Table of Contents

Introduction

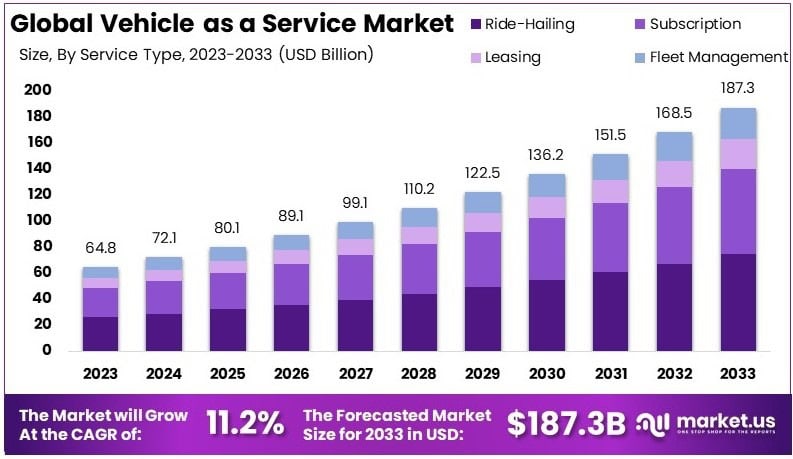

New York, NY – April 09, 2025 – The global Vehicle as a Service (VaaS) market is projected to reach approximately USD 187.3 billion by 2033, increasing from an estimated USD 64.8 billion in 2023. This growth reflects a compound annual growth rate (CAGR) of 11.2% during the forecast period from 2024 to 2033.

Vehicle as a Service (VaaS) refers to a comprehensive mobility solution wherein vehicles are offered to consumers or businesses through a subscription-based or usage-based model, eliminating the need for ownership. This service typically includes access to a vehicle, maintenance, insurance, and other value-added services under a single monthly fee or on-demand pricing structure. The Vehicle as a Service market encompasses the global ecosystem of service providers, technology enablers, and fleet operators facilitating this mobility shift.

Market growth is primarily driven by the rising urbanization, increasing cost of vehicle ownership, and the growing consumer preference for flexible and sustainable mobility options. The widespread adoption of digital platforms and mobile applications has further simplified the user experience, boosting consumer adoption rates. Demand is notably rising in metropolitan regions where congestion, parking limitations, and environmental concerns are prompting consumers and enterprises to opt for more efficient transportation models.

Additionally, the proliferation of electric vehicles (EVs) and advancements in telematics and connectivity are enhancing the value proposition of VaaS offerings. Corporates are increasingly adopting fleet-as-a-service models to reduce operational expenditures and improve resource utilization. An emerging opportunity lies in the integration of artificial intelligence and predictive analytics to personalize offerings and optimize fleet performance.

Furthermore, regulatory support for shared mobility and zero-emission goals is expected to catalyze market expansion across North America, Europe, and Asia-Pacific. As consumers shift from ownership to usership, the VaaS market is poised to play a central role in the future of urban transportation, presenting lucrative avenues for innovation and investment.

Key Takeaways

- The Vehicle as a Service (VaaS) Market was valued at USD 64.8 billion in 2023 and is projected to reach USD 187.3 billion by 2033, expanding at a CAGR of 11.2% during the forecast period.

- Ride-Hailing Services emerged as the leading service type segment in 2023, primarily due to their convenience, real-time accessibility, and increasing consumer preference for on-demand mobility solutions.

- Passenger Vehicles dominated the vehicle type segment in 2023, attributed to their widespread application in both personal and commercial service-based transport services.

- Telematics-Based Solutions held the largest share in the technology integration segment in 2023, supported by their role in enhancing vehicle connectivity, tracking, and data-driven decision-making.

- The Individual Consumer segment led the end-user category in 2023, driven by the growing demand for flexible, affordable, and personalized mobility options.

- North America was the dominant regional market in 2023, supported by its advanced digital infrastructure, high urbanization rates, and early adoption of service-oriented vehicle business models.

