Introduction

Fencing Statistics: Understanding fence basics is essential for anyone embarking on a fencing project. This involves selecting the right materials, such as wood for traditional charm or vinyl for low maintenance, and considering design elements like height and style.

Compliance with local regulations and obtaining necessary permits are crucial steps in ensuring adherence to zoning laws and property boundaries.

Maintenance, including regular cleaning and repairs, helps prolong the fence’s lifespan, while cost considerations encompass material and labor expenses.

Ultimately, integrating the fence seamlessly into the landscape enhances both its aesthetic appeal and functional utility.

Editor’s Choice

- The global fencing market revenue is projected to reach USD 53.01 billion by 2033.

- The global fencing market is dominated by several key players, with Ameristar Fence Products Incorporated leading with an 18% market share.

- North America leads the market, holding a substantial 34.0% share.

- The percentage of the population living in urban areas worldwide has shown a significant increase from 1950 to 2050, with varying trends across different country income groups.

- The longest fences and border walls around the globe vary significantly in length, with the Great Wall of China being the most extensive at 8,500 kilometers.

- The distribution of internal fence types on private and public lands reveals distinct preferences and usage patterns. On private lands, four-strand barbed wire fences are the most common, accounting for 338% of the total fences sampled.

- The Department of Homeland Security, through Customs and Border Protection (CBP), manages these projects with significant financial investments, such as the $1.375 billion allocated in fiscal year 2018 for border infrastructure.

Global Fencing Market Overview

Global Fencing Market Size Statistics

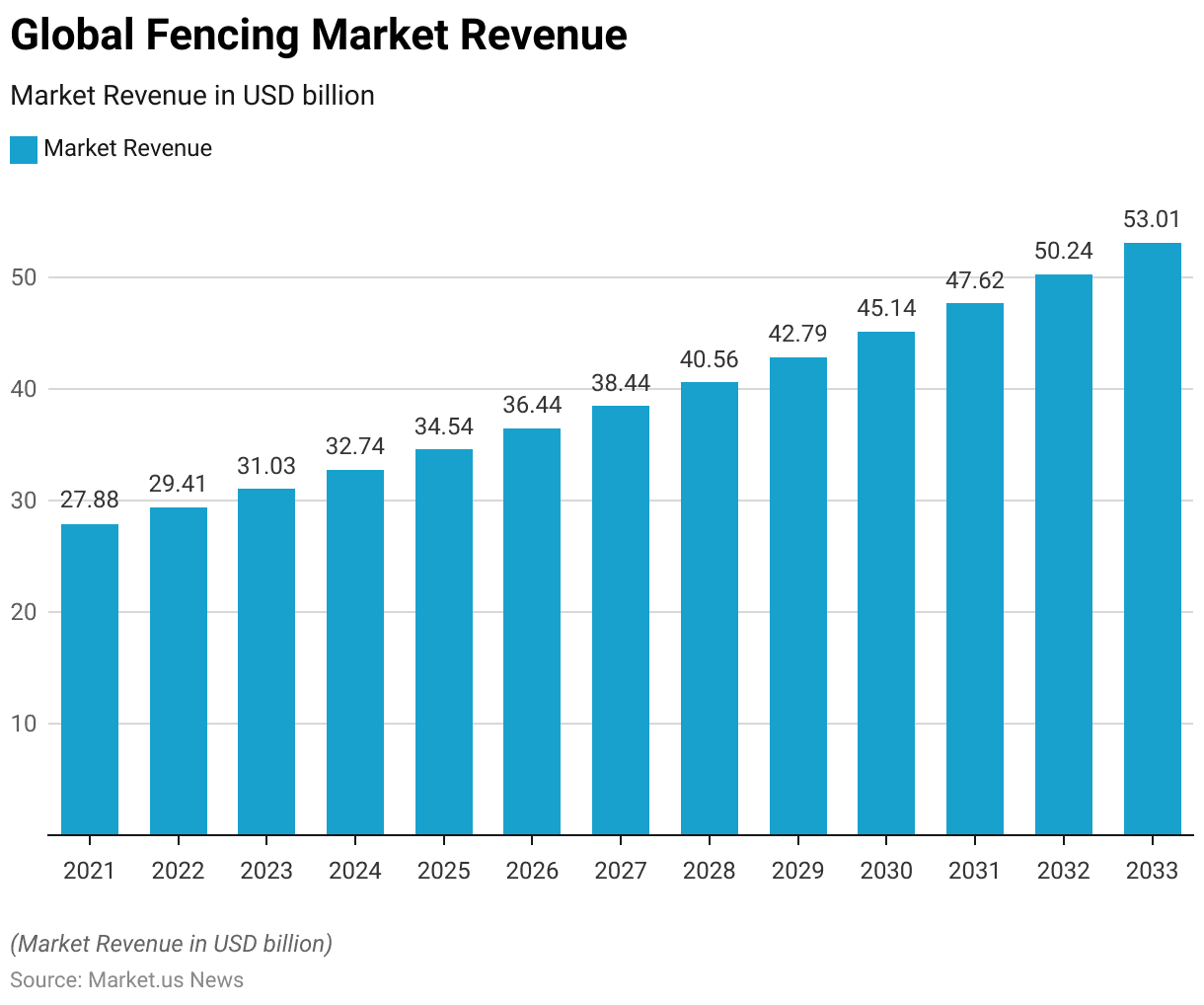

- The Global Fencing Market has experienced significant growth over the years at a CAGR of 5.5%, with revenue steadily increasing from USD 27.88 billion in 2021 to USD 29.41 billion in 2022.

- This upward trend continued through 2023, reaching USD 31.03 billion, and is projected to grow further, with revenue expected to hit USD 32.74 billion in 2024.

- The market is forecasted to expand substantially, achieving USD 34.54 billion in 2025, USD 36.44 billion in 2026, and USD 38.44 billion in 2027.

- By 2028, the market is anticipated to reach USD 40.56 billion, with further growth to USD 42.79 billion in 2029 and USD 45.14 billion in 2030.

- The projections indicate continued expansion, with revenue expected to rise to USD 47.62 billion in 2031, USD 50.24 billion in 2032, and culminating at USD 53.01 billion by 2033.

- This consistent growth highlights the increasing demand and investment in the fencing industry globally.

(Source: market.us)

Competitive Landscape of the Global Fencing Market Statistics

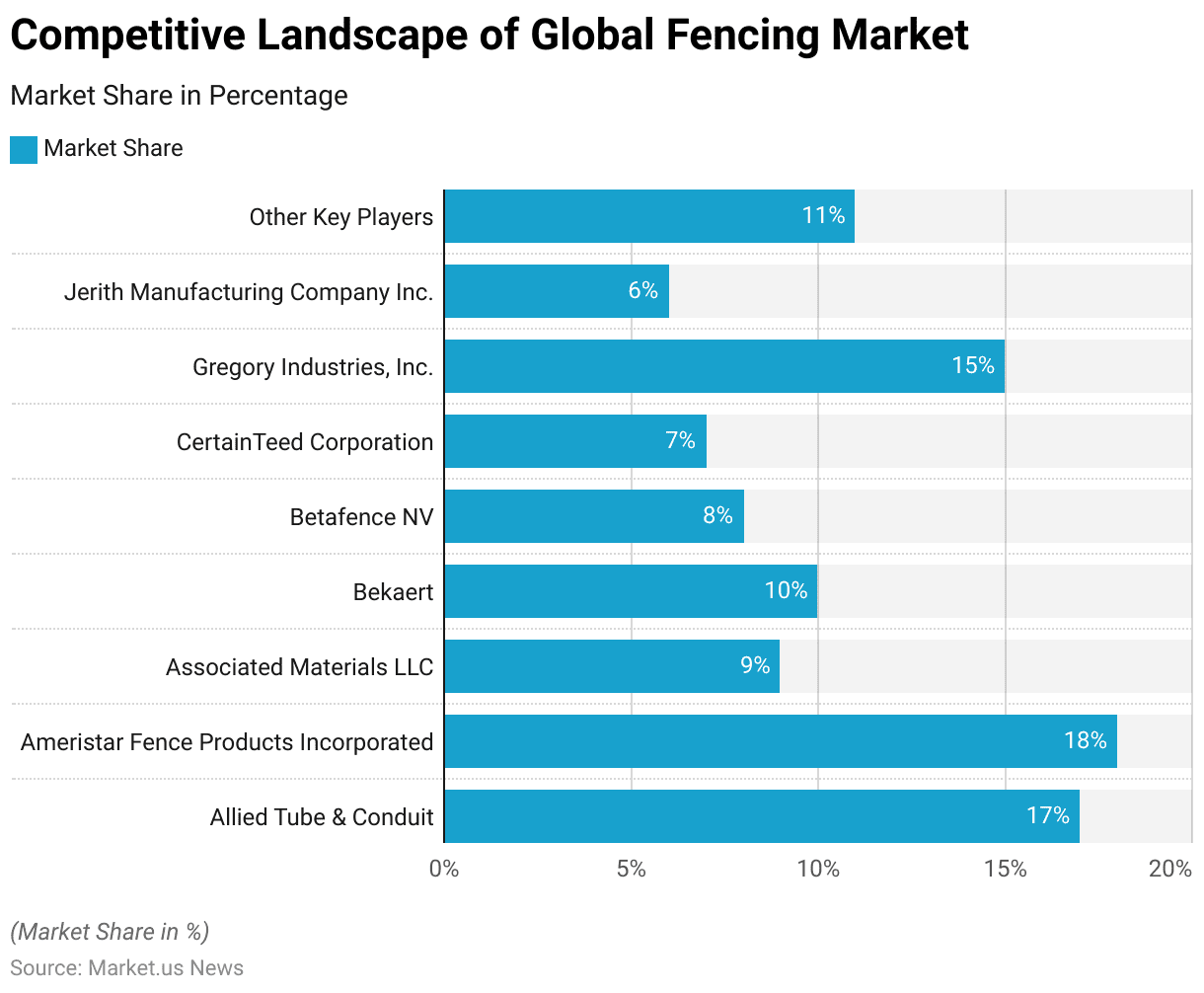

- The global fencing market is dominated by several key players, with Ameristar Fence Products Incorporated leading with an 18% market share.

