Table of Contents

Introduction

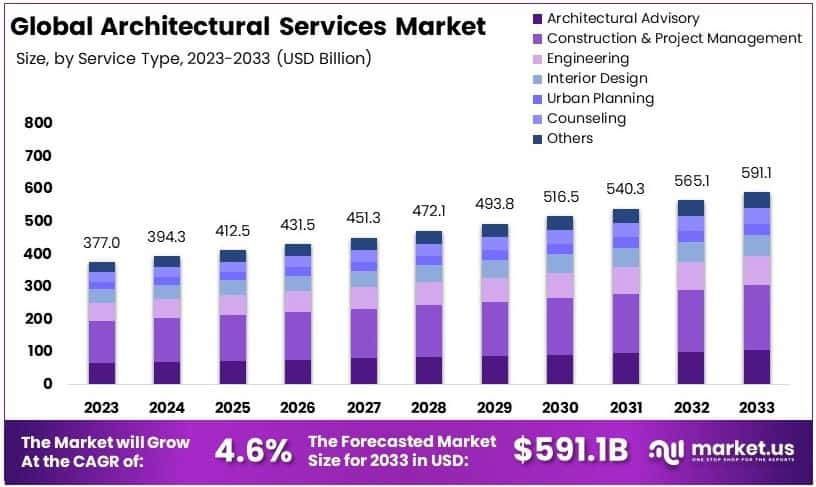

The Global Architectural Services Market is projected to reach a valuation of approximately USD 591.1 billion by 2033, up from an estimated USD 377.0 billion in 2023. This growth reflects a compound annual growth rate (CAGR) of 4.6% over the forecast period from 2024 to 2033.

Architectural services encompass a wide range of professional offerings provided by architects and architectural firms, including design, planning, and management of construction projects. These services involve conceptualizing and developing building designs, preparing detailed blueprints, conducting feasibility studies, ensuring compliance with zoning and regulatory requirements, and overseeing project execution. The objective is to create aesthetically appealing, functional, and sustainable structures that meet client needs while adhering to environmental and economic considerations.

The architectural services market refers to the industry comprising firms and professionals engaged in delivering architecture-related solutions across various sectors, including residential, commercial, industrial, and infrastructure. This market includes activities such as urban planning, interior design, landscape architecture, and consulting services for construction projects. It plays a pivotal role in shaping cities, communities, and infrastructure, responding to evolving trends in urbanization, sustainability, and technology integration.

The growth of the architectural services market is driven by several key factors. Urbanization and population growth are primary contributors, particularly in emerging economies where the demand for housing and infrastructure is surging.

Additionally, the growing emphasis on green and sustainable construction practices has prompted a rising need for architects skilled in energy-efficient and environmentally friendly design solutions. The integration of advanced technologies, such as Building Information Modeling (BIM) and 3D printing, has also enhanced the efficiency and precision of architectural processes, further fueling market expansion.

Demand within the architectural services market is closely linked to construction and infrastructure activities, which are heavily influenced by economic development and government policies. The commercial real estate sector, driven by investments in office spaces, retail establishments, and mixed-use developments, remains a significant demand generator.

Meanwhile, the residential sector has seen a steady rise in demand, particularly for affordable housing in urban areas. The shift toward smart cities and digital infrastructure has further contributed to the growing need for architectural expertise.

The architectural services market is poised for substantial opportunities, especially in areas such as sustainable design and urban redevelopment. Governments worldwide are prioritizing net-zero carbon initiatives and smart city projects, creating a robust demand for architectural services focused on energy-efficient and intelligent design solutions.

Additionally, emerging markets in Asia-Pacific, the Middle East, and Africa present vast opportunities as these regions continue to urbanize and modernize their infrastructure. Technological advancements, such as virtual reality (VR) and artificial intelligence (AI), also open new avenues for innovation, enabling architects to deliver immersive and highly customized solutions to clients.

Key Takeaways

- The Architectural Services Market was valued at USD 377.0 billion in 2023 and is expected to reach USD 591.1 billion by 2033, with a CAGR of 4.6%.

- Construction and Project Management Services led the service type segment in 2023, contributing 33.6% of the market, highlighting their key role in managing complex building projects.

- The industrial sector dominated the end-use segment with a 41.6% share in 2023, reflecting strong demand for specialized architectural services.

