Market Overview

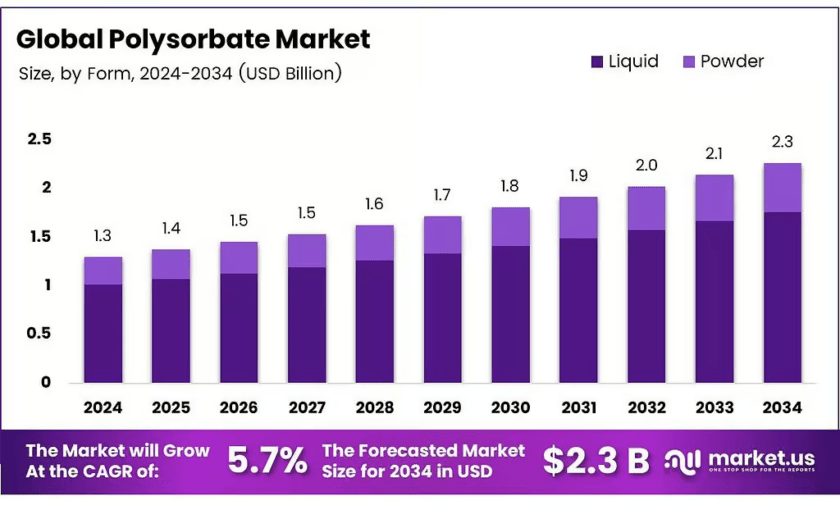

New York, NY – May 25, 2026 – The Global Polysorbate Market size is expected to reach USD 2.3 billion by 2034. This represents growth from USD 1.3 billion in 2024. Consequently, the market will expand at a compound annual growth rate (CAGR) of 5.7% from 2025 to 2034.

Polysorbate acts as a stabilizing molecule that influences nanocrystal performance. Additionally, it serves as a P-glycoprotein (P-gp) inhibitor. Therefore, this nonionic surfactant improves drug delivery by reversing P-gp-mediated efflux in pharmaceutical applications. Manufacturers use polysorbates as emulsifiers, solubilizers, and stabilizers across three major industries. These include cosmetic, pharmaceutical, and food products. For example, polysorbate 80 remains a long-time component in vaccines and biological drugs.

Polysorbates derive from pegylated sorbitan esterified with fatty acids. The numerical designation, such as 20, 40, 60, or 80, indicates the lipophilic fatty acid group. Moreover, polysorbate 80 contains 20–24 PEG units with a molecular weight of 880–1056 g/mol. These excipients enhance solubility in vaccines like Hepatitis B, influenza, and HPV. For instance, AZD1222 and several COVID-19 candidates contain polysorbate 80. However, allergic reactions are mostly linked to medications, while vaccine-related cases remain rare.

Key Takeaways

- The Global Polysorbate Market is projected to grow from USD 1.3 billion in 2024 to USD 2.3 billion by 2034 at a CAGR of 5.7%.

- Liquid form dominated the market in 2024 with a 77.8% share, favored for rapid dissolution and stability in pharmaceutical and food applications.

- The Food and Beverages segment led applications in 2024 with 38.9% share, driven by emulsification in ice creams, dressings, and convenience foods.

- Asia-Pacific held the largest regional share in 2024 at 47.9%, USD 0.6 billion, fueled by growth in pharmaceutical, food, and cosmetics manufacturing.

➤ Download Exclusive Sample Of This Premium Report (Including Full TOC, Table & Figures)- https://market.us/report/polysorbate-market/request-sample/

By Form Analysis

In 2024, Liquid Form held a dominant market position with a 77.8% share. This form excels as an emulsifier in pharmaceuticals and food, blending seamlessly into formulations. Manufacturers prefer it for quick dissolution and stability, driving widespread adoption across multiple industries. The powder form, while smaller, gains traction in dry mixes and specialized uses. It offers superior shelf life and precise dosing, ideal for instant foods and detergents.

Liquid polysorbates enhance product textures and ensure consistent performance. Their liquidity simplifies handling, which boosts efficiency in production lines. Therefore, liquid polysorbates remain the top choice for most manufacturers seeking reliable emulsification and solubilization in their products.