- Allied Tube & Conduit follows closely with a 17% share.

- Gregory Industries, Inc. holds a significant portion of the market at 15%.

- Bekaert and Associated Materials LLC control 10% and 9% of the market, respectively.

- Betafence NV captures 8% of the market, while CertainTeed Corporation and Jerith Manufacturing Company Inc. hold 7% and 6% shares, respectively.

- Other key players collectively account for 11% of the market.

- This distribution of market share underscores the competitive landscape and the presence of both major and minor players in the fencing industry.

(Source: market.us)

Regional Analysis of the Global Fencing Market Statistics

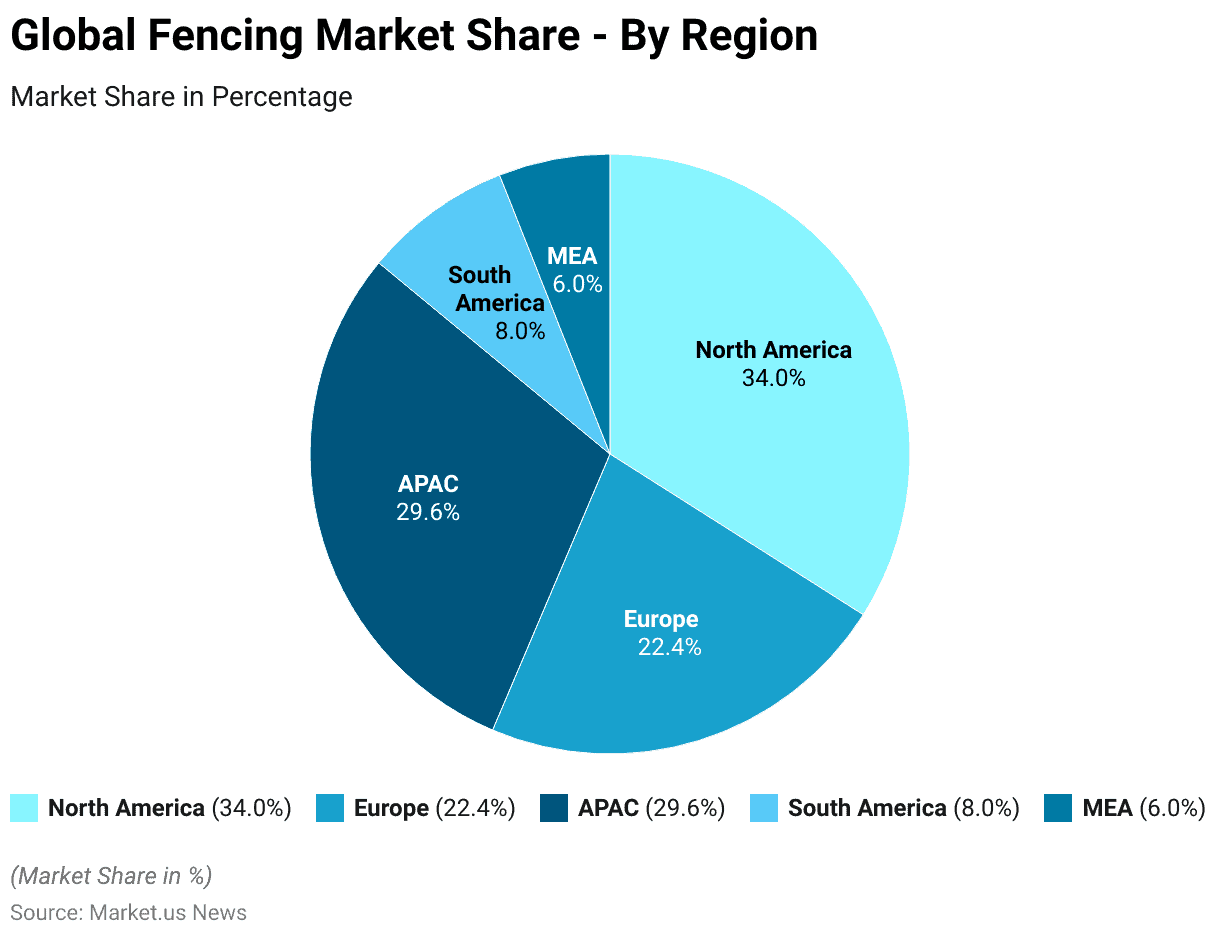

- A diverse regional distribution of market share characterizes the global fencing market.

- North America leads the market, holding a substantial 34.0% share, followed by the Asia-Pacific (APAC) region, which accounts for 29.6% of the market.

- Europe also plays a significant role, capturing 22.4% of the market share.

- South America, the Middle East, and Africa (MEA) contribute smaller portions, with market shares of 8.0% and 6.0%, respectively.

- This regional analysis highlights the prominent role of North America and APAC in the global fencing market while also indicating notable contributions from Europe, South America, and MEA.

(Source: market.us)

Factors Driving the Growth of the Fencing Industry Statistics

Rising Urbanization

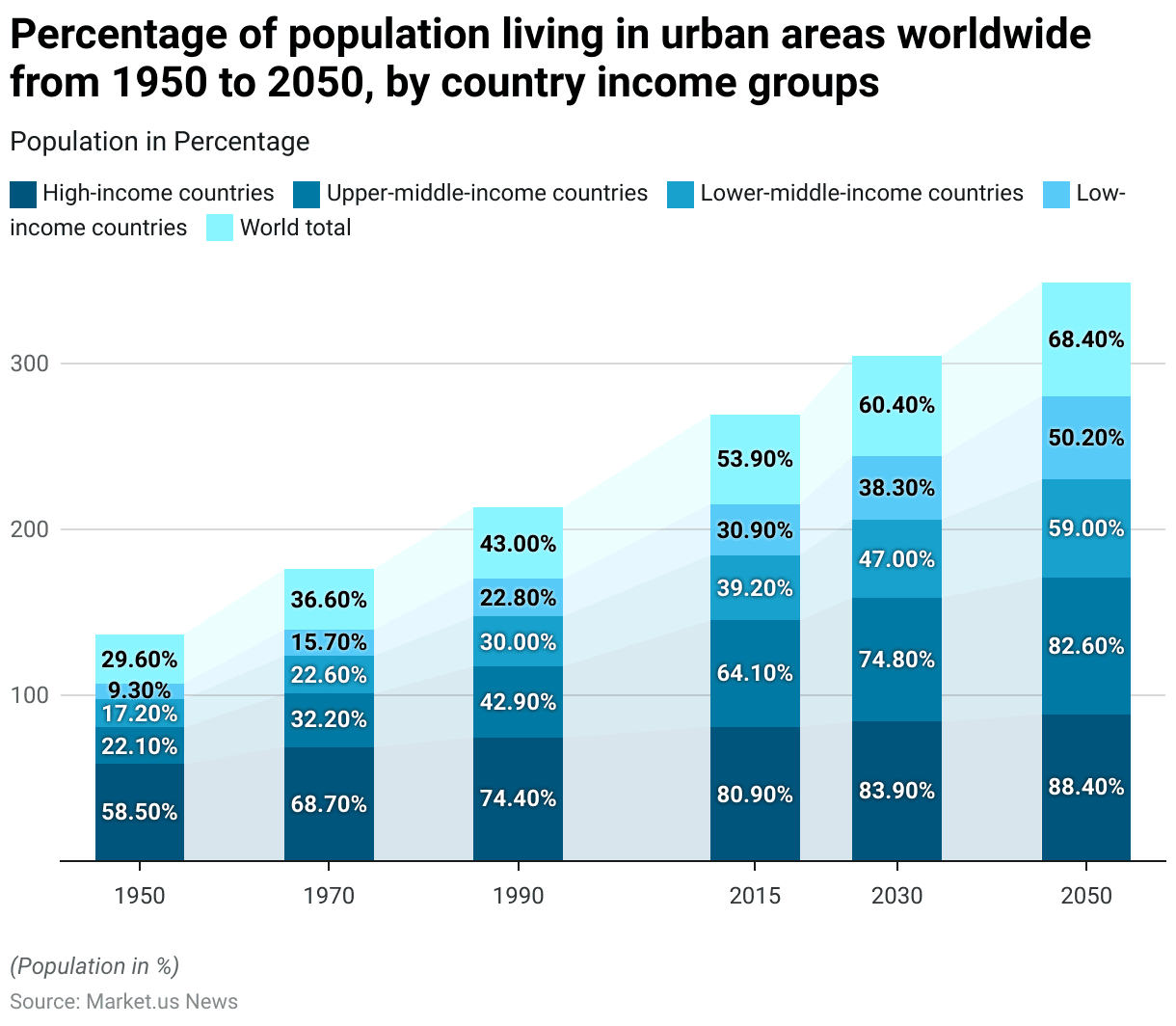

- The percentage of the population living in urban areas worldwide has shown a significant increase from 1950 to 2050, with varying trends across different country income groups.

- In high-income countries, urbanization rose from 58.50% in 1950 to 68.70% in 1970, reaching 74.40% by 1990 and further climbing to 80.90% in 2015. It is projected to grow to 83.90% in 2030 and 88.40% by 2050.

- Upper-middle-income countries saw urban populations grow from 22.10% in 1950 to 32.20% in 1970, 42.90% in 1990, and a significant increase to 64.10% in 2015, with future projections indicating 74.80% by 2030 and 82.60% by 2050.

- Lower-middle-income countries experienced growth from 17.20% in 1950 to 22.60% in 1970, 30% in 1990, and 39.20% in 2015, with expectations of 47% by 2030 and 59% by 2050.

