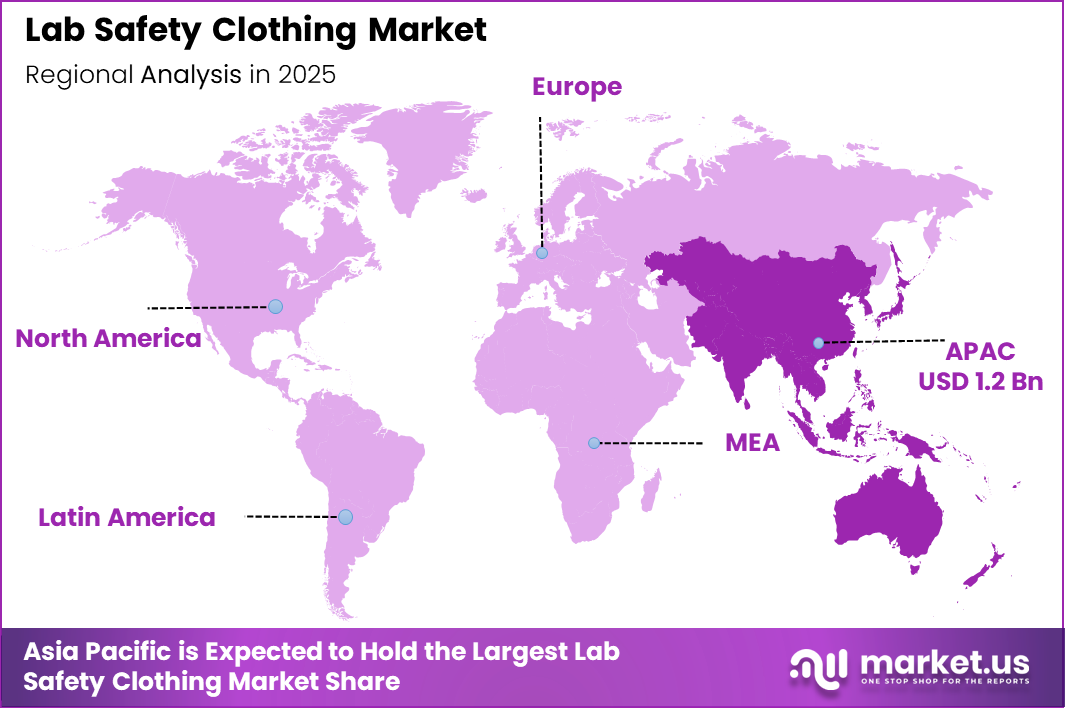

- Asia Pacific dominates regional market with 42.80% share, valued at USD 1.2 Billion

- North America and Europe represent significant markets driven by stringent safety regulations

- Rising adoption of antimicrobial and flame-resistant fabric technologies reshapes product development

Market Segmentation Overview

Lab Coats and Jackets dominate the product type segment with a 32.7% market share in 2025. This dominance reflects widespread adoption across academic, pharmaceutical, and research institutions globally. Their versatility and ease of use make them the most fundamental protective apparel. Consequently, consistent demand arises from basic safety protocols in virtually all laboratory settings.

Coveralls and protective suits gain traction in high-containment laboratories requiring comprehensive body protection. These full-body garments provide superior barrier performance for cleanroom operations and biosafety applications. Moreover, increasing biosafety level requirements in pharmaceutical manufacturing accelerate adoption rates. Therefore, specialized end-users increasingly invest in these advanced protective solutions.

Chemical Handling Laboratories lead the application segment with a 27.9% share in 2025. These facilities demand robust apparel to safeguard personnel against corrosive and toxic chemical exposure. Regulatory compliance frameworks mandate certified chemical-resistant garments, driving consistent procurement cycles. Additionally, industrial chemistry research expansion sustains strong demand growth across this critical segment.

Data-Driven Insights for Smarter Business Decisions:Explore the Full Report

Biosafety and BSL labs require specialized clothing for handling infectious agents across different safety levels. Containment protocols necessitate barrier garments preventing pathogen transmission during extended procedures. Moreover, expanding vaccine development facilities increase demand for high-performance biosafety apparel. Consequently, validated microbiological barrier properties become essential purchasing criteria for these end-users.

Pharma and Biotech Manufacturing leads the end-user segment with a 36.8% share in 2025. These facilities maintain rigorous contamination control standards throughout drug development processes. Personnel safety regulations mandate certified protective garments across cleanrooms and quality control laboratories. Therefore, substantial and recurring protective clothing consumption characterizes this dominant end-user segment.

Hospitals and diagnostic labs constitute another major end-user segment requiring diverse protective apparel. Healthcare facilities prioritize fluid-resistant and antimicrobial garments to protect staff from infectious material exposure. Moreover, increasing diagnostic testing volumes in emerging markets sustain steady demand growth. Consequently, both reusable and disposable protective clothing solutions remain essential for clinical laboratory operations.

Drivers

Regulatory agencies worldwide enforce increasingly stringent laboratory safety standards requiring certified protective apparel. Organizations face substantial penalties for non-compliance, compelling mandatory personal protective equipment adoption. Moreover, regular safety audits verify proper clothing usage, ensuring sustained procurement cycles. Consequently, regulatory pressure creates a stable demand foundation supporting consistent market growth across developed and emerging economies.