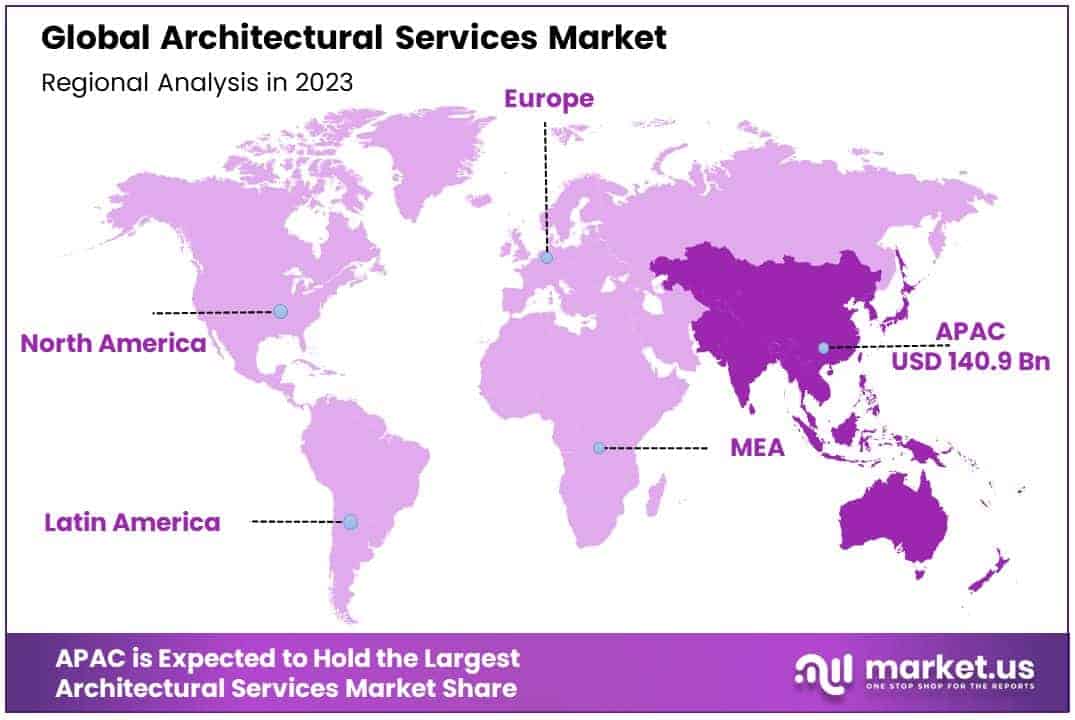

- Asia Pacific held the largest regional share at 37.4% in 2023, valued at USD 140.9 billion, driven by rapid urbanization and infrastructure expansion.

Architectural Services Statistics

- The U.S. has 73,313 architecture businesses.

- Employment for architects is projected to grow 4.8% from 2022 to 2032.

- Around 6,000 architect jobs are expected to open during this period.

- Small firms dominate the industry, with 91% having fewer than 19 employees.

- About 75% of architecture firms operate with five or fewer employees.

- Women make up 46% of emerging professionals and 53% of students at firms.

- Licensed female architects represent 27% of the profession.

- Firms with 50+ employees generate nearly half of total revenue in private practice.

- Larger firms, with 100+ employees, contribute 30% of industry employment and billings.

- Private companies employ 56% more architects than public companies.

- 45% of architecture firms use IoT technology for smart building systems.

- There are 121,368 employees in the U.S. architecture industry.

- Firms with 50+ employees represent over half of private practice employment.

- 90% of firms place operational responsibilities on principals and executive teams.

- Approximately 8,200 new architect positions are expected annually over the decade.

- In the UK, there are 375,000 listed buildings, one for every 170 residents.

- Hiring activity in the industry has surged from 52% to 84% in the last year.

- The Great Resignation has had a limited impact, with turnover stable at 45% of firms.

- Female students now make up 57% of new Part 1 entrants, a 5% rise over five years.

- Only 6.5% of AIA firms had 50 or more employees, and 2.5% had 100 or more.

- 35,621 candidates were actively working toward licensure recently.

Emerging Trends

- Sustainability and Green Architecture: There is an increasing demand for eco-friendly architectural designs, driven by stricter government regulations and a growing emphasis on sustainability. The use of materials such as recycled steel, bamboo, and solar panels is becoming standard. For instance, over 40% of global construction now integrates green building principles.

- Adoption of Building Information Modeling (BIM): The adoption of BIM technology is transforming the architectural industry by enabling better visualization, design precision, and project efficiency. More than 70% of architectural firms in developed markets now utilize BIM tools, allowing for seamless collaboration and real-time updates during project development.