More Insights

- Low-income countries had the lowest urbanization rates, starting at 9.30% in 1950 and increasing to 15.70% in 1970, 22.80% in 1990, and 30.90% in 2015, with projections of 38.30% by 2030 and 50.20% by 2050.

- The global total urban population grew from 29.60% in 1950 to 36.60% in 1970, 43% in 1990, and 53.90% in 2015, with future projections of 60.40% by 2030 and 68.40% by 2050, reflecting a steady and significant trend toward urbanization across all income groups.

- The surge in urbanization significantly boosts the fence market, driven by the migration of people from rural to urban areas, resulting in higher population densities.

- This trend spurs demand for residential and non-residential constructions, thereby propelling the fencing industry forward.

- The growth of the middle class further supports this sector. As a result, future growth in the fencing industry is expected to be driven by increasing urbanization.

(Source: Statista)

Rise in Construction Spending

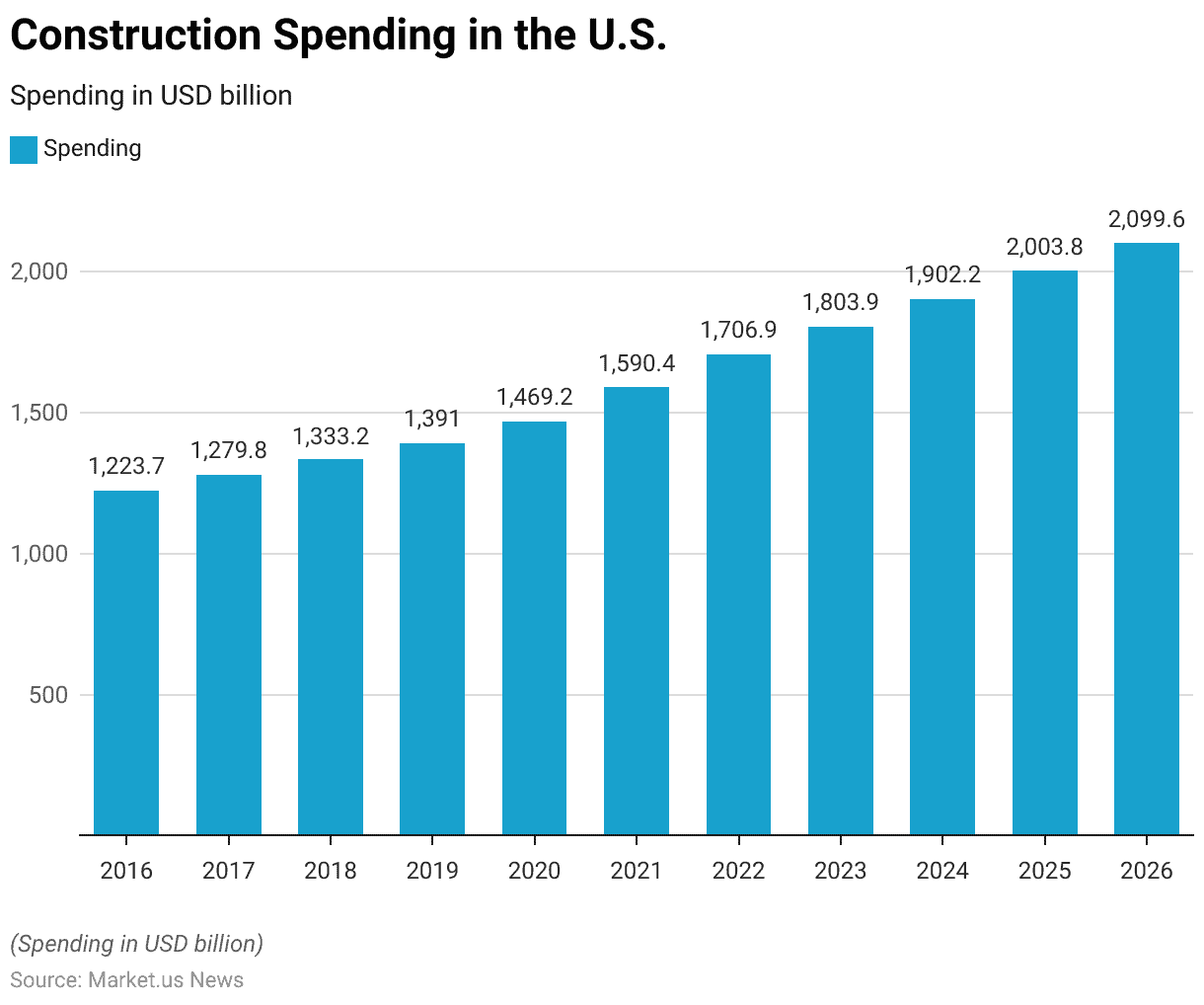

- Construction spending in the United States has shown a consistent upward trend from 2016 to 2026.

- In 2016, the total construction spending amounted to USD 1,223.7 billion.

- This figure increased to USD 1,279.8 billion in 2017 and further to USD 1,333.2 billion in 2018.

- By 2019, spending reached USD 1,391.0 billion, and a significant jump was seen to USD 1,469.2 billion in 2020.

- The growth continued in 2021, with spending rising to USD 1,590.4 billion, followed by an increase to USD 1,706.9 billion in 2022.

- In 2023, construction spending reached USD 1,803.9 billion, and it is projected to grow to USD 1,902.2 billion in 2024.

- By 2025, spending is expected to surpass USD 2 trillion, reaching USD 2,003.8 billion and further expanding to USD 2,099.6 billion in 2026.

- This steady increase underscores the robust growth and expansion in the U.S. construction industry over the past decade.

- The rise in construction spending is driving demand for reliable and durable fencing, spurring innovations in manufacturing.

(Source: Statista)

Types of Fencing Material Statistics

Steel Fencing Statistics

Global Crude Steel Production

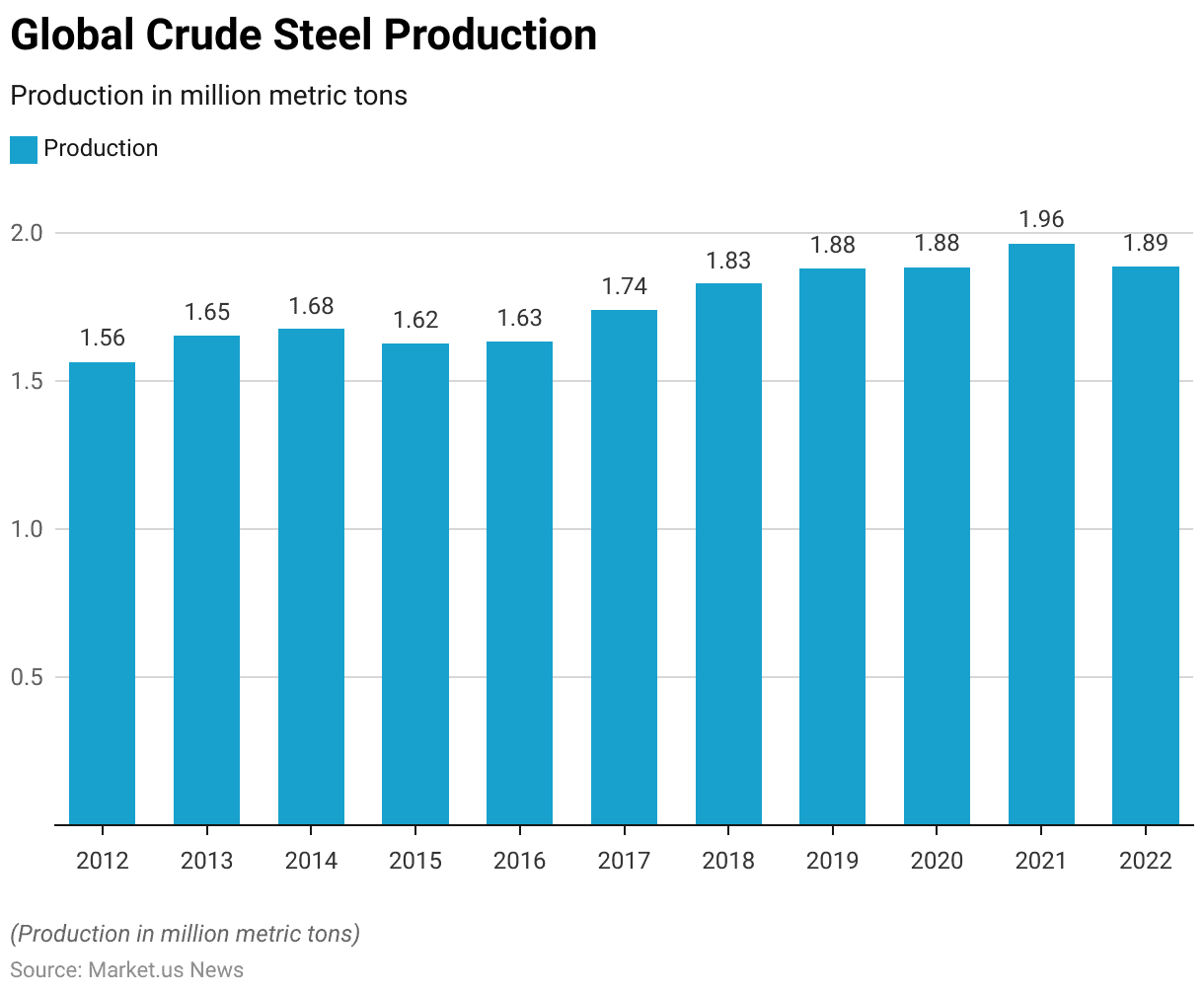

- Global crude steel production has shown notable fluctuations and overall growth from 2012 to 2022.