By Application Analysis

In 2024, Food and Beverages held a dominant market position with a 38.9% share. Polysorbates stabilize emulsions in ice creams and dressings, preventing separation. This boosts appeal in convenience foods, meeting consumer needs for creamy textures without altering taste profiles. Cosmetics and personal care utilize polysorbates for smooth emulsions in lotions and shampoos. They enable oil-water blending, improving spreadability and feel on skin.

The pharmaceuticals segment thrives on polysorbates’ solubilizing prowess in drug delivery. It prevents aggregation in vaccines, ensuring efficacy during storage and transportation. Though not leading, this segment grows with healthcare demands, remaining vital for oral and injectable formulations.

Regional Analysis

In 2024, Asia-Pacific held a dominant 47.9% share, valued at USD 0.6 billion. The region’s leadership stems from expanding pharmaceutical, food, and cosmetics manufacturing sectors. Countries like China and India have become central hubs for biologics production and vaccine formulation.

Government investments in vaccine infrastructure drive regional growth. Additionally, rapid growth in processed and convenience foods increases polysorbate adoption as an emulsifier. Consequently, Asia-Pacific will likely retain its leading position over the coming decade, supported by expanding healthcare and food-processing industries.

Drivers

The surge in demand for polysorbates stems from explosive vaccine and biologic drug growth. These products depend on non-ionic surfactants like polysorbate 20 or 80 to maintain protein stability. In 2024, UNICEF distributed 2.787 billion vaccine doses across 99 countries, reaching 45% of the world’s children under five.

Global DTP3 vaccination coverage hit 85% in 2024, yet 14.3 million children remained unvaccinated. This gap highlights the need for reliable scaling through durable formulations. Therefore, manufacturers require consistent polysorbate supplies that withstand challenging logistics and maintain product integrity throughout distribution.

Use Cases

Polysorbates serve as critical stabilizers in biologic drug products, particularly monoclonal antibodies and high-concentration protein therapies. These surfactants prevent protein aggregation in vials and prefilled syringes. Consequently, pharmaceutical companies rely on polysorbates to ensure patient safety and product efficacy.

Food manufacturers use polysorbates as emulsifiers in bakery, confectionery, and dairy applications. They prevent ingredient separation in ice creams, dressings, and processed foods. This application improves product texture and shelf life, meeting consumer expectations for consistent quality and appealing mouthfeel.

Business Opportunities

Manufacturers can develop ultra-low-impurity, plant-derived polysorbate grades for sensitive biologics and vaccine lines. The FDA recorded 18 biosimilar approvals in 2024, an all-time high. This expands the number of protein drugs requiring high-purity surfactants, creating significant opportunities for specialty excipient suppliers.

Vaccine makers now disclose exact excipient loads per dose, raising the bar on oxidative byproducts. The USP monograph for polysorbate 80 embeds a Peroxide Value test, signaling industry expectations for oxidation risk management. Suppliers offering low-peroxide grades and robust change-control will capture market share.

Major Challenges

Polysorbate degradation through hydrolysis and oxidation complicates manufacturing and regulatory compliance. A recent survey found that about 69% of companies reported hydrolysis in at least one product, while 63% reported oxidation. This degradation releases free fatty acids, forming particles that raise safety concerns.

Raw material lots must be tightly controlled for peroxide value, with limits like ≤10 mEq/kg in some pharmacopeial standards. Without rigorous control, manufacturers risk batch failures and shorter shelf life. Consequently, companies face real costs and operational burdens to maintain consistent quality throughout production.

Top Key Players in the Market

- Croda International PIC

- BASF SE

- Evonik Industries AG

- Solvay SA

- Stepan Company

- Others

Conclusion

The global polysorbate market continues its steady growth, driven by vaccine expansion and biologic drug development. Manufacturers face challenges from degradation risks but can capitalize on opportunities in ultra-pure grades. Asia-Pacific leads regional demand, while liquid form and food applications dominate their respective segments. Market players must prioritize quality control and regulatory compliance to maintain a competitive advantage in this evolving landscape.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)