Table of Contents

Market Overview

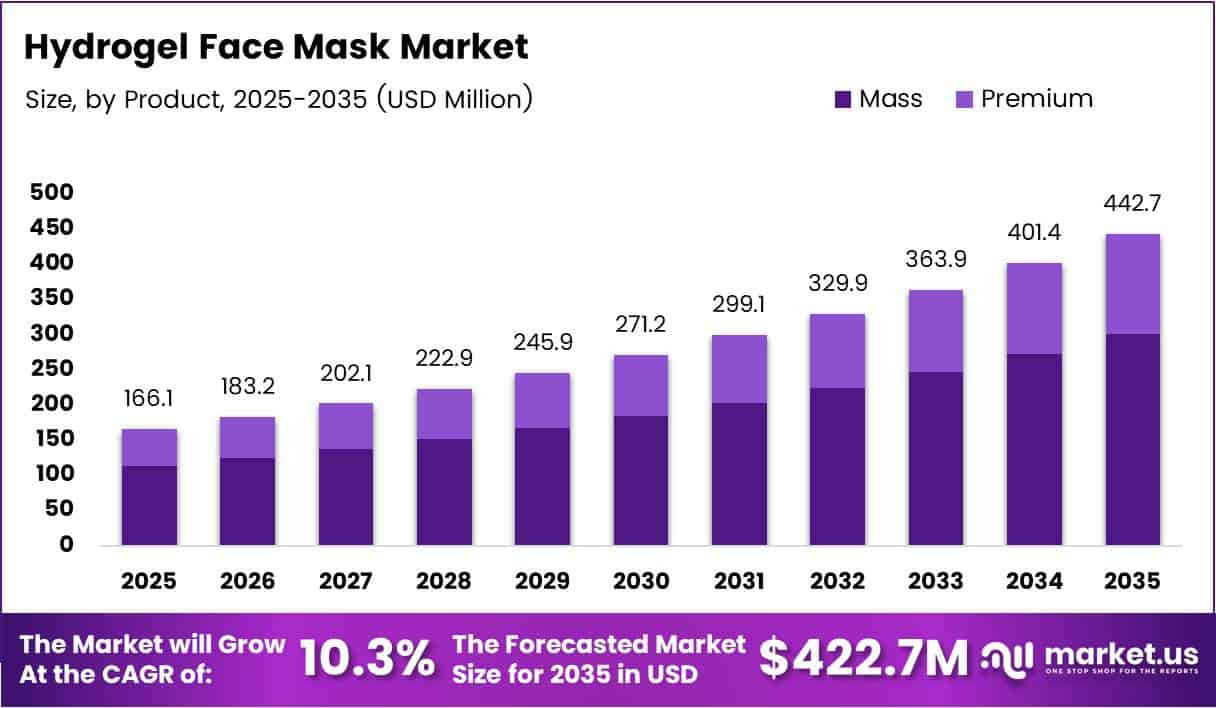

The global hydrogel face mask market size is expected to reach USD 442.7 million by 2035. This growth starts from a base value of USD 166.9 million in 2025. Consequently, the market will expand at a compound annual growth rate (CAGR) of 10.3% during the forecast period 2026 to 2035. Hydrogel face masks represent an advanced skincare delivery system gaining global consumer traction.

Hydrogel face masks use polymer-based gel matrices to deliver active ingredients deep into skin layers. These masks create occlusive barriers that enhance hydration retention and active ingredient penetration significantly. Moreover, the technology offers superior facial adherence compared to traditional sheet masks. Therefore, consumers experience better ingredient absorption and more visible results from regular use.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Consumer preference for intensive at-home spa treatments drives robust market expansion across all regions. Additionally, rising awareness about skin barrier health accelerates product adoption among millennials and Gen Z. Moreover, dermatology-backed formulations strengthen consumer confidence in premium hydrogel mask efficacy. Consequently, brands invest heavily in clinical testing to validate product claims and safety profiles.

Product innovation focuses on multi-sensory experiences including cooling effects and visible skin transformation. Manufacturers integrate aromatherapy benefits and instant radiance-boosting properties into new hydrogel formulations. Additionally, social media amplifies at-home treatment trends through before-after content sharing. Therefore, companies prioritize Instagram-worthy packaging and immediate visible results to drive repeat purchases.

Government regulations increasingly focus on cosmetic ingredient transparency and safety standards worldwide. Therefore, companies prioritize clean beauty formulations with fully disclosed ingredient lists. Additionally, regulatory frameworks in major markets mandate hypoallergenic testing for sensitive skin product claims. Consequently, compliance costs rise but consumer trust strengthens through verified safety documentation.