- In 2012, production was recorded at 1,563 million metric tons, increasing to 1,653 million metric tons in 2013 and 1,675 million metric tons in 2014.

- There was a slight decline in 2015, with production dropping to 1,624 million metric tons, but it rebounded to 1,633 million metric tons in 2016.

- The upward trend continued in subsequent years, reaching 1,737 million metric tons in 2017, 1,828 million metric tons in 2018, and 1,877 million metric tons in 2019.

- In 2020, production slightly increased to 1,882 million metric tons and further rose to 1,962 million metric tons in 2021.

- However, there was a slight decrease in 2022, with production totaling 1,885 million metric tons.

- This data reflects the dynamic nature of global crude steel production over the decade.

(Source: Statista)

Largest Crude Steel Producers

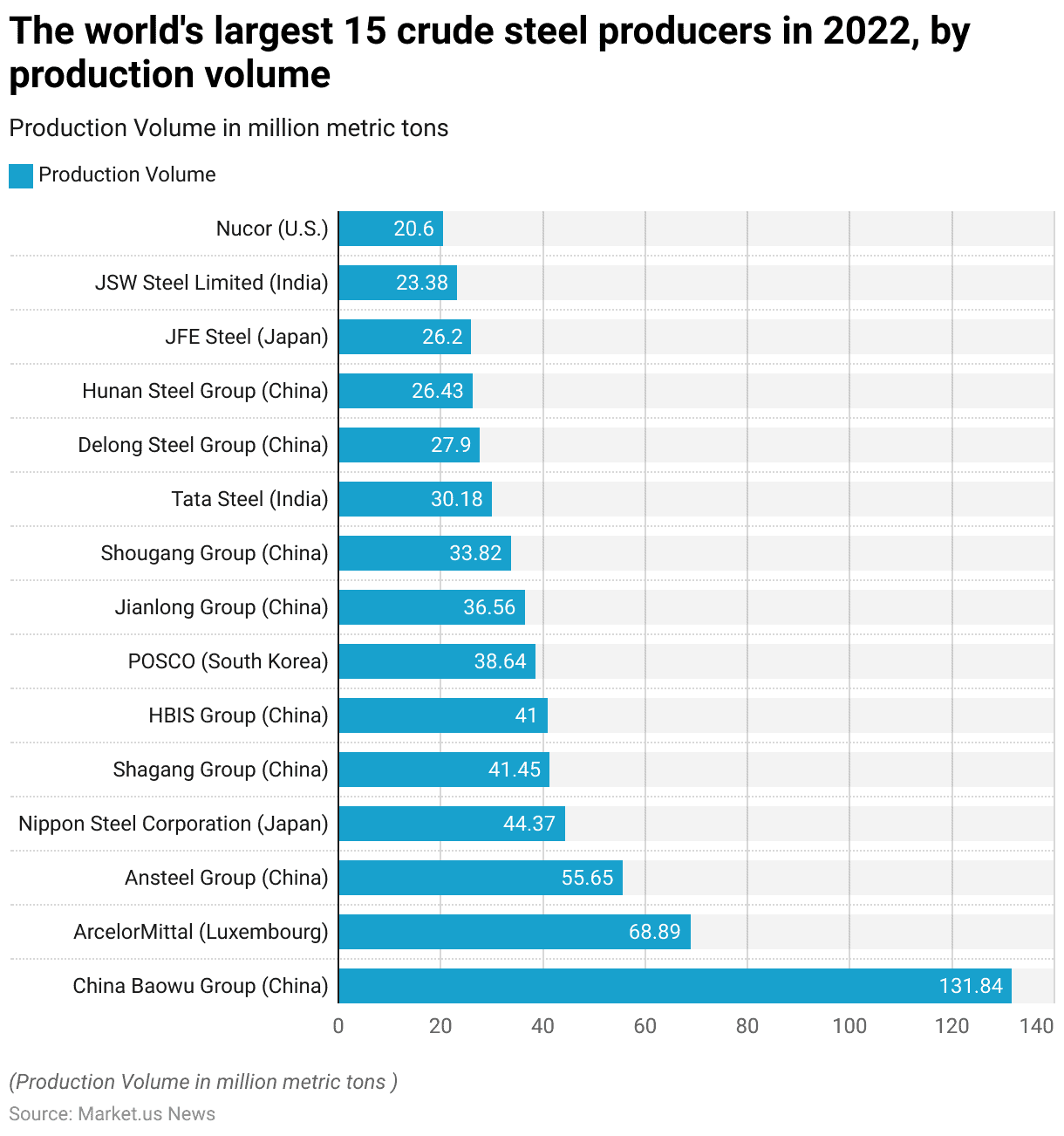

- In 2022, the world’s largest crude steel producers were led by China Baowu Group, with a production volume of 131.84 million metric tons.

- ArcelorMittal, based in Luxembourg, followed with 68.89 million metric tons.

- China’s Ansteel Group produced 55.65 million metric tons, while Japan’s Nippon Steel Corporation contributed 44.37 million metric tons.

- Other significant Chinese producers included Shagang Group with 41.45 million metric tons, HBIS Group with 41 million metric tons, and Jianlong Group with 36.56 million metric tons.

- South Korea’s POSCO produced 38.64 million metric tons.

- China’s Shougang Group and Delong Steel Group produced 33.82 million metric tons and 27.9 million metric tons, respectively.

- India’s Tata Steel and JSW Steel Limited contributed 30.18 million metric tons and 23.38 million metric tons, respectively.

- Hunan Steel Group of China produced 26.43 million metric tons, while Japan’s JFE Steel produced 26.2 million metric tons.

- The U.S. company Nucor produced 20.6 million metric tons, rounding out the list of the top 15 crude steel producers by volume in 2022.

(Source: Statista)

Bricks Fencing Statistics

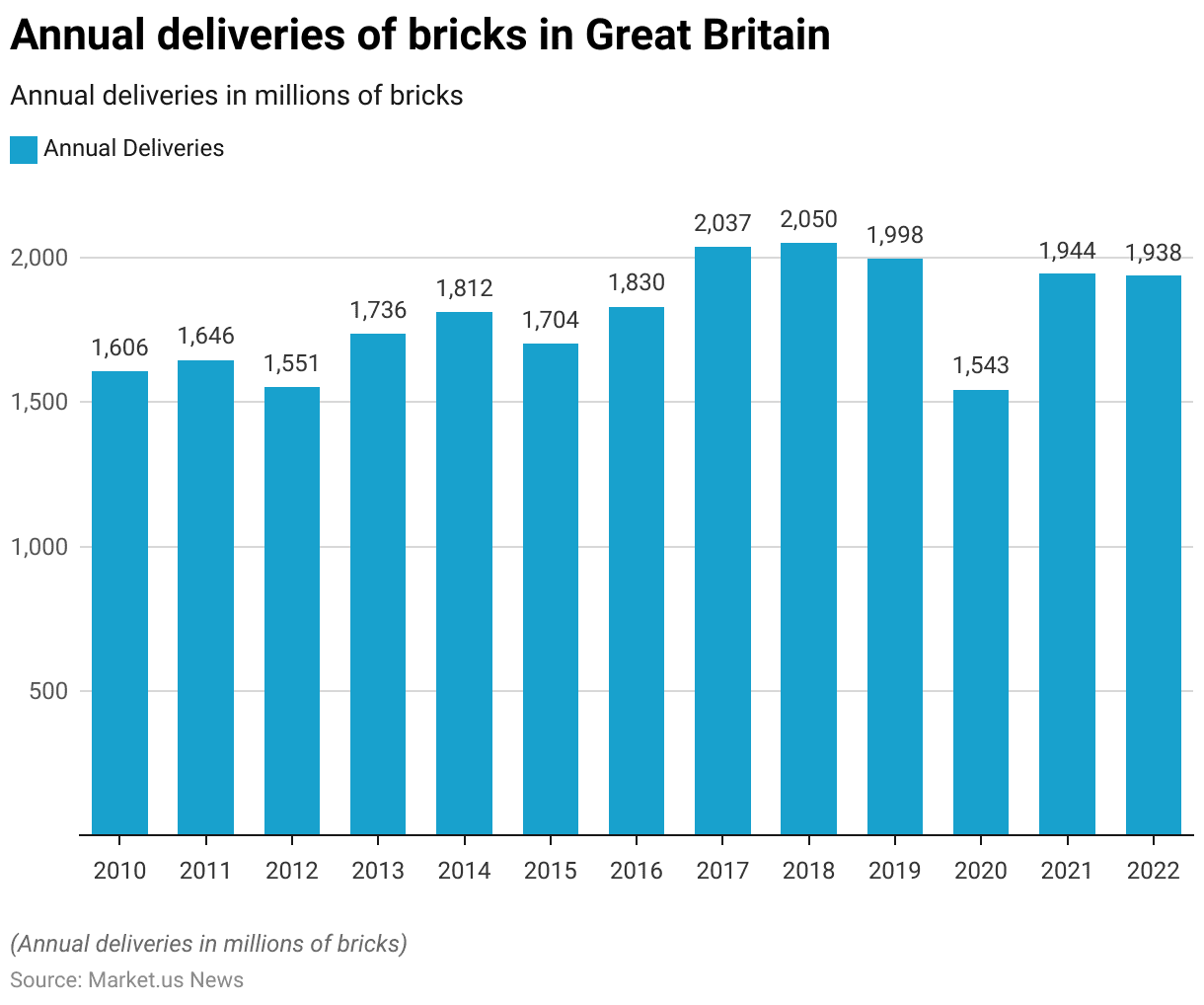

Annual Deliveries of Bricks

- The annual deliveries of bricks in Great Britain have shown considerable variation from 2010 to 2022.

- In 2010, deliveries stood at 1,606 million bricks, increasing slightly to 1,646 million bricks in 2011.

- The following year saw a decline to 1,551 million bricks, but deliveries rose again to 1,736 million bricks in 2013.

