Table of Contents

Introduction

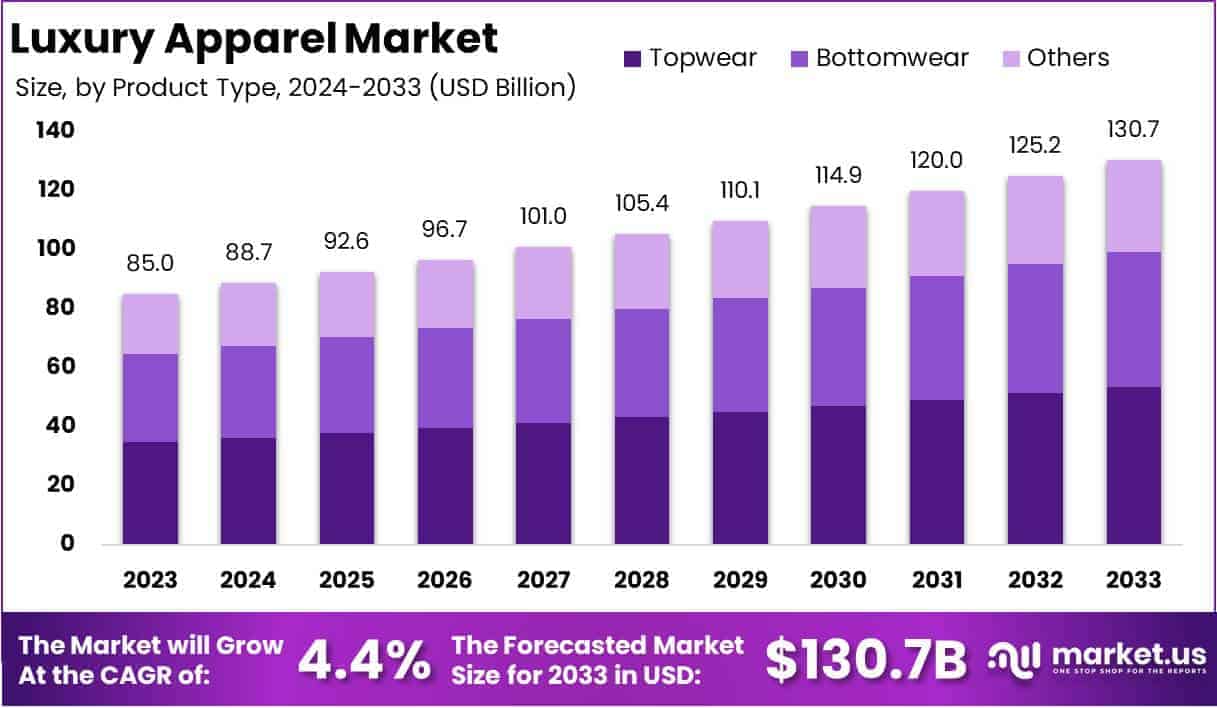

The Global Luxury Apparel Market is projected to reach a valuation of approximately USD 130.7 billion by 2033, up from USD 85.0 billion in 2023. This represents a compound annual growth rate CAGR of 4.4% over the forecast period from 2024 to 2033.

Luxury apparel refers to high-end clothing and accessories characterized by superior craftsmanship, premium materials, and exclusive designs. These products are typically associated with well-established brands that cater to affluent consumers seeking to express status, sophistication, and personal style. Luxury apparel spans various categories, including haute couture, ready-to-wear, and limited-edition collections, and often incorporates elements of heritage and innovation.

The luxury apparels market encompasses the global industry focused on the production, distribution, and retail of high-end clothing. This market includes a broad range of players, from iconic luxury fashion houses to emerging brands that emphasize exclusivity and quality. The market is highly competitive, with a strong emphasis on brand reputation, consumer experience, and innovation. Distribution channels range from flagship stores and exclusive boutiques to online platforms and partnerships with luxury department stores.