Obtain A Sample Copy Of This Report at https://market.us/report/vehicle-as-a-service-market/request-sample/

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 64.8 Billion |

| Forecast Revenue (2033) | USD 187.3 Billion |

| CAGR (2024-2033) | 11.2% |

| Segments Covered | By Service Type (Subscription Services, Leasing Services, Fleet Management Services, Ride-Hailing Services), By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles), By Technology Integration (Connected Vehicle Solutions, Autonomous Vehicle Integration, Telematics-Based Solutions), By End-User (Individual Consumers, Businesses or Corporates, Government and Public Sector) |

| Competitive Landscape | BMW Group, Daimler AG, Ford Motor Company, Volvo Car Corporation, Toyota Motor Corporation, Uber Technologies Inc., Lyft Inc., DiDi Chuxing, Grab, Ola, Cluno GmbH, Fair Financial Corp., Borrow, Carbar, Carly, Harman International Industries, Inc., Facedrive Inc., Primemover Mobility Technologies Pvt Ltd. |

Emerging Trends

- Shift from Ownership to Usership: Consumers are increasingly favoring flexible vehicle access over traditional ownership, opting for subscription-based models that offer convenience and cost-effectiveness.

- Integration of Electric Vehicles (EVs): There is a growing incorporation of EVs into VaaS offerings, aligning with global efforts to reduce carbon emissions and promote sustainable transportation.

- Advancements in Autonomous Vehicle Technology: Investments are being made in autonomous taxis to enhance safety and efficiency, with the potential to revolutionize the VaaS landscape.

- Digital Platform Development: The creation of robust digital platforms is facilitating seamless user experiences, enabling easy access to vehicle services through smartphones and other devices.

- Data-Driven Decision Making: Utilization of big data analytics is optimizing fleet management and personalizing customer experiences, leading to more efficient operations.

Top Use Cases

- Corporate Fleet Management: Businesses are leveraging VaaS for flexible fleet solutions, allowing them to scale vehicle usage based on demand without the burden of ownership.

- Ridesharing and Ride-Hailing Services: VaaS is underpinning services that provide on-demand transportation, reducing the need for personal vehicle ownership.

- Short-Term Vehicle Access: Individuals are utilizing VaaS for short-term needs, such as vacations or temporary work assignments, benefiting from the flexibility it offers.

- Subscription-Based Vehicle Access: Consumers are subscribing to vehicle services that allow them to switch between different car models based on their needs and preferences.

- Electric Vehicle Adoption: VaaS is facilitating the transition to EVs by providing access without the high upfront costs, encouraging broader adoption.

Major Challenges

- Depreciation and Resale Value Concerns: Leasing models are under pressure due to uncertainties in the resale values of vehicles, particularly EVs, affecting profitability.

- Regulatory Compliance: Navigating varying regulations across regions poses challenges for VaaS providers in standardizing their services.

- Infrastructure Limitations: Inadequate charging infrastructure for EVs can hinder the expansion of VaaS offerings that include electric vehicles.

- Market Competition: The increasing number of entrants into the VaaS market intensifies competition, necessitating differentiation strategies.

- Consumer Trust and Adoption: Building consumer confidence in the reliability and benefits of VaaS is essential for widespread adoption.

Top Opportunities

- Expansion into Emerging Markets: There is potential for growth in regions with increasing urbanization and demand for flexible transportation solutions.

- Partnerships with EV Manufacturers: Collaborations can enhance VaaS offerings by integrating the latest EV models, appealing to environmentally conscious consumers.

- Development of Autonomous Vehicle Services: Investing in autonomous technology can position VaaS providers at the forefront of innovation in mobility services.

- Enhanced Digital User Experiences: Improving app interfaces and user engagement can attract tech-savvy customers seeking convenience.

- Sustainable Mobility Solutions: Offering eco-friendly vehicle options aligns with global sustainability goals and can attract environmentally conscious users.