- This upward trend continued in 2014, reaching 1,812 million bricks.

- There was a slight dip in 2015, with 1,704 million bricks delivered, followed by an increase to 1,830 million bricks in 2016.

- Deliveries surged to 2,037 million bricks in 2017 and slightly more to 2,050 million bricks in 2018.

- In 2019, deliveries slightly decreased to 1,998 million bricks.

- The year 2020 saw a significant drop to 1,543 million bricks, likely due to the impact of the COVID-19 pandemic.

- However, deliveries rebounded to 1,944 million bricks in 2021 and remained relatively stable at 1,938 million bricks in 2022.

- This data reflects the fluctuations in the brick market over the past decade, influenced by various economic factors.

(Source: Statista)

Cement Fencing Statistics

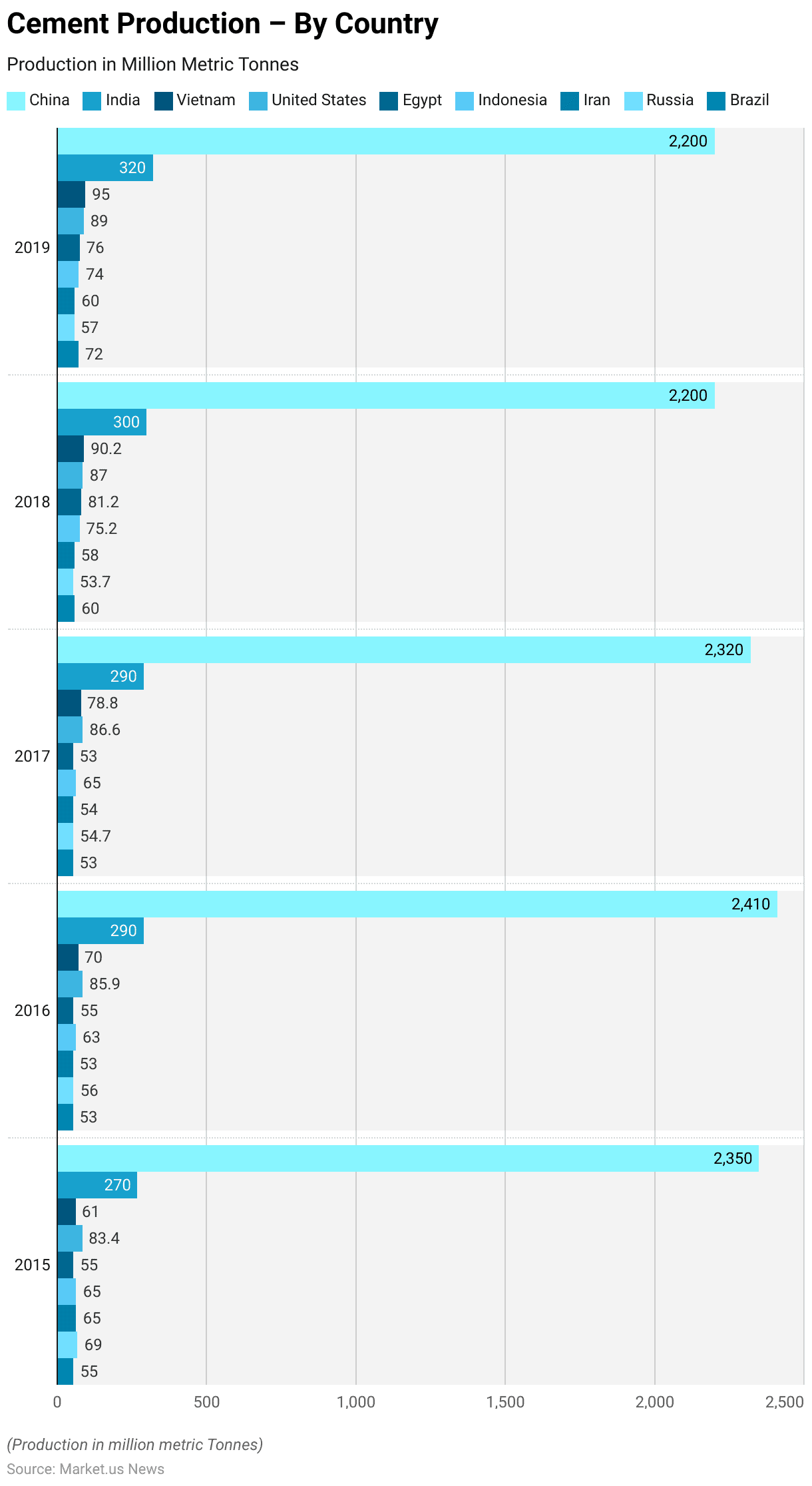

Cement Production – By Country

- From 2015 to 2019, cement production varied significantly among major producing countries.

- China consistently led global production, with volumes fluctuating between 2,350 million metric tonnes in 2015 and 2,410 million metric tonnes in 2016 before stabilizing at 2,200 million metric tonnes by 2018 and 2019.

- India saw a steady increase from 270 million metric tonnes in 2015 to 320 million metric tonnes in 2019.

- Vietnam’s production rose notably from 61 million metric tonnes in 2015 to 95 million metric tonnes in 2019.

- The United States maintained a steady increase, from 83.4 million metric tonnes in 2015 to 89 million metric tonnes in 2019.

- Egypt experienced significant growth, with production increasing from 55 million metric tonnes in 2015 to 81.2 million metric tonnes in 2018 before dropping to 76 million metric tonnes in 2019.

- Indonesia’s production varied slightly, peaking at 75.2 million metric tonnes in 2018.

- Iran’s production remained relatively stable, from 65 million metric tonnes in 2015 to 60 million metric tonnes in 2019.

- Russia’s production decreased from 69 million metric tonnes in 2015 to 53.7 million metric tonnes in 2018, then rose to 57 million metric tonnes in 2019.

- Brazil showed an increase from 55 million metric tonnes in 2015 to 72 million metric tonnes in 2019.

- This data highlights the dynamic changes in cement production across these key countries.

(Source: Datis Export Group)

Aluminum Fencing Statistics

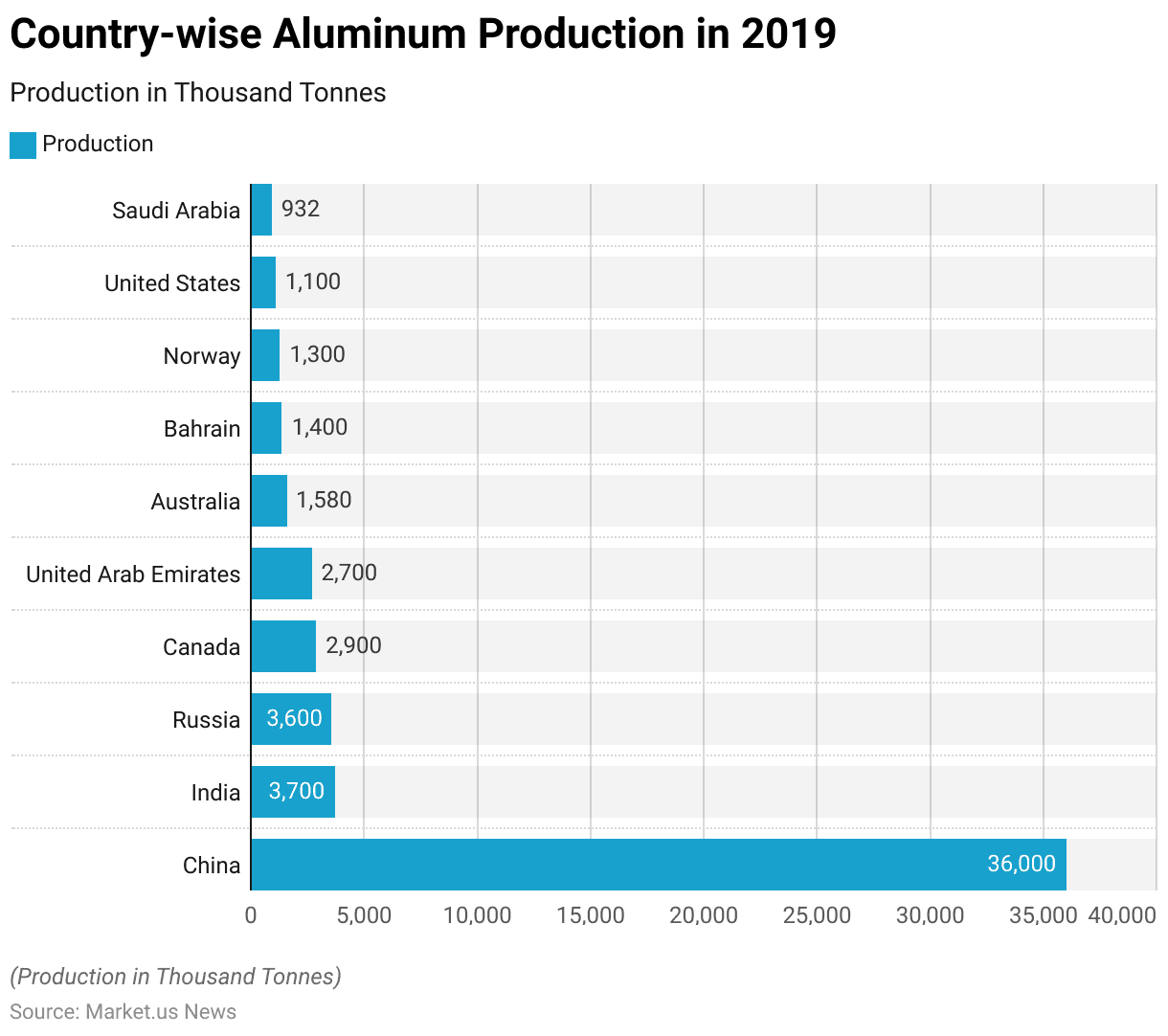

Aluminum Production – By Country

- In 2019, global aluminum production was led by China, which produced a staggering 36,000 thousand tonnes.