The growth of the luxury apparels market is driven by several key factors. Rising disposable incomes in emerging markets, particularly in Asia-Pacific regions such as China and India, have expanded the customer base for luxury products. Additionally, the growing influence of social media and digital marketing has enabled luxury brands to reach a broader, more diverse audience. The increasing emphasis on sustainability and ethical production has also prompted many luxury brands to innovate, tapping into the growing demand for environmentally conscious products.

Demand for luxury apparel remains resilient, even amid economic uncertainties. High-net-worth individuals (HNWIs) continue to be the primary consumers, but younger demographics, including Millennials and Gen Z, are emerging as influential segments. This younger audience is driving demand for casual luxury, athleisure, and collaborations between high-fashion and streetwear brands. Additionally, there is a notable shift toward personalized and experiential luxury, with consumers seeking products that reflect their individuality and values.

The luxury apparels market presents several opportunities for growth and differentiation. Digital transformation, including e-commerce and virtual showrooms, has created new avenues for engagement and sales. Moreover, the rise of the metaverse and digital fashion presents untapped potential for luxury brands to establish their presence in virtual spaces.

Emerging markets, particularly in Africa and Southeast Asia, offer significant growth potential as their middle classes expand and consumer preferences evolve. Lastly, the increasing consumer focus on sustainability provides an opportunity for brands to innovate through circular fashion, including recycled materials and rental services.

Key Takeaways

- The global luxury apparel market is forecasted to expand from USD 85.0 billion in 2023 to USD 130.7 billion by 2033, achieving a steady CAGR of 4.4% over the period.

- Topwear accounts for 41% of the market, highlighting strong consumer preference for visible, brand-centric pieces that signal status.

- The women’s segment accounts for 63% of the market, highlighting the significant purchasing power and influence of female consumers in the luxury apparel sector.

- Offline stores continue to dominate with a 67% market share, reflecting the ongoing importance of experiential, in-person shopping in the luxury segment.

- The Asia-Pacific region holds the largest share at 38.2%, propelled by rising wealth and brand-conscious consumers, particularly in markets like China and India.

Luxury Apparels Statistics

- 58% of Americans prefer U.S.-made clothing.

- Nearly 70% prioritize eco-friendly clothing.

- Over 60% plan to shop more sustainably.

- 35% choose brands aligned with their values.

- Over 40% intend to increase spending on eco-friendly apparel.

- Each American discards over 80 pounds of clothing annually.

- 64% favor sustainable fashion.

- The average American buys 68 clothing items yearly.

- 48% prefer ethically sourced clothing.

- Women’s and girls’ clothing dominate 52% of U.S. apparel sales.

- 80% of the U.S. apparel workforce is female.

- Apparel contributes 0.8% to U.S. GDP.

- Over 1.8 million people work in U.S. apparel retail.

- Fast fashion accounts for 20% of global production; the U.S. is a major market.

- Men’s clothing sales are forecasted to grow 10% in five years.

- Athleisure holds 30% of the U.S. apparel market.

- Footwear sales in the U.S. are expected to reach $105 billion in 2023.

- Work uniforms generate $10 billion in U.S. revenue.

- Top luxury brands allocate 5-7% of revenue to marketing.

- Accessories contribute 30% to global luxury fashion revenue.

- Over 4,397 fashion designers are employed in the U.S.

- U.S. apparel market growth is projected at 2.82% annually.

- Fashion contributes 2% to global GDP.

- 59% of 18-34-year-olds prefer sustainable luxury fashion.

- Luxury fashion spending averages $4,563 per U.S. consumer annually.

- 65% of luxury buyers cite quality as the top purchase driver.

- Luxury fashion comprises 60% of the global luxury market.

- 76% of luxury brands operate e-commerce platforms.

- Digital influencers impact 85% of luxury purchases.

- Male consumers make up 42% of global luxury fashion purchases.

- Demand for limited edition luxury items rose by 35%.

- Luxury athleisure grew 18% in 2023.

- Social media influences 70% of luxury buying decisions.

- Mobile shopping accounts for 56% of online luxury purchases.

- The fashion industry produces 92 million tonnes of textile waste annually.

- Apparel industry emissions are projected to increase by 50% by 2030.

- An average U.S. consumer throws away 81.5 lbs of clothes each year.