According to Nutriadvisor, hydrogel masks increase stratum corneum hydration by 40-60% immediately after application with effects lasting 24-48 hours. Moreover, clinical testing reveals these masks reduce transepidermal water loss by 25-35% for up to 72 hours post-treatment. Alibaba Product Insights confirms +39.1% hydration at 20 minutes and +22.4% retention after 2 hours. These statistics validate superior performance over conventional sheet mask technologies.

Key Takeaways

- Global Hydrogel Face Mask Market valued at USD 166.9 Million in 2025, projected to reach USD 442.7 Million by 2035

- Market grows at a CAGR of 10.3% during forecast period 2026-2035

- Mass segment dominates By Product category with 69.1% market share in 2025

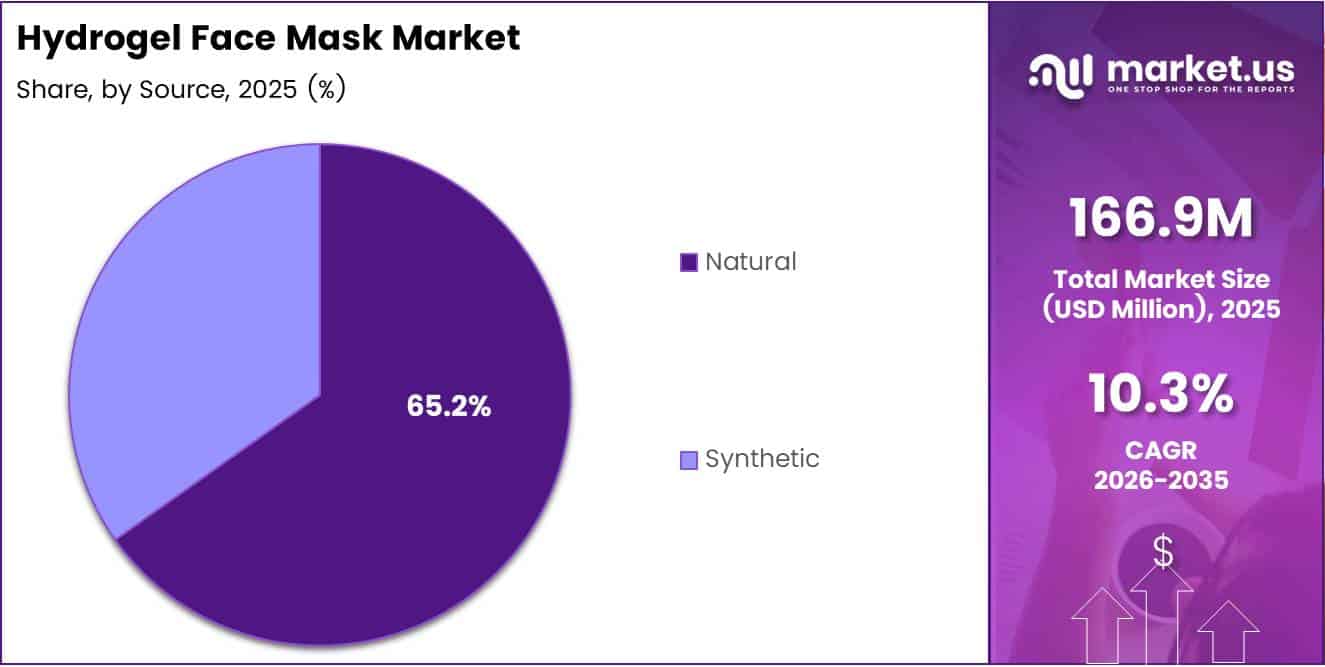

- Natural source segment leads with 65.2% share driven by clean beauty trends

- Skin Brightening application holds largest share at 56.7% reflecting consumer priorities