- India followed as the second-largest producer with 3,700 thousand tonnes, closely trailed by Russia with 3,600 thousand tonnes.

- Canada also played a significant role, producing 2,900 thousand tonnes.

- The United Arab Emirates contributed 2,700 thousand tonnes to global production.

- Other notable producers included Australia with 1,580 thousand tonnes, Bahrain with 1,400 thousand tonnes, and Norway with 1,300 thousand tonnes.

- The United States produced 1,100 thousand tonnes, while Saudi Arabia accounted for 932 thousand tonnes.

- This data underscores China’s dominance in the aluminum industry and highlights the contributions of other key players globally.

(Source: British Geological Survey)

Iron Fencing Statistics

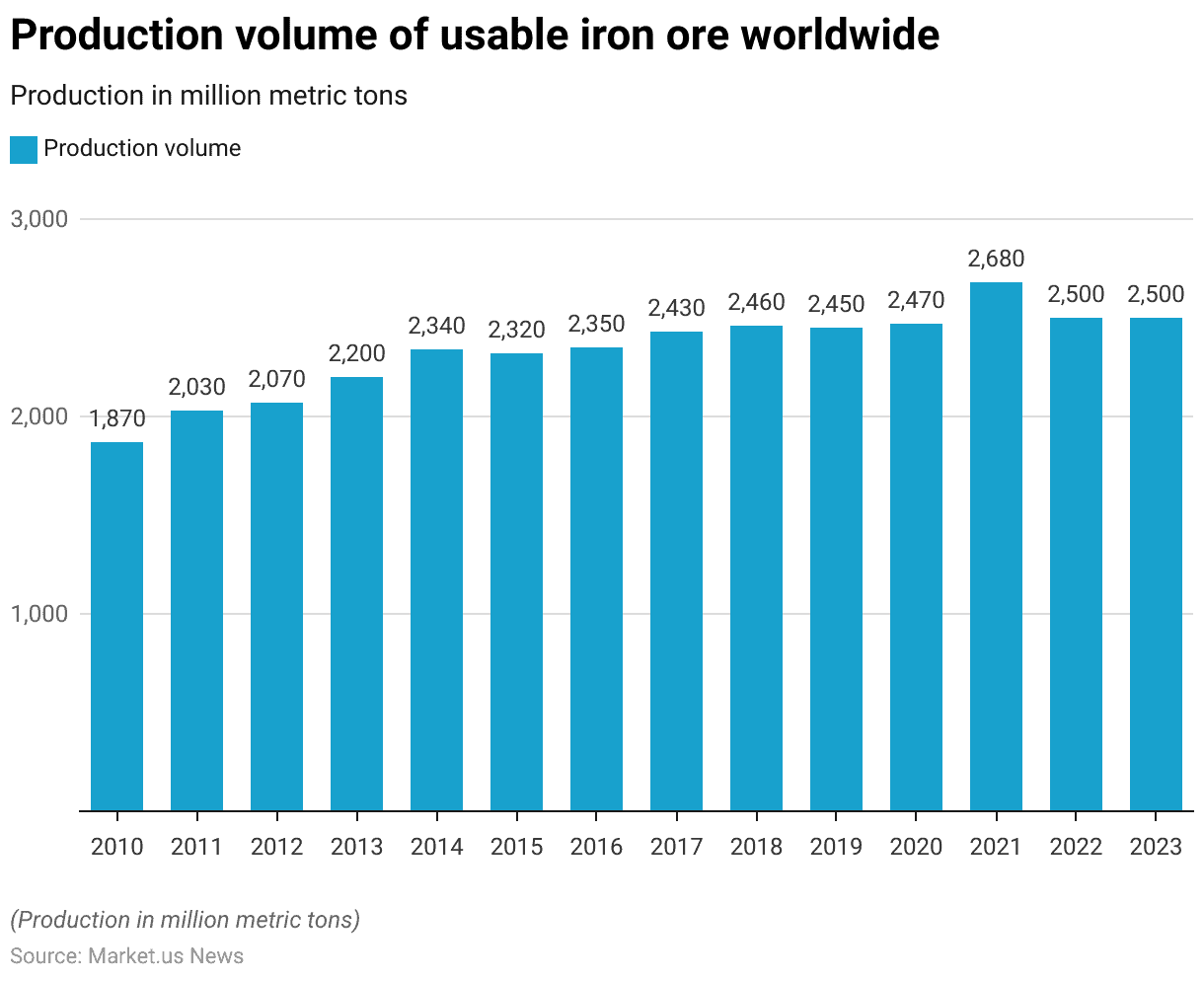

Production Volume of Usable Iron Ore Worldwide

- The production volume of usable iron ore worldwide has shown a steady increase from 2010 to 2023.

- In 2010, global production was 1,870 million metric tons, which rose to 2,030 million metric tons in 2011 and slightly increased to 2,070 million metric tons in 2012.

- The growth continued with 2,200 million metric tons in 2013 and 2,340 million metric tons in 2014.

- Despite a slight decrease to 2,320 million metric tons in 2015, production rebounded to 2,350 million metric tons in 2016.

- This upward trend persisted, with production volumes reaching 2,430 million metric tons in 2017 and 2,460 million metric tons in 2018.

- In 2019, production slightly decreased to 2,450 million metric tons but rose again to 2,470 million metric tons in 2020.

- The year 2021 saw a significant increase, with production peaking at 2,680 million metric tons.

- However, production volumes stabilized at 2,500 million metric tons in both 2022 and 2023.

- This data highlights the overall growth in iron ore production over the past decade, with notable fluctuations in recent years.

(Source: Statista)

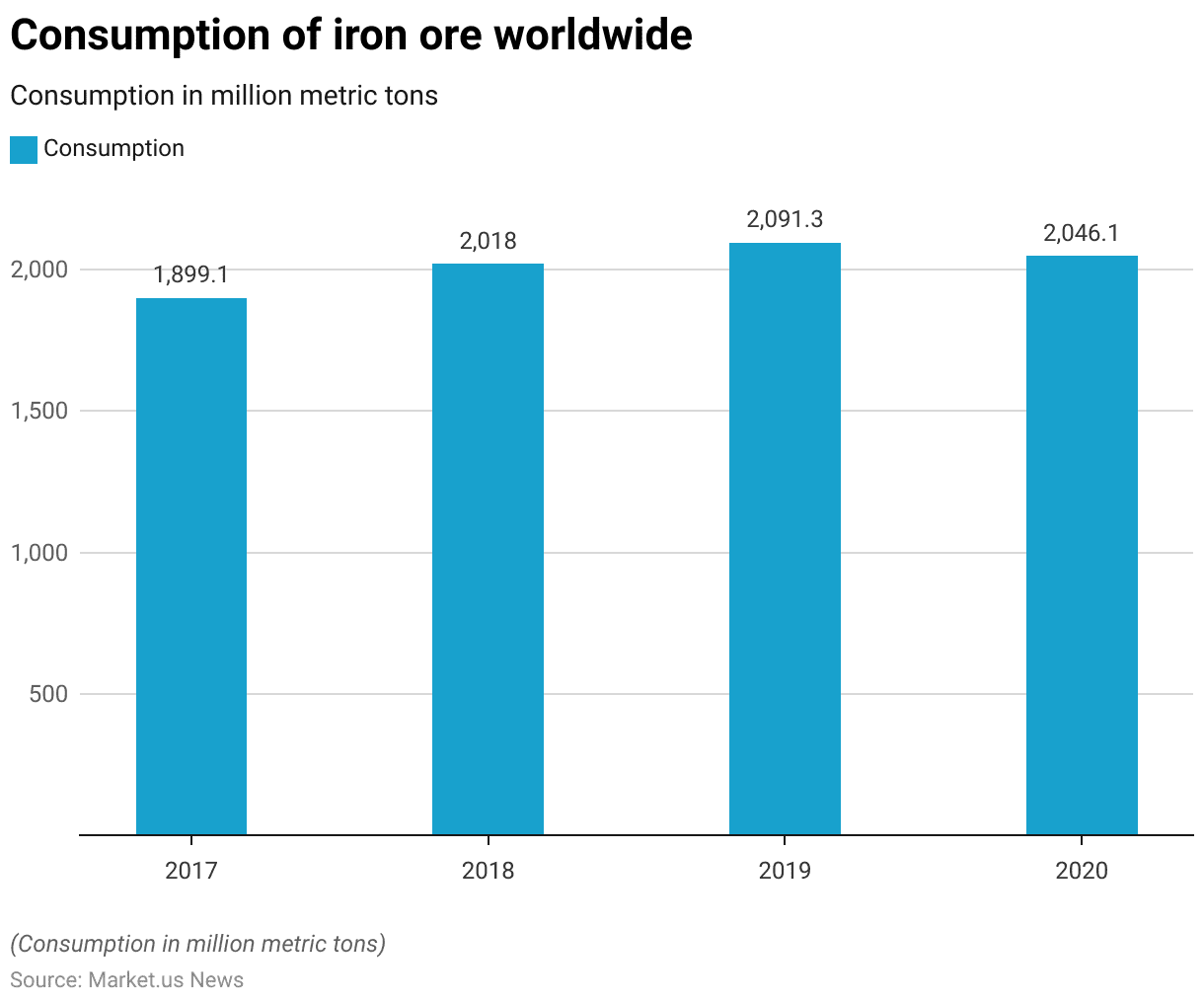

Consumption of Iron Ore Worldwide

- From 2017 to 2020, the global consumption of iron ore has shown an upward trend with slight fluctuations.

- In 2017, the consumption was 1,899.1 million metric tons, which increased to 2,018.0 million metric tons in 2018.

- The upward trend continued in 2019, reaching 2,091.3 million metric tons.