Workplace safety incidents involving chemical burns and pathogen exposure drive employer liability concerns significantly. Organizations mitigate legal exposure through comprehensive protective clothing programs exceeding minimum regulatory standards. Additionally, corporate safety culture evolution prioritizes employee well-being, translating into higher-quality protective apparel investments. Therefore, liability risk management becomes a powerful driver for premium protective clothing adoption across all laboratory types.

Use Cases

Pharmaceutical quality control laboratories use chemical-resistant suits to protect analysts during potency testing of active ingredients. These garments prevent dermal absorption of potent compounds that could cause systemic health effects. Moreover, the suits enable safe handling of carcinogenic materials during routine quality assurance procedures. Consequently, pharmaceutical companies mandate certified barrier protection for all QC personnel handling hazardous drug substances.

Academic teaching laboratories utilize durable, flame-resistant lab coats for undergraduate chemistry and biology practical sessions. Students performing open-flame experiments and corrosive reagent handling require basic but reliable thermal protection. Additionally, these coats withstand frequent laundering cycles necessary for multi-user educational environments. Therefore, universities prioritize cost-effective, reusable protective clothing that balances safety compliance with budget constraints.

Major Challenges

Advanced protective clothing incorporating specialized fabrics like Nomex aramid and chemical-resistant polymers commands premium pricing. Budget-constrained laboratories, particularly in academic and small research settings, struggle to afford certified high-performance garments. Moreover, organizations requiring frequent garment replacement face escalating operational expenses. Consequently, cost barriers drive substitution toward lower-specification alternatives that may compromise safety performance and increase injury risks.

Protective laboratory garments often sacrifice comfort and breathability to achieve required barrier properties and flame resistance. Extended wear periods cause heat stress, restricted mobility, and reduced productivity among laboratory personnel. Additionally, uncomfortable garments reduce user compliance with mandatory protective apparel protocols during complex procedures. Therefore, comfort limitations create resistance to consistent protective clothing usage, undermining safety objectives despite strict regulatory requirements.

Business Opportunities

Rapid expansion of academic research institutions across emerging Asian, Latin American, and Middle Eastern economies drives substantial market growth. Government investments in scientific research infrastructure and pharmaceutical manufacturing capabilities accelerate laboratory construction significantly. Moreover, multinational corporations establish R&D facilities in cost-advantaged regions. Consequently, emerging market laboratory proliferation represents a significant growth opportunity for protective clothing suppliers seeking geographic diversification.

Environmental sustainability concerns drive adoption of reusable protective clothing systems designed for multiple laundering cycles. Durable garments reduce waste generation and operational costs compared to single-use alternatives substantially. Furthermore, recyclable fabric technologies and closed-loop manufacturing processes appeal to environmentally conscious organizations. Therefore, manufacturers developing eco-friendly protective apparel solutions gain competitive differentiation in procurement decisions favoring sustainable products.

Regional Analysis

Asia Pacific dominates the laboratory protective clothing market with 42.80% share, valued at USD 1.2 billion in 2025. Rapid pharmaceutical manufacturing expansion across China, India, and Southeast Asia drives this regional leadership. Government initiatives promoting biotechnology research and chemical manufacturing create substantial protective clothing demand. Moreover, cost-competitive production capabilities attract multinational laboratory operations, accelerating regional market expansion through increased facility construction and personnel hiring.

North America maintains significant market presence supported by stringent OSHA regulations and extensive pharmaceutical research activities. The region emphasizes premium protective clothing solutions meeting rigorous safety certifications and performance standards. Additionally, Europe demonstrates strong demand driven by comprehensive EU safety directives and robust pharmaceutical manufacturing bases. Therefore, both mature markets provide stable revenue streams through established laboratory safety cultures and consistent replacement cycles.

Recent Developments

- July 2024 – Ansell Limited completed acquisition of Kimberly-Clark’s Personal Protective Equipment Business for approximately USD 640 Million, expanding laboratory protective clothing portfolio across pharmaceutical and healthcare segments

- December 2025 – NSA strengthened safety solutions through acquisition of NASCO Industries, marking its third strategic acquisition in 2025 and eighteenth overall transaction

Conclusion

The global laboratory protective clothing market demonstrates robust growth driven by regulatory enforcement and infrastructure expansion. Stringent occupational safety standards mandate certified protective apparel across research and industrial facilities worldwide. Moreover, workplace incident prevention concerns compel organizations to invest in quality garments. Consequently, the market maintains a stable growth trajectory supported by fundamental safety requirements that cannot be delegated or eliminated.

Lab coats and jackets dominate product segments with a 32.7% share, while chemical handling laboratories lead applications at 27.9%. Asia Pacific commands regional leadership with 42.80% market share valued at USD 1.2 billion. Additionally, pharmaceutical and biotech manufacturing represents the largest end-user segment at 36.8%. These dominance patterns reflect concentrated demand drivers across specific laboratory types and geographic regions.

Manufacturers must address comfort limitations and cost barriers to capture remaining market potential across academic and emerging economy segments. Technological advancements in breathable barrier fabrics and sustainable reusable designs present significant differentiation opportunities. Therefore, companies investing in ergonomic innovation and eco-friendly production processes will capture premium market share. The market is projected to reach USD 5.1 billion by 2035.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)