Overview

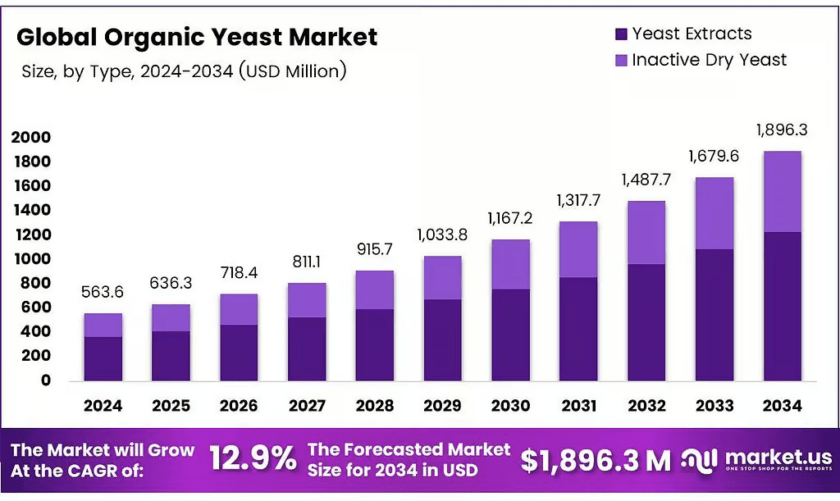

New York, NY – May 22, 2026 – The Global Organic Yeast Market expects significant growth from USD 563.6 million in 2024 to USD 1896.3 million by 2034. This expansion represents a compound annual growth rate (CAGR) of 12.9% during the forecast period from 2025 to 2034. Market analysts attribute this growth to rising consumer preferences for natural and organic food ingredients worldwide.

Organic yeast cultivation uses raw materials from organic origins with strict processing standards. EU organic regulations permit only a maximum of 5% processing aids to maintain consistent production quality. Unlike conventional methods that use ammonia as a nitrogen source, organic yeast relies on plant-derived nitrogen compounds. The fermentation media contains various plant-based ingredients that provide essential nutrients for proper yeast growth and development.

Yeast thrives best at temperatures between 30–37 °C and prefers neutral or slightly acidic pH conditions. Temperatures above 37 °C cause stress, while exposure above 50°C leads to cell death. Interestingly, exposing yeast to a 7% salt solution before bulk fermentation triggers glycerol buildup in cell walls. This glycerol transfers to dough and bread during baking, effectively enhancing final product texture and moisture retention.

Key Takeaways

- The Global Organic Yeast Market projects growth from USD 563.6 million in 2024 to USD 1896.3 million by 2034 at a 12.9% CAGR.

- Yeast Extracts dominate the By Type segment with a 65.9% share in 2024, driven by demand for natural umami flavor in clean-label products.

- Dry form leads the By Form segment with a 75.4% share in 2024, valued for stability and ease of use in baking and dry mixes.

- Food and Beverages hold a 59.3% share in the By Application segment in 2024, fueled by organic trends in breads, beers, and probiotic snacks.

- North America commands 43.9% market share, representing USD 247.4 million in 2024, led by clean-label awareness and sustainable manufacturing practices.

➤ See the Full TOC, Market Tables & Figures in Your Sample Copy – https://market.us/report/organic-yeast-market/request-sample/

Market Segmentation

By Type

Yeast Extracts held a dominant market position in 2024 with a 65.9% share of the By Type segment. This sub-segment thrives as manufacturers increasingly seek natural flavor enhancers for their clean-label product lines. Extracting nutrients from organic yeast boosts umami flavor profiles and supports food fortification initiatives. Consequently, demand rises steadily in savory snacks and ready meal applications.

Inactive Dry Yeast captures a significant yet secondary role within the organic yeast market landscape. Producers favor this form for its long shelf life and easy incorporation into baking and fermentation processes. This yeast variety retains essential vitamins and proteins, which appeals to bakers crafting organic breads and pastries. Additionally, rising sustainability trends support eco-friendly supply chains and foster expansion in niche gluten-free product markets.

By Form

Dry form held a dominant market position in 2024 with a 75.4% share of the By Form Analysis segment. This form excels in practicality by offering extended stability without requiring refrigeration for storage. Its powdered consistency integrates seamlessly into dry mixes and nutritional supplements, fueling widespread adoption across the baking industry. Consequently, organic certifications increasingly emphasize quality preservation during product transit and logistics management.

Liquid form serves as a vital alternative in the organic yeast market, prized for immediate activation in brewing and fresh dough preparations. While requiring careful handling to maintain cell viability, this form delivers superior fermentation efficiency that enhances product freshness. Brewers and artisanal producers increasingly turn to liquid organic yeast for premium organic beers and wines. This form effectively bridges application gaps requiring rapid microbial activity despite inherent storage challenges.

By Application

Food and Beverages held a dominant market position in 2024 with a 59.3% share of the By Application Analysis segment. This sector surges as organic trends reshape consumer palates and purchasing decisions worldwide. Manufacturers incorporate organic yeast for leavening and flavor enhancement in breads, beers, and fermented foods. Health-conscious consumers further propel its use in probiotic-rich yogurts and healthy snacks, amplifying overall market pull.