Key Player Analysis

Global Vehicle as a Service (VaaS) Market in 2024, the competitive landscape is shaped by a mix of established automotive giants and agile mobility service providers. Leading automakers such as BMW Group, Daimler AG, Ford Motor Company, Volvo Car Corporation, and Toyota Motor Corporation are leveraging their extensive manufacturing expertise and global reach to integrate subscription-based and on-demand mobility models into their business portfolios. These companies are focusing on fleet electrification, connectivity, and in-house mobility platforms to capture growing consumer demand for flexible vehicle usage.

Simultaneously, tech-driven mobility companies such as Uber Technologies Inc., Lyft Inc., DiDi Chuxing, Grab, and Ola are expanding their ride-hailing and shared mobility services, investing in AI-based route optimization, and forming strategic alliances with automakers. Emerging players like Cluno GmbH, Fair Financial Corp., Borrow, Carbar, Carly, and Primemover Mobility are disrupting traditional vehicle ownership models through app-based vehicle subscriptions, while Harman International and Facedrive Inc. enhance value through connected vehicle technologies and sustainability-focused offerings.

Purchase The Full Report Now at https://market.us/purchase-report/?report_id=134736

Key Players in the Market

- BMW Group

- Daimler AG

- Ford Motor Company

- Volvo Car Corporation

- Toyota Motor Corporation

- Uber Technologies Inc.

- Lyft Inc.

- DiDi Chuxing

- Grab

- Ola

- Cluno GmbH

- Fair Financial Corp.

- Borrow

- Carbar

- Carly

- Harman International Industries, Inc.

- Facedrive Inc.

- Primemover Mobility Technologies Pvt Ltd.

Recent Developments

- In 2024, CEFC and Splend expanded their EV efforts in Australia with an additional $20 million investment. This follows an earlier 2023 investment that added 500 electric vehicles to Splend’s rideshare fleet in under six months. The fresh funding lifts CEFC’s total support to $40 million, aimed at reducing petrol car use and supporting the shift to clean transport.

- In 2023, WeFlex secured £40 million funding from LCM Partners to grow its electric vehicle offerings for ride-hailing drivers in the UK. With this funding, over 1,300 new EVs are set to join the fleet, helping meet the high demand for zero-emission vehicles. WeFlex already operates more than 2,000 EVs, and the new support is expected to drive faster fleet electrification.

- In 2024, Waymo raised $5.6 billion to expand its robotaxi operations across more cities in the U.S. The autonomous driving unit of Alphabet plans to use the funding to scale services in Los Angeles, San Francisco, and Phoenix. Investors included Alphabet, a16z, Fidelity, Silver Lake, and Tiger Global, highlighting strong backing for the self-driving future.

- In 2024, General Motors announced its decision to exit the robotaxi business and redirect focus to personal vehicle technologies. The automaker plans to strengthen its Super Cruise system rather than continue investing in its Cruise unit. GM cited long development timelines and increased competition as reasons for this move.

- In 2025, Tesla will launch its first Robotaxi service in Austin, Texas, introducing a fully driverless ride model. The new system will operate without a human driver or remote supervision, marking a significant step in Tesla’s autonomous vehicle journey.

- In 2024, Rimac introduced its autonomous rideshare service Verne at its campus in Croatia. The service features a newly designed two-seater vehicle and aims to redefine urban mobility. Inspired by author Jules Verne, the project reflects Rimac’s ambition to shape the future of transportation.

Conclusion

The Vehicle as a Service (VaaS) market is evolving rapidly, supported by growing urbanization, digital adoption, and a clear shift from ownership to usership. Advancements in electric and autonomous vehicle technologies, coupled with rising environmental awareness and regulatory support for shared mobility, are strengthening the market’s foundation. Despite challenges such as infrastructure gaps and regulatory complexity, opportunities remain strong in emerging regions, fleet electrification, and AI-powered mobility solutions. As service providers and automakers continue to innovate, VaaS is expected to become a key pillar in the global mobility ecosystem.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)