Market Overview

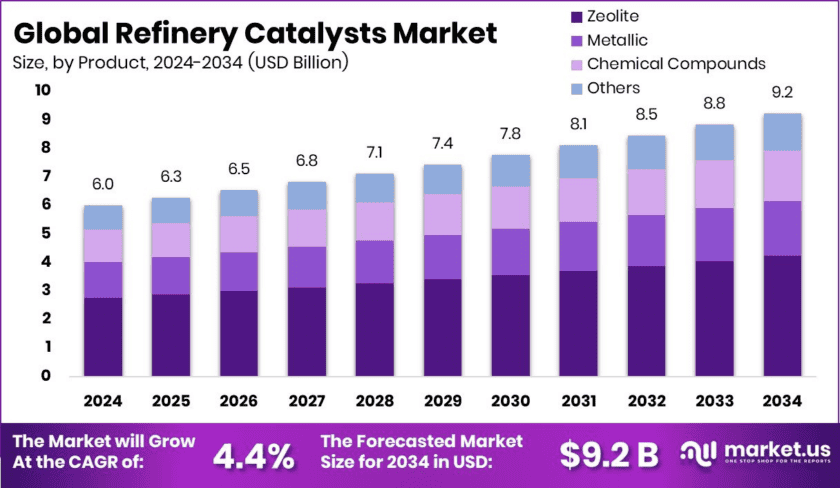

The Global Refinery Catalysts Market is expected to reach USD 9.2 billion by 2034, up from USD 6.0 billion in 2024. Market growth will occur at a CAGR of 4.4% from 2025 to 2034. Asia Pacific leads global consumption with a 44.8% market share, valued at USD 2.6 billion.

Refinery catalysts accelerate chemical reactions that convert crude oil into valuable products like gasoline, diesel, and jet fuel. These substances enhance key processes such as fluid catalytic cracking, hydrocracking, and catalytic reforming. Consequently, they improve efficiency, selectivity, and reduce both energy use and emissions.

Rising demand for cleaner fuels drives global market expansion. Stricter environmental regulations also push refineries toward advanced catalyst adoption. Additionally, technological advancements continue to improve catalyst performance, making refining operations more cost-effective and environmentally friendly.

Refineries in the Asia Pacific increasingly adopt catalysts to process heavier crude oils and renewable feedstocks. This strategy improves product yield and fuel quality significantly. Moreover, regulatory compliance remains a primary driver, as governments enforce emission standards that require advanced sulfur-reduction catalysts.

Key Takeaways

- The Global Refinery Catalysts Market is expected to reach USD 9.2 billion by 2034, up from USD 6.0 billion in 2024, at a CAGR of 4.4% from 2025 to 2034.

- Zeolite accounts for 45.8% of total product demand in the Refinery Catalysts Market globally.

- FCC catalysts dominate applications in the Refinery Catalysts Market, representing 38.2% of overall usage worldwide.

- The Asia Pacific, worth USD 2.6 billion, continues growing due to rising refinery demand and industrial expansion.

➤ Download Exclusive Sample Of This Premium Report – https://market.us/report/global-refinery-catalysts-market/request-sample/

Market Segmentation Overview

By Product Analysis

Zeolite held a dominant market position in the By Product segment with a 45.8% share in 2024. This strong performance results from Zeolite’s high efficiency in fluid catalytic cracking processes. The material enhances conversion rates and improves product yields substantially.

Zeolite’s ability to selectively target reactions while reducing energy consumption makes it a preferred choice for refineries worldwide. Moreover, increasing demand for cleaner fuels and stricter environmental regulations drives refiners toward Zeolite-based catalysts. These catalysts provide improved sulfur removal and better fuel quality outcomes.

By Application Analysis

FCC catalysts led the By Application segment with a 38.2% market share in 2024. This leadership stems from FCC catalysts’ critical role in converting heavy crude oils into high-value products. The process transforms crude oil into gasoline and diesel efficiently.

FCC catalysts enhance conversion rates, improve selectivity, and reduce energy consumption for global refineries. Therefore, growing fuel demand and stringent environmental regulations support continued segment growth. Ongoing technological advancements further strengthen FCC catalyst performance and market dominance.

Drivers

The Indian government actively advances zeolite production through research funding initiatives. The Science and Engineering Research Board provides financial assistance for zeolite-related projects under the Department of Science and Technology. Consequently, this support accelerates domestic catalyst manufacturing capabilities and reduces import dependence.

National Aluminium Company Limited developed indigenous technology for detergent-grade Zeolite-A, licensed through the National Research Development Corporation. This achievement showcases the successful translation of government-supported research into industrial production. Therefore, continued government backing will likely expand zeolite applications across refining sectors.

Use Cases

Refinery catalysts enable the processing of heavier crude oil grades that would otherwise prove difficult to refine. For example, hydrocracking catalysts convert low-value heavy residues into high-demand diesel and jet fuel. This capability allows refineries to purchase cheaper crude feedstocks while producing premium products.

Catalysts also play essential roles in meeting ultra-low sulfur fuel specifications globally. Hydrotreating catalysts remove sulfur compounds from gasoline and diesel, reducing harmful emissions from vehicles. Consequently, refineries without advanced catalyst systems cannot comply with modern environmental regulations in major markets.

Major Challenges

High raw material costs, particularly for precious metals like platinum and palladium, constrain catalyst manufacturing profitability. These metals serve as active components in many hydrocracking and reforming catalysts. Therefore, price volatility directly impacts production costs and final catalyst pricing for refineries.

Stringent environmental regulations governing catalyst disposal and regeneration create additional compliance burdens. Spent catalysts often contain heavy metals and require specialized handling procedures. Consequently, refineries must invest in proper disposal infrastructure or third-party services, increasing operational expenses.

Business Opportunities

Government funding for Fluid Catalytic Cracking catalyst innovation opens new market opportunities. Indian institutions like the Centre for High Technology and the Oil Industry Development Board actively support research projects. For instance, the development of sulfur-reduction catalysts for FCC gasoline received government backing, creating commercialization pathways.

Bharat Petroleum Corporation Limited issued a tender for 900 metric tons of fresh FCC catalyst, demonstrating government facilitation of advanced technology adoption. Such procurement activities signal sustained demand for innovative catalyst solutions. Therefore, manufacturers focusing on next-generation FCC catalysts will find ready markets in public sector refineries.

Regional Analysis

Asia Pacific dominated the Refinery Catalysts Market with a 44.8% share valued at USD 2.6 billion in 2024. This leadership reflects the region’s expanding refining infrastructure and high petroleum product consumption. Rapid industrialization across China and India drives continuous catalyst demand growth.

North America and Europe remain notable contributors through ongoing refinery upgrades and advanced catalytic technology adoption. The Middle East & Africa and Latin America also support market growth through capacity expansion projects. However, Asia Pacific’s strategic importance continues to grow as companies focus on meeting rising energy demands efficiently.

Top Key Players in the Market

- Albemarle Corporation

- BASF SE

- Johnson Matthey Plc

- W. R. Grace

- Clariant International Ltd.

- Arkema

- Zeolyst International

- Chevron Corporation

- Exxon Mobil Corporation

- Evonik Industries AG

- DuPont

- Haldor Topsoe A/S

Conclusion

The Global Refinery Catalysts Market demonstrates steady growth driven by clean fuel demand and regulatory pressure. Asia Pacific leads global consumption, while zeolite and FCC catalysts dominate product and application segments, respectively. Moreover, government funding initiatives across India and other regions accelerate catalyst innovation and domestic production capabilities. Market challenges include high raw material costs and disposal regulations, yet opportunities abound in next-generation catalyst development.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)