- Prefabrication and Modular Construction: Architectural designs are increasingly incorporating prefabricated and modular construction approaches. These methods reduce project timelines by up to 30% and construction costs by 20%, making them highly attractive for urban housing projects and commercial developments.

- Smart Building Integration: Architectural services are evolving to include the integration of smart building technologies such as IoT-enabled lighting, HVAC systems, and energy monitoring tools. In 2023, it was reported that 25% of new commercial buildings in urban areas were designed with smart technology capabilities in mind.

- Focus on Urban Redevelopment and Mixed-Use Spaces: Urban population growth has led to a shift toward redeveloping older spaces into modern, mixed-use areas that combine residential, retail, and office spaces. Nearly 60% of urban development projects today involve mixed-use planning to optimize land usage and address housing shortages.

Top Use Cases

- Urban Residential Development: Architectural services are widely used in designing high-density residential complexes in metropolitan areas. In cities with over 1 million residents, housing projects now account for more than 40% of architectural projects due to the increasing demand for affordable and compact living spaces.

- Commercial and Retail Spaces: Architects are playing a key role in designing innovative commercial spaces, such as shopping malls and office hubs. For instance, in 2022 alone, global retail construction projects valued over $800 billion relied on architectural expertise to meet modern consumer and tenant preferences.

- Infrastructure Projects: From airports to bridges and stadiums, architectural services are crucial in shaping large-scale infrastructure projects. For example, it is estimated that over 20% of global architectural firms focus primarily on infrastructure design to support urbanization and connectivity.

- Restoration of Heritage Buildings: The restoration of cultural and historical buildings is a growing use case for architectural services. Governments and private institutions are spending significant budgets to restore structures, with over $25 billion allocated globally in 2023 for heritage preservation.

- Educational and Healthcare Facilities: Educational institutions and healthcare facilities are increasingly relying on architects to design functional and patient/student-centric buildings. Over 15% of global architectural service revenues are estimated to come from these two sectors, driven by rising investments in public infrastructure.

Major Challenges

- Cost Management and Budget Overruns: Architects face challenges in managing costs and preventing budget overruns during projects. On average, 25% of construction projects exceed their budget by 10–20%, often due to unanticipated design changes or material cost fluctuations.

- Labor Shortages and Skills Gaps: A shortage of skilled labor in architecture and construction has emerged as a significant challenge. In 2023, nearly 35% of firms reported difficulty in finding experienced professionals, impacting project timelines and design quality.

- Complex Regulatory Compliance: Adhering to complex zoning laws, environmental regulations, and building codes is time-consuming and costly. In urban areas, over 40% of projects face delays due to issues related to regulatory approvals.

- Technological Adaptation: Many smaller architectural firms struggle to adopt and integrate advanced technologies such as BIM, AR/VR, and AI tools. Approximately 30% of such firms cite financial constraints or lack of expertise as barriers to digital transformation.

- Client Expectations and Design Revisions: Frequent design revisions due to shifting client demands often lead to delays and inefficiencies. Studies show that over 20% of architectural projects experience an extended timeline due to misaligned expectations or last-minute changes.

Top Opportunities

- Expansion in Emerging Markets: Emerging markets in Asia, Africa, and Latin America present immense growth opportunities for architectural services. Urbanization in these regions is projected to drive demand for residential, commercial, and infrastructure projects, potentially contributing to over 50% of the global market’s growth by 2030.

- Rising Demand for Affordable Housing: The global shortage of affordable housing has created an opportunity for architects to design cost-effective yet sustainable housing solutions. Governments in developing countries are investing billions annually in affordable housing schemes, signaling high potential for architectural contributions.

- Integration of Renewable Energy Solutions: Architectural services can capitalize on the push for renewable energy by designing buildings with integrated solar panels, wind turbines, and energy storage systems. By 2025, it is expected that at least 30% of new architectural designs will include renewable energy elements.

- Healthcare Infrastructure Expansion: The growing demand for hospitals and clinics, especially in aging and underserved populations, represents a key growth avenue. By 2024, global healthcare infrastructure spending is projected to exceed $500 billion, offering architects a chance to design innovative and patient-friendly facilities.

- Adoption of Smart City Concepts: Architectural services are critical for developing smart cities, which incorporate advanced technologies for efficient urban living. With over 150 cities worldwide implementing smart city projects by 2030, architects have opportunities to design technology-enabled urban landscapes.