- However, in 2020, there was a slight decrease in consumption, which fell to 2,046.1 million metric tons.

- This data reflects the overall growth in iron ore consumption worldwide despite minor variations in the trend.

(Source: Statista)

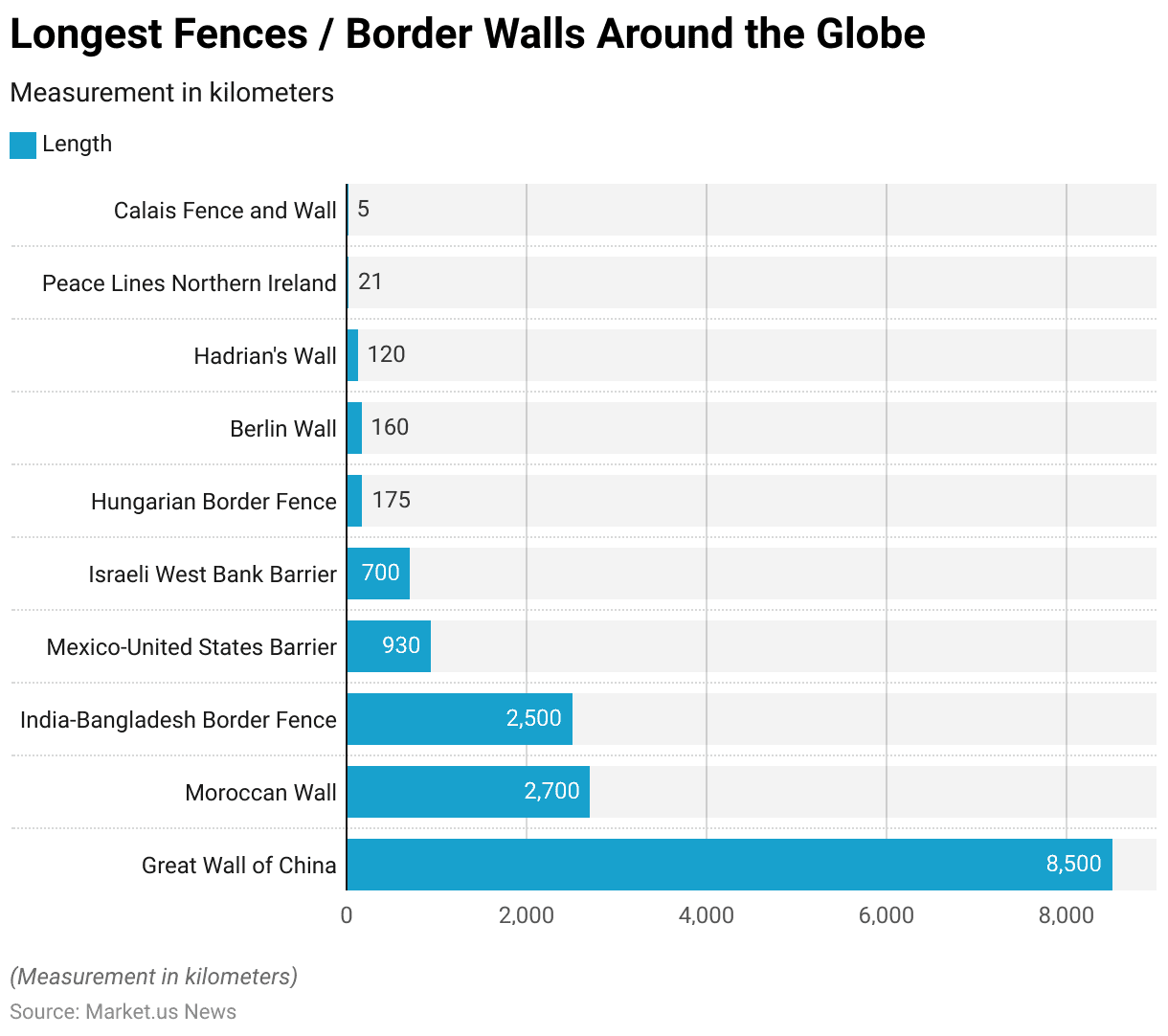

Longest Fencing/Border Walls Around the Globe Statistics

- The longest fences and border walls around the globe vary significantly in length, with the Great Wall of China being the most extensive at 8,500 kilometers.

- Following this is the Moroccan Wall, which stretches for 2,700 kilometers.

- The India-Bangladesh Border Fence is also notable, covering 2,500 kilometers.

- The Mexico-United States Barrier extends for 930 kilometers, while the Israeli-West Bank Barrier is 700 kilometers long.

- The Hungarian Border Fence measures 175 kilometers, and the Berlin Wall, although no longer standing, historically extended 160 kilometers.

- Hadrian’s Wall, built by the Romans, spans 120 kilometers.

- In Northern Ireland, the Peace Lines measure 21 kilometers.

- The Calais Fence and Wall, used to prevent illegal immigration, is the shortest among these, at just 5 kilometers.

- These structures reflect the diverse geopolitical, historical, and security considerations that have driven their construction.

(Source: Statista)

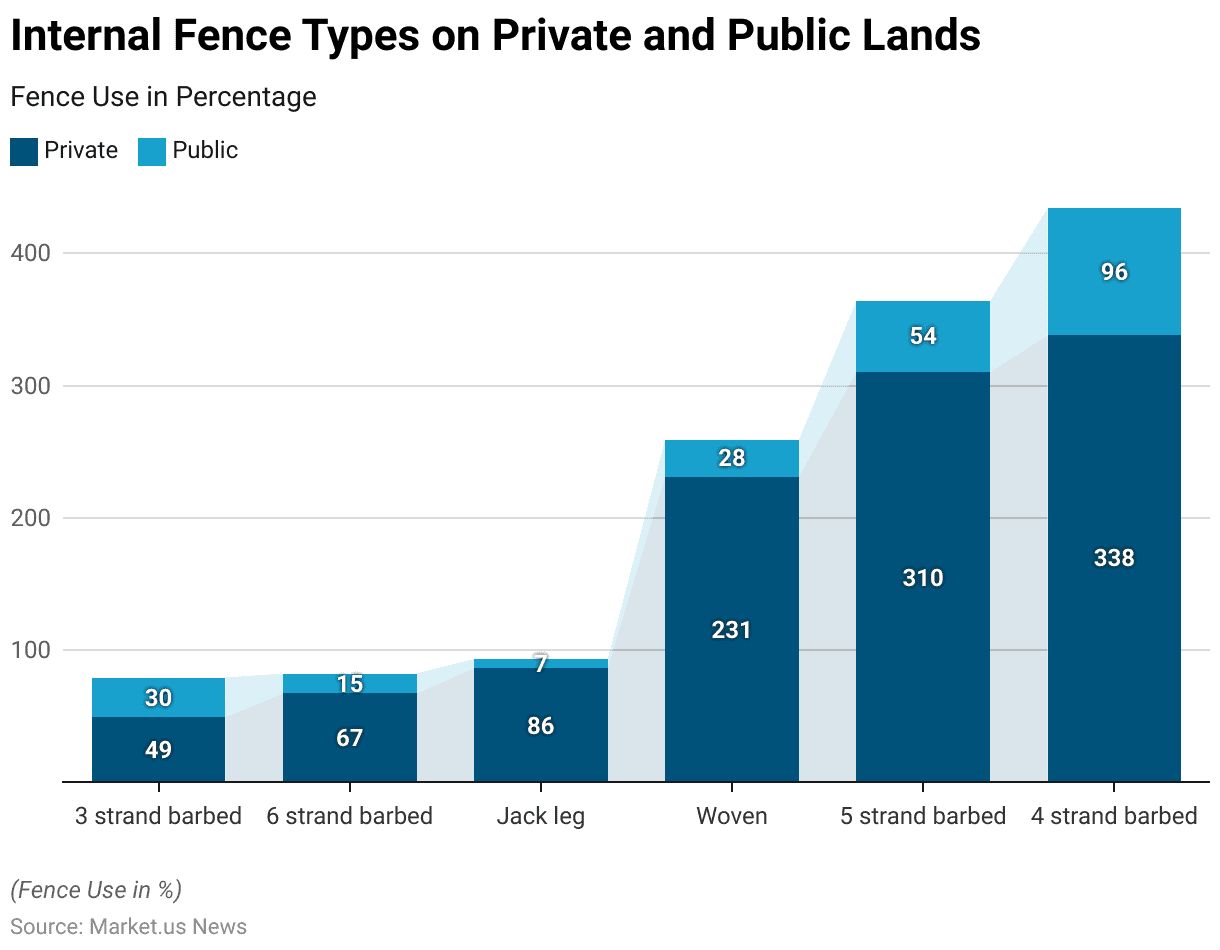

Internal Fencing Types on Private and Public Lands Statistics

- The distribution of internal fence types on private and public lands reveals distinct preferences and usage patterns.

- On private lands, four-strand barbed wire fences are the most common, accounting for 338% of the total fences sampled.

- Five-strand barbed wire fences follow this at 310%, and woven fences at 231%.

- Jack-leg fences are less prevalent on private lands, representing 86% of the total, while six-strand barbed wire and three-strand barbed wire fences account for 67% and 49%, respectively.

- In contrast, on public lands, four-strand barbed wire fences also lead in usage but at a significantly lower rate of 96%.

- The five-strand barbed wire fences make up 54% of the total, while woven fences are used even less frequently at 28%.

- Jack-leg fences are rare, constituting only 7%, and the six-strand barbed and three-strand barbed fences account for 15% and 30% of the total, respectively.

- This data illustrates a higher diversity and frequency of barbed wire fences on private lands compared to public lands.