- The number of times a garment is worn has dropped by 36% in 15 years.

- Fashion accounts for 20% of global wastewater production.

- Producing 1 kg of cotton requires 20,000 liters of water.

- $500 billion is lost annually due to under-wearing and lack of recycling.

- Global fiber production reached 124 million tonnes in 2023, a 7% increase.

Emerging Trends

- Emphasis on Core Products and Heritage: Brands are refocusing on their signature items and heritage to strengthen market position. For instance, Burberry is centering its strategy on classic trench coats and scarves to revitalize its brand identity.

- Rise of ‘Quiet Luxury’: There’s a growing preference for understated elegance over conspicuous branding. Consumers are favoring high-quality, subtle designs that reflect sophistication without overt logos, a trend often referred to as “quiet luxury.”

- Integration of Outdoor Aesthetics: The ‘gorpcore’ trend, which blends outdoor and utilitarian styles, is influencing luxury fashion. Brands like Arc’teryx are gaining popularity among urban consumers seeking functional yet stylish apparel.

- Sustainability and Circular Fashion: There’s an increasing focus on sustainability, with brands adopting circular fashion models. Initiatives such as in-house resale programs and the use of eco-friendly materials are becoming more prevalent.

- Digital Engagement and E-commerce Expansion: Luxury brands are enhancing their digital presence to meet the growing demand for online shopping. This includes leveraging social media platforms and developing robust e-commerce channels to reach a broader audience.

Top Use Cases

- Personalized Customer Experiences: Luxury brands are utilizing data analytics to tailor shopping experiences. By analyzing customer preferences and purchase histories, companies can offer personalized product recommendations and exclusive offers, leading to a 30-50% increase in digital sales.

- Inventory Optimization: Advanced analytics enable brands to manage inventory more effectively. By predicting demand patterns, companies can reduce overstock and stockouts, resulting in a 10% increase in sales through optimized stock levels.

- Enhanced Supply Chain Management: Data-driven insights allow for improved supply chain operations. Real-time tracking and predictive analytics help in anticipating disruptions, ensuring timely product availability and reducing lead times by up to 20%.

- Targeted Marketing Campaigns: By analyzing consumer behavior and market trends, luxury brands can design more effective marketing strategies. This targeted approach can lead to a 15% increase in customer engagement and higher conversion rates.

- Product Development and Innovation: Leveraging big data, brands can identify emerging fashion trends and consumer preferences, informing the design of new products. This approach has led to a 20% reduction in time-to-market for new collections.

Major Challenges

- Economic Uncertainty and Market Volatility: Global economic fluctuations have led to decreased consumer spending on luxury goods. For instance, the global luxury goods market is projected to decline by 2% in 2025, from €369 billion in 2024 to €363 billion in 2025, marking the first contraction since the Great Recession.

- Shifting Consumer Preferences: There’s a growing demand for sustainability and ethical practices in fashion. Brands failing to adapt may lose relevance, as consumers increasingly prioritize environmental responsibility. The global fashion industry, including luxury segments, is under pressure to reduce its environmental impact, with 92 million tons of clothing-related waste discarded annually.

- Digital Transformation and E-commerce Competition: The rise of online shopping has intensified competition, requiring luxury brands to enhance their digital presence. In 2024, e-commerce is expected to account for approximately 39% of fashion industry sales, underscoring the need for robust online strategies.

- Counterfeiting and Brand Dilution: The proliferation of counterfeit luxury goods, especially through social media platforms, undermines brand integrity and results in significant revenue losses. Studies indicate that 20% of items tagged with luxury brand names on Instagram are counterfeit, highlighting the scale of this issue.

- Supply Chain Disruptions: Global events, such as pandemics and geopolitical tensions, have disrupted supply chains, leading to production delays and increased costs. The COVID-19 pandemic, for example, caused a 7% sales drop and a 9% decline in net profit for luxury brand Hermès in 2020.

Top Opportunities

- Expansion into Emerging Markets: Regions such as India, Southeast Asia, and Africa are experiencing economic growth and an expanding affluent consumer base. Targeting these markets can lead to significant revenue increases, as the global luxury market is projected to grow by 2% to 4% in 2025, with emerging markets contributing substantially.

