Market Overview

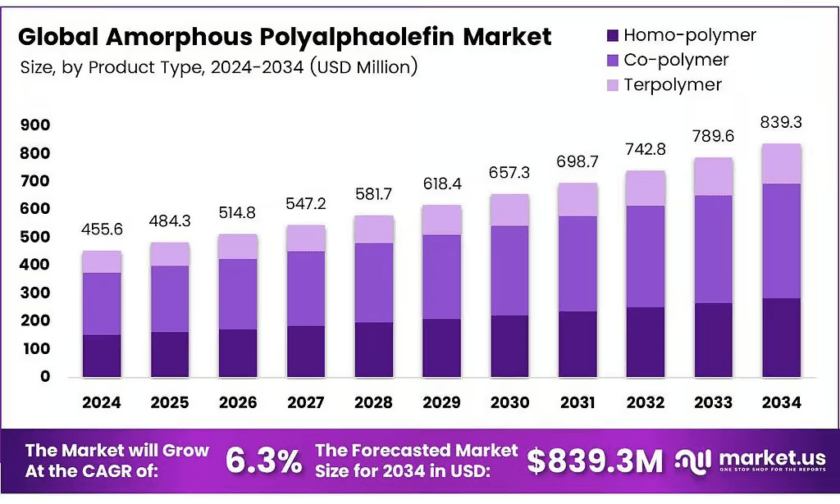

New York, NY – May 25, 2026 – The Global Amorphous Polyalphaolefin Market size will grow from USD 455.6 million in 2024 to USD 839.3 million by 2034. Consequently, the market will expand at a 6.3% CAGR during the forecast period from 2025 to 2034. This steady growth reflects rising industrial adoption across multiple sectors.

APAO represents a low molecular weight amorphous plastic material with high compatibility for asphalt binder. Manufacturers value this material for its flexibility, recyclability, and reduced glass transition temperature. Moreover, APAO dissolves completely in asphalt binder when the content stays below 6 wt.%.

Research demonstrates that APAO-modified binder processes at 165 degrees Celsius. This temperature stands significantly lower than the 180 degrees Celsius required for the SBS-modified binder. Consequently, producers achieve better efficiency without needing shearing equipment or stabilizers.

APAO enhances elastic properties while reducing temperature susceptibility in modified binders. Additionally, this material improves high-temperature performance, storage stability, and aging resistance. When combined with waste tire rubber or SBS, APAO delivers superior results compared to standalone modifiers.

Key Takeaways

- The Global Amorphous Polyalphaolefin Market will grow from USD 455.6 million in 2024 to USD 839.3 million by 2034 at a 6.3% CAGR.

- Co-polymer segment dominated in 2024 with 48.8% share, driven by flexibility, adhesion, and impact strength in hot-melt packaging applications.

- Polyalphaolefin Copolymers held 44.9% market share in 2024, excelling in wettability, heat resistance, and durability for packaging and adhesives.

- The Paper and Packaging application led in 2024 with a 33.2% share, fueled by APAO’s moisture-resistant seals and e-commerce-driven demand.

- Asia-Pacific commanded 43.9% global share in 2024, valued at USD 200.0 million, led by strong demand in packaging, automotive, and hygiene sectors for hot-melt adhesives.

➤ Access the Exclusive Sample Report Featuring Full TOC, Data Tables & Figures – https://market.us/report/amorphous-polyalphaolefin-market/request-sample/

Market Segmentation

By Product Type

In 2024, Co-polymer held a dominant market position with a 48.8% share. This segment thrives because co-polymers blend seamlessly, boosting flexibility and adhesion in hot melt applications. Manufacturers favor co-polymers for superior impact strength, driving widespread use in packaging. Consequently, demand surges as industries seek reliable bonding solutions.

Homo-polymer follows closely, offering consistent performance across various substrates. This product type excels in uniform structure, ensuring reliable adhesion without processing complexity. Industries adopt homo-polymer for cost-effective bonding in woodworking and hygiene products. Thus, homo-polymer sustains steady demand through its dependable qualities.

By Chemical Composition

In 2024, Polyalphaolefin Copolymers held a dominant market position with a 44.9% share. These copolymers shine in diverse applications, providing excellent wettability and heat resistance. They integrate smoothly into adhesive formulations, enhancing overall product durability. The packaging and adhesives sectors widely embrace these copolymers for efficient production.

Polyalphaolefin Homopolymers provide cost-effective adhesion with uniform consistency across applications. These materials bond effectively to various surfaces, supporting woodworking and basic hygiene product needs. Their simple composition reduces processing costs, appealing to budget-conscious manufacturers. Hence, homopolymers maintain strong relevance in everyday industrial uses.