(Source: Frontier)

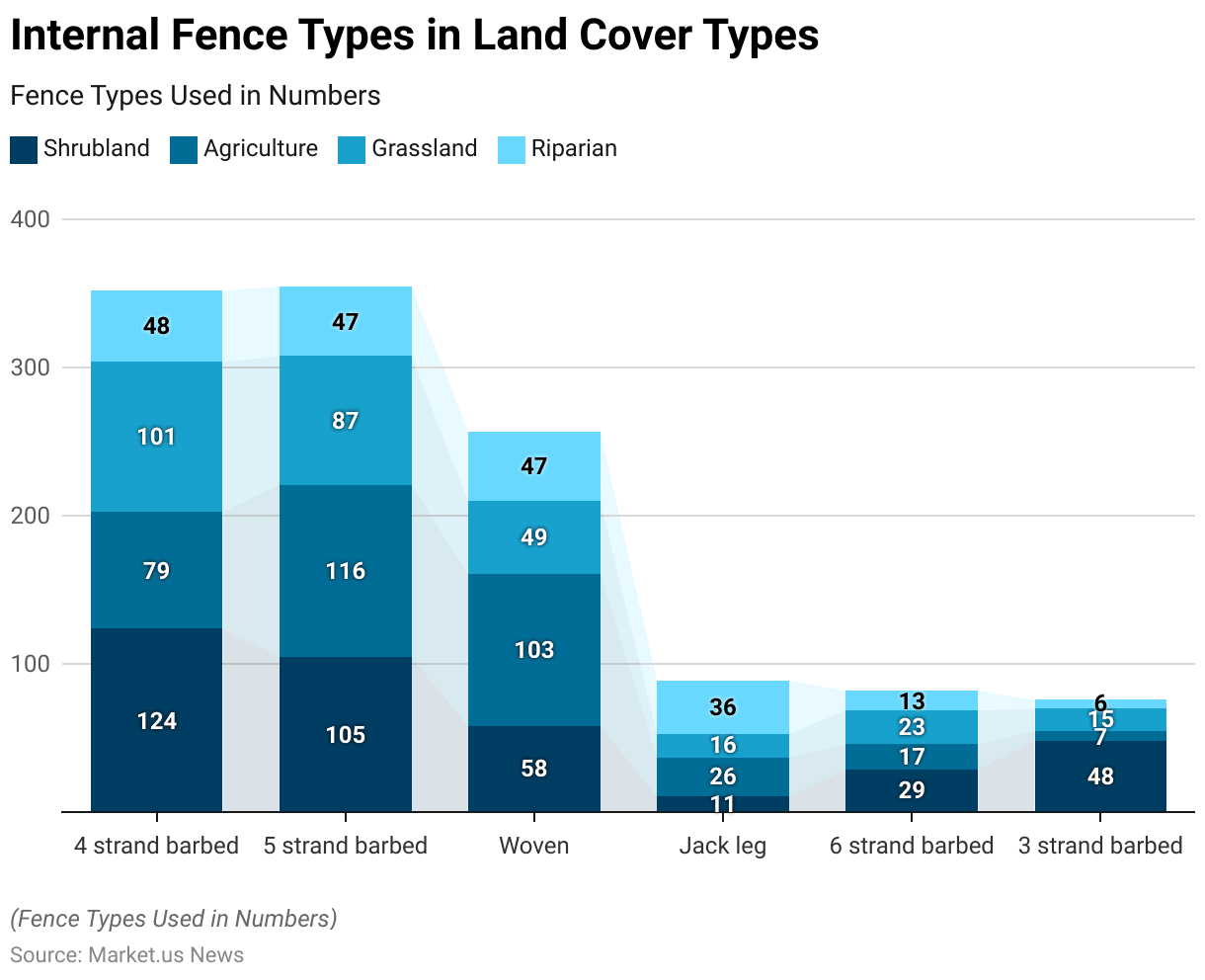

Internal Fencing Types in Land Cover Types Statistics

- The distribution of internal fence types across different land cover types shows varying preferences. In shrubland areas, four-strand barbed wire fences are the most prevalent, accounting for 124% of the total fences sampled.

- Five-strand barbed wire fences follow this at 105%, and three-strand barbed wire fences at 48%. Woven fences constitute 58% of the total in shrubland, while jack-leg and six-strand barbed wire fences represent 11% and 29%, respectively.

- In agricultural areas, five-strand barbed wire fences dominate with 116%, followed by woven fences at 103%.

- The four-strand barbed wire fences account for 79%, while jack leg fences make up 26%.

- The six-strand barbed and three-strand barbed wire fences are less common in agricultural lands, accounting for 17% and 7%, respectively.

- Grassland areas show a higher prevalence of 4-strand barbed wire fences at 101%, followed by five-strand barbed wire fences at 87%.

- Woven fences and three-strand barbed wire fences account for 49% and 15%, respectively. Jack-leg fences are used less frequently, representing 16%, and six-strand barbed wire fences account for 23%.

- In riparian areas, four-strand and five-strand barbed wire fences are equally common, each accounting for 47%. Woven fences also make up 47% of the total, while jack-leg fences represent 36%.

- The six-strand and three-strand barbed wire fences are the least common, accounting for 13% and 6%, respectively.

- This data illustrates the varying usage patterns of fence types based on the specific characteristics and needs of different land cover types.

(Source: Frontier)

Regulations and Policies for Border Walls/ Fencing Statistics

- Regulations and policies for border walls and fences vary significantly across countries and have evolved in response to political, security, and migration challenges.

- In the United States, the Secure Fence Act of 2006 authorized the construction of hundreds of miles of fencing along the U.S.-Mexico border, with subsequent budgets and policies under various administrations further expanding and maintaining these barriers.

- The Department of Homeland Security, through Customs and Border Protection (CBP), manages these projects with significant financial investments, such as the $1.375 billion allocated in fiscal year 2018 for border infrastructure.

- In Europe, the EU has been cautious about directly financing physical barriers, although substantial funds are allocated for border management and surveillance technologies.

- For instance, from 2021 to 2027, the EU has earmarked €6.7 billion for border management, focusing more on integrated approaches and less on physical walls, despite pressures from certain member states.

- Countries like Hungary and Lithuania have independently financed and constructed extensive fences to manage migration flows, often with significant national investments.

- These examples reflect the complex and varied approaches nations take toward regulating and implementing border security measures.

(Sources: U.S. Customs and Border Patrol, Migration Policy Institute, El Pais)

Recent Developments

Acquisitions:

- Fencing Supply Group’s Acquisition of Atlantic Fence Supply: In September 2023, Fencing Supply Group acquired Atlantic Fence Supply, a U.S.-based fencing supplier. This acquisition aims to expand Fencing Supply Group’s capabilities and increase its customer base.

- TriWest Capital Partners Acquires Phoenix Fence Corp.: In February 2023, TriWest Capital Partners acquired a controlling interest in Phoenix Fence Corp., a market-leading provider of fencing and related goods. This acquisition will help Phoenix Fence expand its market presence and product offerings.

New Product Launches:

- Jacksons Fencing’s New T-shaped Steel Posts: In May 2021, Jacksons Fencing launched T-shaped steel posts designed for timber fence panels. These posts offer enhanced durability and stability for fencing installations.

- Introduction of Reverse Vending Machines: Companies are integrating advanced technology into vending machines, such as reverse vending machines that incentivize recycling efforts by providing rewards. These machines can process multiple containers simultaneously, enhancing efficiency.

Funding:

- Crossplane Capital’s Investment in Viking Fence: In February 2023, Crossplane Capital joined forces with Sal Chavarria to purchase a controlling stake in Viking Fence. This investment aims to enhance Viking Fence’s capabilities and expand its market reach.

Market Growth:

- Global Market Expansion: The growth is driven by increasing construction activities, rising demand for security, and advancements in fencing technologies.

- Regional Insights: North America held the largest market share in 2021, driven by the high demand for home renovation and remodeling. The Asia-Pacific region is expected to witness significant growth due to increasing safety concerns and government initiatives to improve public infrastructure.

Innovation and Trends:

- Smart Fencing Systems: Advancements in fencing technologies, such as smart fencing systems with integrated surveillance and alarm systems, are attracting customers looking for enhanced security solutions.

- Sustainable Fencing Materials: There is a growing trend towards eco-friendly fencing materials, such as recycled composites and energy-efficient manufacturing processes, to meet the increasing demand for sustainable products.

Conclusion

Fencing Statistics – The increasing global demand for fencing, driven by rising construction activities and security concerns, has prompted significant advancements in fencing technologies and materials.

Regulations and policies for border walls and fences differ across regions, reflecting diverse geopolitical contexts.

In the U.S., extensive funding and legislative support have facilitated the construction and maintenance of border barriers, emphasizing security and immigration control.

Conversely, the European Union focuses on integrated border management, investing heavily in surveillance and infrastructure without directly financing physical walls, reflecting a more holistic approach to border security.

This divergence highlights the complex interplay between national security priorities, economic considerations, and humanitarian concerns in the development and implementation of fencing and border wall policies globally.

FAQs

Common types of fences include chain-link, wood, vinyl, aluminum, and wrought iron. Each type serves different purposes, such as security, privacy, aesthetics, and durability.

Installing a fence provides several benefits, including enhanced privacy, increased security, and improved property aesthetics. Fences can also define property boundaries, contain pets, and provide a safe play area for children. Additionally, a well-installed fence can increase property value and curb appeal.

Costs vary widely based on materials, height, length, and complexity of the installation. On average, expect to pay between $1,500 and $4,000 for residential fencing projects.

Regulations vary by location. It’s essential to check with local municipalities or homeowner associations for any required permits, height restrictions, and boundary regulations.

Environmental impacts vary by material. Wood fences, if sourced sustainably, can have a lower environmental footprint but may require treatments that involve chemicals. Vinyl fences are durable and low-maintenance but are made from PVC, a plastic that can be challenging to recycle. Metal fences, such as aluminum, are often recyclable and can be made from recycled materials, making them a more environmentally friendly option.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)