- Specialty Stores channel captures 34.9% distribution share in 2025

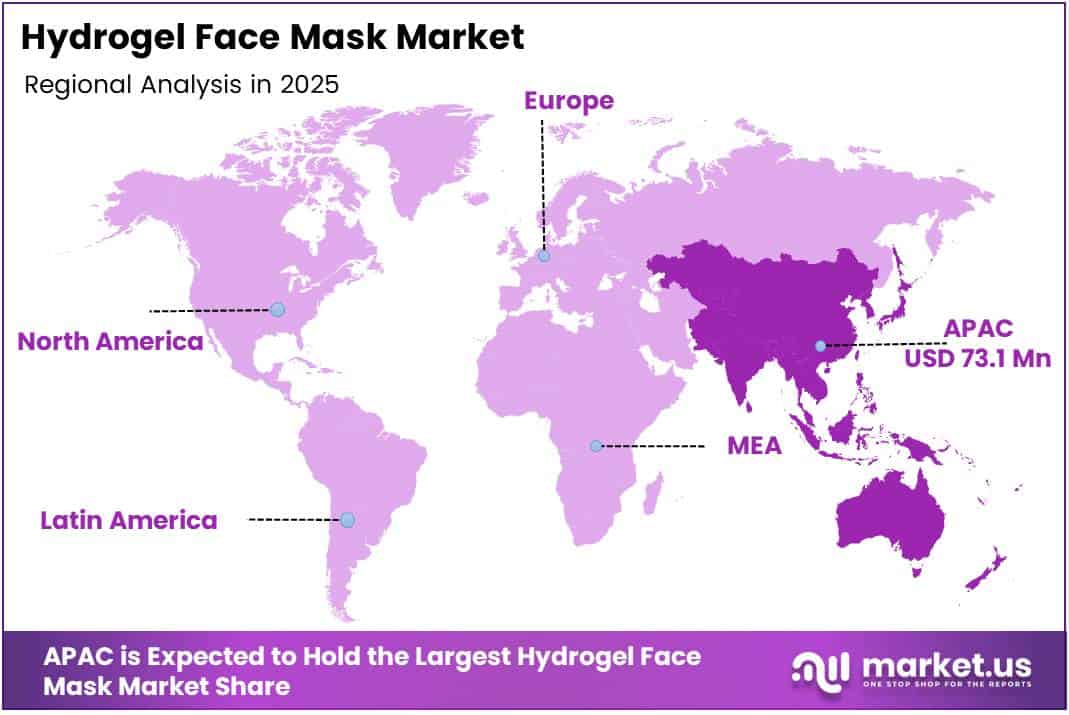

- Asia Pacific dominates regional landscape with 43.80% share valued at USD 73.1 Million

Market Segmentation Overview

The Mass segment dominates the product category with a 69.1% market share in 2025. This dominance reflects affordability and widespread retail availability across drugstores and supermarkets. Mass brands leverage extensive distribution networks to attract price-conscious consumers seeking effective skincare solutions. Consequently, product accessibility drives volume sales particularly in emerging markets where premium products remain unaffordable.

The Premium segment captures growing demand from affluent consumers prioritizing dermatologist-developed formulations. These products feature advanced actives like peptides, exosomes, and microbiome boosters for superior results. Additionally, premium brands invest heavily in clinical testing and luxury packaging innovation. Therefore, this segment commands higher margins despite lower volume penetration compared to mass alternatives.

Natural source products dominate the source segment with a 65.2% market share in 2025. The clean beauty movement drives consumer preference for plant-based and bio-derived hydrogel materials. Moreover, natural sources align perfectly with sustainability concerns and eco-conscious purchasing behavior. Consequently, brands increasingly reformulate existing products using bio-cellulose and algae-derived polymers instead of synthetic alternatives.

Dry skin dominates the skin type segment with a 37.4% market share in 2025. This segment benefits from hydrogel technology’s proven ability to increase epidermal water content significantly. Consumers with dry skin prioritize products offering long-lasting moisture retention beyond immediate application benefits. Therefore, brands formulate specialized hydrogels with hyaluronic acid and ceramides targeting this largest skin type segment.

Skin brightening dominates the application segment with a 56.7% market share in 2025. This segment addresses hyperpigmentation concerns through ingredients like vitamin C, niacinamide, and kojic acid. Moreover, brightening claims resonate strongly across Asian markets where fair skin preferences persist culturally. Consequently, brands prioritize melanin-inhibiting actives in hydrogel formulations to capture this substantial consumer demand.

Specialty stores lead distribution channels with a 34.9% market share in 2025. These outlets provide personalized skincare advice and demonstrate product benefits through sampling programs. Moreover, specialty retailers curate high-quality brands that build consumer trust through expert recommendations. Consequently, educated store staff drive conversions through targeted product suggestions matching individual skin concerns and preferences.

Drivers

Consumers increasingly replicate professional skincare experiences at home through advanced hydrogel mask technologies. This shift reflects changing lifestyle priorities and desire for convenient luxury self-care rituals without spa visits. Moreover, pandemic-era behaviors permanently altered consumer expectations for at-home treatment efficacy and convenience. Consequently, brands invest heavily in spa-quality formulations designed specifically for retail distribution rather than professional channels.

According to PubMed, hydrogel research output increased from approximately 350 publications in 2000 to 11,000 publications in 2024. This research expansion validates hydrogel efficacy and drives consumer confidence in product performance claims. Moreover, the scientific community’s growing interest accelerates technology transfer from academic research to commercial applications. Therefore, manufacturers benefit from continuous innovation streams supported by peer-reviewed efficacy evidence.