Animal Feed emerges as a key application pillar for organic yeast, enhancing livestock nutrition without synthetic additives. Farmers integrate organic yeast into feed to boost gut health and immunity in poultry and cattle operations. This application gains significant traction as regulations tighten on conventional feed quality standards. Better yields and improved animal welfare result from organic feed adoption, supporting resilient supply chains for organic producers globally.

Regional Analysis

North America held a dominant 43.9% market share in 2024, valued at approximately USD 247.4 million in the global organic yeast market. Strong consumer awareness about clean-label ingredients and sustainable food manufacturing practices drives this regional leadership position. The United States stands at the forefront, supported by the USDA National Organic Program and growing retail demand for certified organic foods.

European markets follow closely behind North America, driven by the EU Organic Action Plan targeting 25% of farmland under organic cultivation by 2030. This policy expands the organic supply base and nudges retail demand toward certified organic products. Germany, France, and the United Kingdom represent key growth markets where organic yeast fits naturally into clean-label product formulations.

Drivers

Rising consumer demand for organic, clean-label food ingredients drives significant growth in the organic yeast market. In the United States, organic retail food sales grew from approximately USD 11 billion to an estimated USD 52 billion over recent years. This influx of shoppers seeking organic and minimally processed foods pushes manufacturers toward ingredients like organic yeast.

Food companies increasingly recognize that organic yeast helps align product formulations with evolving consumer preferences and clean-label trends. Government initiatives and regulatory frameworks also support this market expansion effectively. The USDA’s National Organic Program provides certification, labeling, and enforcement mechanisms that help consumers trust organic claims.

Moreover, certified organic cropland increased by 79% according to USDA data, pointing to broadening organic agriculture capacity nationwide. The Strengthening Organic Enforcement rule entered full compliance, expanding oversight, traceability, and certification coverage for businesses handling organic products.

Use Cases

Organic food brands increasingly use organic yeast extracts to reduce sodium content while preserving robust flavor profiles. This application aligns with government-backed nutrition goals and evolving organic regulations that explicitly include yeast within product scope. Demand tailwinds remain strong on the market side as consumers seek salt-reduced, flavor-forward ready meals and snacks.

Organic ready meals, soups, and plant-based items particularly benefit from organic yeast’s ability to improve taste naturally. Animal nutrition represents another growing use case where organic yeast enhances livestock health without synthetic additives.

Farmers integrate organic yeast into poultry and cattle feed to boost gut health and strengthen immune system function. This application gains traction as regulations tighten on feed quality standards and conventional antibiotic use. Better animal welfare outcomes and improved production yields result from organic yeast adoption, supporting resilient supply chains for organic livestock operations.

Business Opportunities

Growing consumer demand for organic and clean-label products creates substantial opportunities for organic yeast manufacturers. The U.S. organic food market reached USD 63.8 billion in 2023, part of total certified organic product sales reaching USD 69.7 billion. This represents a year-on-year increase of approximately 3.4%, showing sustained appetite for organic foods that avoid synthetic additives.

Food manufacturers respond by reformulating products with organic yeast, which meets clean-label expectations while delivering functional benefits. Expanding applications in nutraceuticals and wellness supplements offer additional growth avenues for market players. Organic yeast provides natural vitamin enrichment and serves as a clean-label ingredient for dietary supplements.

The bioactive compounds found in organic yeast appeal to health-conscious consumers seeking functional foods and natural wellness products. Emerging bio-based product categories and therapeutic applications represent untapped potential for innovative companies willing to invest in research and development.

Major Challenges

Higher input costs and tighter compliance requirements raise organic yeast prices compared to conventional alternatives. Yeast manufacturers rely on sugar or molasses as fermentation feedstock, and sugar prices have swung sharply in recent years. The FAO Sugar Price Index dropped 21.3% year-on-year in September 2025 after earlier price spikes. This volatility complicates contracting and inventory planning for organic processors who must maintain strict certification standards throughout their supply chains.

Strengthening Organic Enforcement rules adds compliance burdens that increase operating costs for market participants. These regulations expand oversight, traceability requirements, and certification coverage for businesses handling organic products. While these safeguards build consumer trust and market integrity, they also add audits, documentation, and supplier vetting steps. Importers, distributors, and processors buying organic yeast face higher operating costs that ultimately pass through to end consumers.

Top Key Players in the Market

- Lesaffre Group

- Angel Yeast Co. Ltd.

- Lallemand Inc.

- Koninklijke DSM N.V.

- Kerry Group plc

- Biorigin

- Biospringer

- Synergy Flavors

- AB Mauri

- Levapan S.A.

- Ohly GmbH

- Oriental Yeast Co. Ltd.

- Givaudan

- Kothari Fermentation and Biochem Ltd.

Conclusion

The global organic yeast market enters a strong growth phase driven by clean-label trends and rising consumer health awareness. North America leads the current market share, while Europe and the Asia Pacific present substantial expansion opportunities for forward-looking companies. Yeast extracts and dry formulations dominate their respective segments, with food and beverages remaining the primary application area. Despite challenges from input cost volatility and regulatory compliance burdens, market fundamentals remain positive for organic yeast producers worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)