Key Player Analysis

- AECOM: AECOM is a global leader in architecture, engineering, and construction services, generating over $13 billion in revenue as of 2023. The firm is known for its multidisciplinary approach, combining design excellence with infrastructure development. AECOM’s portfolio includes projects like stadiums, urban developments, and transportation hubs. Its ability to execute large-scale, complex projects positions it as a dominant force in the industry.

- Gensler: Gensler, one of the world’s largest architecture firms, operates across 49 locations globally and reported revenue exceeding $1.5 billion in 2023. The company specializes in workplace design, retail spaces, and urban planning. With high-profile projects like the Shanghai Tower and tech campus developments, Gensler continues to innovate through human-centric and technology-forward designs.

- Nikken Sekkei Ltd.: Based in Japan, Nikken Sekkei is renowned for its sustainable architecture and urban design expertise, contributing to projects such as the Tokyo Skytree. The firm employs over 2,800 professionals and focuses heavily on reducing environmental impacts through innovative materials and design strategies. Nikken Sekkei generates approximately $600 million in annual revenue, primarily from its projects in Asia.

- Foster + Partners: Foster + Partners is a UK-based architectural powerhouse with a strong emphasis on sustainable design and futuristic aesthetics. Generating annual revenue near $300 million, the firm’s landmark projects include Apple’s headquarters in Cupertino and the London City Hall. Known for integrating advanced technologies like AI and parametric design, Foster + Partners remains at the forefront of the global architectural landscape.

- HOK: HOK, a globally recognized design, architecture, and engineering firm, is celebrated for its focus on healthcare facilities, sports venues, and urban planning. The firm’s annual revenue is estimated at $400 million, with flagship projects such as the Mercedes-Benz Stadium in Atlanta and the Dubai Marina Mall. HOK consistently drives innovation through sustainable practices and client-focused solutions.

Asia Pacific Architectural Services Market

Asia Pacific The Lead Region in the Architectural Services Market with Largest Market Share at 37.4%

Asia Pacific dominated the architectural services market in 2023, accounting for a substantial 37.4% of the global market share, with a market valuation of USD 140.9 billion. This remarkable growth is driven by rapid urbanization, booming construction activities, and significant government investments in infrastructure development across emerging economies such as China, India, and Southeast Asia. China’s robust construction sector, fueled by its urban planning initiatives, contributes heavily to the region’s market dominance, while India’s rising demand for affordable housing and commercial infrastructure supports sustained growth.

Additionally, Southeast Asia has emerged as a key growth frontier due to ongoing investments in smart city projects and industrial parks. The increasing adoption of sustainable and eco-friendly architectural designs, coupled with the presence of a large pool of skilled professionals, further amplifies the region’s competitive edge. These factors collectively position Asia Pacific as the pivotal hub for architectural services on a global scale.

Recent Developments

- In 2024, AECOM collaborated with stakeholders to create transformative outdoor spaces designed to improve community wellbeing. The company’s Architecture team, among the largest globally, remains committed to innovation, inclusivity, and ecological design principles aimed at building a better world.

- In 2024, Little Rock’s airport commission approved extensions for architectural service contracts. Bill and Hillary Clinton National Airport continues its partnership with Alliiance, a Minneapolis-based firm, to support terminal developments.

- October 2024 Architecture firms faced their twentieth consecutive month of declining billings, as reflected in the AIA/Deltek Architecture Billings Index score of 45.7. This trend underscores ongoing challenges despite improvements in the wider economy.

- In 2024, HOK reported surpassing the AIA 2030 Commitment energy reduction targets, showcasing significant advancements toward a carbon-neutral portfolio well ahead of schedule. This achievement reflects HOK’s leadership in sustainable design innovation.

Conclusion

The architectural services market is poised for steady growth, driven by increasing urbanization, infrastructure expansion, and the growing emphasis on sustainable and smart building solutions. Architects and firms are playing a critical role in addressing the rising demand for innovative, functional, and eco-friendly designs across residential, commercial, and industrial sectors.

While challenges such as regulatory complexities, cost management, and technological adoption persist, the market is adapting through advanced tools like BIM, modular construction methods, and renewable energy integration. Emerging economies present significant opportunities for expansion, particularly as governments invest in urban redevelopment and affordable housing projects. As the industry evolves, a focus on collaboration, sustainability, and technological innovation will be key to meeting client expectations and shaping the future of urban and architectural landscapes globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)