Use Cases

Dermatologists recommend hydrogel masks for post-procedure recovery following laser treatments and chemical peels. The cooling gel matrix reduces inflammation and redness while delivering calming ingredients like centella asiatica. Moreover, the occlusive barrier maintains hydration during critical healing windows when skin barrier function remains compromised. Consequently, medical aesthetics clinics stock hydrogel masks as take-home products for patient recovery protocols.

Frequent travelers use single-use hydrogel mask packets to combat in-flight dehydration and jet lag effects on skin. The sealed packaging prevents leakage during carry-on transport while providing instant hydration upon arrival. Moreover, compact size allows easy storage in personal item bags without occupying significant space. Therefore, airport duty-free shops and travel retailers feature hydrogel masks prominently in their beauty sections.

Major Challenges

Hydrogel mask manufacturing requires specialized polymer synthesis processes and controlled production environments. These technical requirements increase capital investment and per-unit production costs significantly compared to sheet masks. Moreover, bio-cellulose materials demand fermentation facilities and extended production timelines of several weeks. Consequently, retail prices remain elevated, limiting mass market penetration in price-sensitive regions and among budget-conscious consumers.

Raw material sourcing challenges affect production consistency and supply chain stability for natural hydrogel bases. Additionally, cold chain storage requirements for certain hydrogel formulations increase distribution expenses significantly. Therefore, smaller brands face substantial entry barriers due to minimum order quantities and specialized equipment investments. This cost-quality trade-off constrains market expansion velocity particularly in developing economies.

Business Opportunities

Expanding middle-class populations in tier-2 and tier-3 cities across emerging economies demonstrate increasing skincare expenditure. These secondary markets offer significant volume growth potential as disposable incomes rise steadily. Moreover, digital connectivity enables beauty education and product discovery beyond metropolitan areas through social media. Consequently, brands develop region-specific formulations and pricing strategies targeting these underserved urban populations.

According to PubMed, bio-based hydrogel superabsorbent systems demonstrate high water retention capacity while enabling active ingredient carrier functionality. This technological advantage supports product differentiation and compelling efficacy claims in crowded markets. Additionally, ingredient innovation drives premium positioning and margin expansion opportunities for forward-thinking manufacturers. Therefore, companies investing in proprietary hydrogel technologies capture sustainable competitive advantages.

Regional Analysis

Asia Pacific dominates the hydrogel face mask market with 43.80% share, valued at USD 73.1 million in 2025. The region’s consumers demonstrate strong affinity for innovative mask technologies and ingredient-focused formulations. Moreover, cultural emphasis on complexion perfection and multi-step skincare regimens drives frequent product usage. Consequently, regional brands like Amorepacific and TONYMOLY dominate through localized product development tailored to Asian beauty preferences.

North America experiences steady growth through clean beauty movement adoption and dermatologist-recommended product trust. Consumers prioritize ingredient transparency and clinical efficacy validation when selecting hydrogel masks. Additionally, Europe emphasizes sustainable packaging and natural ingredient sourcing aligned with strict cosmetic regulations. Therefore, both mature markets offer premium positioning opportunities for brands with verified safety profiles and environmental commitments.

Recent Developments

- November 2025 – Rini launched hydrating hydrogel face masks including Vitamin B12 hydrogel mask as part of its kids skincare line, expanding market reach into pediatric personal care segments with gentle formulations for young sensitive skin

- October 2025 – Rhode launched Peptide Eye Prep hydrogel eye patches formulated with caffeine and peptides, targeting under-eye concerns including dark circles, puffiness, and fine lines through targeted active ingredient delivery

- January 2026 – Elurea launched a long-wear hydrogel collagen mask formulated with kojic acid for skin brightening and extended wear performance, addressing consumer demand for multi-functional products combining hydration, brightening, and prolonged efficacy

Conclusion

The global hydrogel face mask market demonstrates robust growth driven by at-home spa treatment preferences and ingredient transparency demands. Strong CAGR of 10.3% reflects sustained consumer interest in advanced skincare delivery technologies. Moreover, scientific validation through increased research publications strengthens product credibility and adoption rates. Consequently, the market maintains positive momentum supported by fundamental shifts in beauty consumption behaviors.

Mass products dominate with 69.1% share, while natural source formulations lead at 65.2%. Skin brightening represents the largest application at 56.7%, with specialty stores as the primary distribution channel at 34.9%. Asia Pacific commands regional leadership with 43.80% share valued at USD 73.1 million. These dominance patterns reflect concentrated consumer priorities around affordability, natural ingredients, and visible brightening results.

Manufacturers must address production cost barriers while developing multi-functional products for time-constrained consumers. Emerging market expansion and biodegradable material innovation present significant growth opportunities for proactive companies. Therefore, brands investing in clinical validation and sustainable packaging will capture premium market share. The market is projected to reach USD 442.7 million by 2035.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)