- Adoption of Sustainable Practices: Consumers are increasingly valuing environmental responsibility. Implementing sustainable sourcing and production methods can attract eco-conscious buyers, aligning with the trend towards sustainability in the fashion industry.

- Leveraging Digital Channels: Enhancing online presence through e-commerce platforms and social media engagement can tap into the growing online luxury market, which is expected to account for a significant portion of sales in the coming years.

- Personalization and Customization: Offering tailored products and experiences can meet the demand for unique luxury items, fostering customer loyalty and potentially increasing sales.

- Integration of Technology and Innovation: Incorporating advanced technologies such as augmented reality (AR) for virtual try-ons and blockchain for product authentication can enhance customer experience and trust, setting brands apart in a competitive market.

Key Player Analysis

- Gucci: Founded in 1921, Gucci is an Italian luxury fashion house renowned for its high-end clothing, accessories, and leather goods. In 2023, Gucci’s brand value was estimated at $15.6 billion, reflecting its strong market presence. However, the brand faced challenges in 2024, reporting a 25% decline in revenue for Q3, attributed to decreased demand in the Asia Pacific region.

- Prada S.p.A. : Established in 1913, Prada is an Italian luxury fashion company known for its sophisticated designs and high-quality products. In the first half of 2024, Prada reported a 20% increase in retail sales, indicating robust growth. The company’s strategic focus on brand elevation and product innovation has contributed to its positive performance.

- Dior SE: Christian Dior SE, commonly known as Dior, is a French luxury goods company founded in 1946. In 2022, Dior reported revenues of €79.18 billion, showcasing its significant market influence. The brand continues to expand its product lines and global presence, maintaining a strong position in the luxury market.

- Ralph Lauren Corporation : Founded in 1967, Ralph Lauren Corporation is an American fashion company known for its premium lifestyle products. In the fiscal second quarter of 2024, the company reported revenues of $1.726 billion, surpassing estimates and reflecting a 3% increase from the previous year. This growth was driven by strong performance in North America and Asia.

- Armani S.p.A.: Established in 1975, Armani is an Italian luxury fashion house offering a range of products, including apparel and accessories. The company has maintained a strong brand presence, with revenues estimated at €2.5 billion in 2023. Armani continues to focus on brand diversification and digital expansion to sustain its market position.

Recent Developments

- In 2023, Tapestry, Inc. (NYSE: TPR), owner of brands like Coach, Kate Spade, and Stuart Weitzman, announced its acquisition of Capri Holdings Limited (NYSE: CPRI), the parent of Versace, Jimmy Choo, and Michael Kors. Capri shareholders will receive $57.00 per share, valuing the deal at $8.5 billion.

- In 2023, Frasers Group acquired luxury retailer Matches for $65.9 million in cash from Apax Partners’ subsidiary, MF Intermediate Limited, strengthening its presence in high-end fashion.

- In 2024, Authentic Brands Group acquired Sperry, a heritage footwear brand. As part of the deal, ALDO Group will handle Sperry’s North American operations and global footwear production.

- In 2024, OTB Group took a majority stake in Calzaturificio Stephen, a long-time footwear supplier for Margiela’s iconic Tabi shoe. This aligns with OTB’s strategy to boost supply chain efficiency and preserve Italian craftsmanship.

- In 2024, Cult Mia, a UK-based luxury platform, raised over €4.6 million in seed funding to drive global growth and reinforce its position in independent luxury fashion.

Conclusion

The luxury apparel market is poised for sustained growth, driven by rising disposable incomes, evolving consumer preferences, and technological advancements. Brands that strategically align with these dynamics emphasizing sustainability, digital engagement, and personalized experiences are well-positioned to capitalize on emerging opportunities. However, navigating challenges such as economic fluctuations, shifting consumer expectations, and supply chain complexities will require agility and innovation. Success in this competitive landscape will depend on a brand’s ability to adapt to market trends while maintaining the exclusivity and quality that define luxury apparel.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)