By Application

In 2024, Paper and Packaging held a dominant market position with a 33.2% share. APAO excels in this sector by offering robust moisture-resistant seals for cartons and labels. The e-commerce boom amplifies the need for secure, durable packaging solutions. Consequently, APAO secures bonds swiftly while reducing material waste.

Personal Hygiene benefits from APAO’s gentle adhesion in diapers and sanitary products. This material ensures user comfort without causing skin irritation, aligning with rising hygiene awareness. Manufacturers integrate APAO for leak-proof designs, boosting consumer trust in branded products. Therefore, this segment expands steadily with global population growth.

Regional Analysis

In 2024, the Asia-Pacific led the global amorphous polyalphaolefin market with a 43.9% share valued at USD 200.0 million. This dominance stems from strong demand in packaging, automotive, and hygiene sectors for durable low-temperature hot-melt adhesives. Key drivers include heavy investments in sustainable packaging and infrastructure across China, India, Japan, and South Korea.

Europe follows as a significant market driven by strict packaging waste regulations. The European Commission’s Packaging and Packaging Waste Regulation requires all packaging to be fully recyclable. This regulatory push favors APAO because the material is polyolefin-based and bonds well to PE and PP films without contaminating recycling streams. Consequently, European brand owners redesign packs toward mono-material solutions that work seamlessly with APAO adhesives.

Drivers

Strong regulatory momentum toward recyclable mono-polymer packaging drives APAO demand significantly. Under the European Commission’s PPWR, all new packaging must be 100% recyclable, with recyclability rates below 70% disqualifying products. As converters redesign packaging toward mono-polymer structures, APAO adhesives gain preference because they are polyolefin-based and compatible with PE and PP systems.

Additionally, rising e-commerce activity accelerates APAO adoption in packaging applications. Online retail demands secure, moisture-resistant seals that maintain integrity during transit and storage. APAO-based hot-melt adhesives provide these properties while supporting recyclability goals. Therefore, both regulatory pressure and commercial demand create strong tailwinds for market expansion.

Use Cases

In mono-material recyclable packaging, APAO serves as the preferred adhesive for polyolefin film structures. Brand owners redesign flexible packaging to use single polymer types, simplifying sorting and recycling processes. APAO adhesives do not contaminate these recycling streams because they belong to the same polyolefin family. Consequently, converters choose APAO to meet sustainability targets without sacrificing bond strength.

In automotive manufacturing, APAO provides low-odor, heat-resistant bonding for interior assemblies and nonwoven components. Vehicle producers require adhesives that withstand temperature fluctuations while maintaining structural integrity. APAO meets these demands while offering better processability than traditional SBS modifiers. Therefore, automotive suppliers increasingly specify APAO for interior trim and sound deadening applications.

Business Opportunities

Manufacturers can capitalize on the growing demand for mono-material packaging adhesives in European markets. As PPWR enforcement tightens, converters urgently need adhesive systems compatible with PE and PP recycling streams. Companies that develop specialized APAO grades for specific mono-material structures will capture significant market share. Building technical partnerships with packaging converters creates long-term supply relationships.

Producers can also expand into emerging Asian markets where packaging consumption grows rapidly. Urbanization and rising disposable incomes drive demand for consumer goods, electronics, and food packaging in China and India. APAO manufacturers can establish local production facilities to serve these price-sensitive markets cost-effectively. Additionally, offering technical support for application development differentiates suppliers from commodity producers.

Major Challenges

Volatile polyolefin feedstock prices create significant margin pressure for APAO producers. Propylene and alpha-olefin prices swing dramatically based on energy costs and refinery utilization rates. When supply tightens, manufacturers face higher raw material costs that cannot always be passed through to customers. Consequently, profit margins shrink, discouraging capacity expansion investments.

Energy-intensive production processes further strain APAO economics in high-cost regions. European Chemical Industry Council data shows capacity utilization fell to 74.1% due to competitive disadvantages versus the US, China, and the Middle East. Higher energy and feedstock costs in Europe create structural headwinds for specialty polyolefin adhesive producers. Therefore, manufacturers must locate facilities strategically to remain cost-competitive.

Top Key Players in the Market

- Qida Chemicals Co. Ltd.

- Ter Hell and Co. GMBH

- Exxonmobil Corporation

- Soltex

- Chevron Phillips Chemical

- Evonik Industries AG

- Ineos Oligomers

- REXtac LLC

- A S Harrison and Co. Pty Limited

Conclusion

The Global Amorphous Polyalphaolefin Market enters a growth phase driven by sustainable packaging regulations and expanding polyolefin substrate usage. APAO’s unique compatibility with recycling streams positions it as the adhesive of choice for mono-material packaging designs. Manufacturers that innovate specialized grades for emerging applications will capture significant value. However, feedstock volatility requires strategic sourcing and location decisions to maintain competitiveness.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)