Table of Contents

Overview

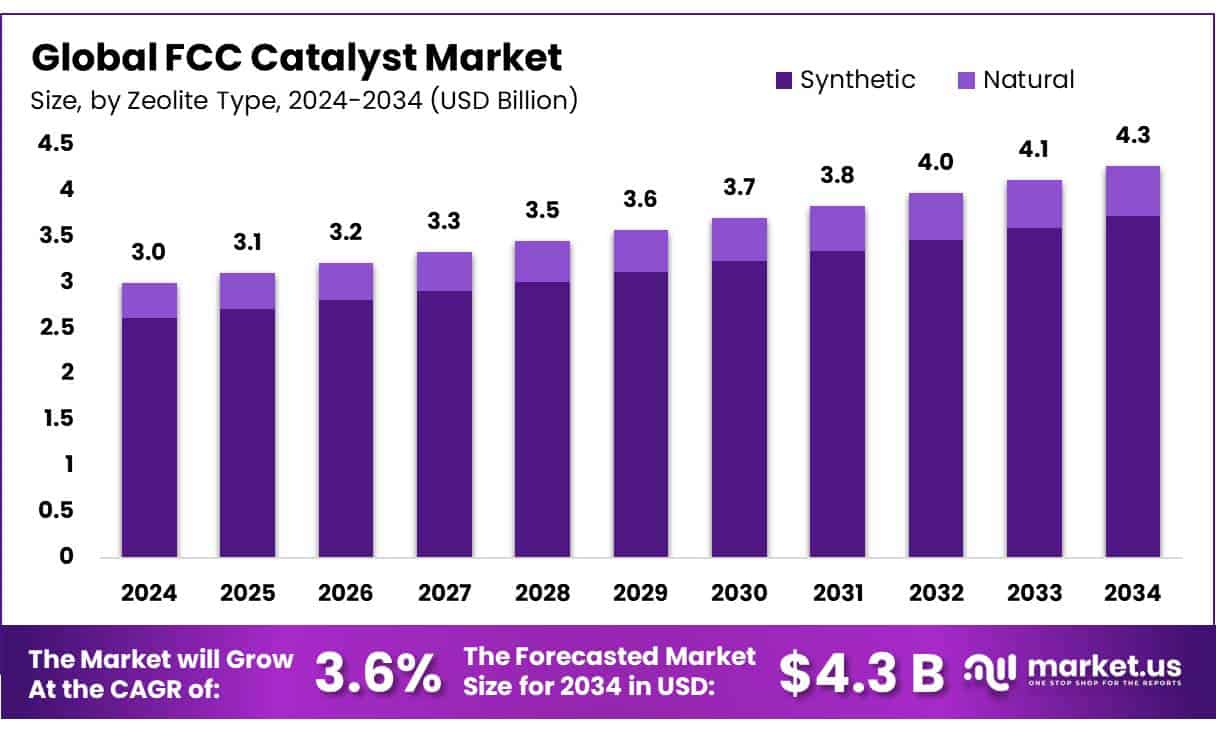

New York, NY – July 01, 2025 – The Global FCC Catalyst Market is witnessing strong growth, driven by the rising demand for refined petroleum products like gasoline, diesel, and petrochemicals. Valued at USD 3.0 billion in 2024, the market is projected to reach USD 4.3 billion by 2034, growing at a CAGR of 3.6% during the forecast period from 2025 to 2034.

The FCC catalyst market is divided by zeolite type into natural and synthetic categories. In 2024, synthetic zeolites captured a commanding 87.2% revenue share, driven by their superior catalytic performance, selectivity, and durability compared to natural zeolites. The FCC catalyst market is segmented by unit type into side-by-side and stacked configurations.

In 2024, side-by-side units led with a 68.3% market share, attributed to their proven design, operational reliability, and ease of maintenance. By application, the FCC catalyst market is segmented into Vacuum Gas Oil, Residue, and others. In 2024, Vacuum Gas Oil accounted for 56.3% of the market share, owing to its widespread use as a preferred feedstock in FCC units.

Key Takeaways

- The global FCC catalyst market was valued at USD 3.0 billion in 2024.

- The global FCC catalyst market is projected to grow at a CAGR of 3.6% and is estimated to reach USD 4.3 billion by 2034.

- Among zeolite types, Synthetic accounted for the largest market share of 87.2%. Due to its superior catalytic activity, higher selectivity, and enhanced durability compared to natural zeolites.

- Among FCC unit types, the side-by-side type accounted for the majority of the market share at 68.3%.

- By process, maximum middle distillates accounted for the largest market share of 34.5%. Due to the growing demand for cleaner-burning diesel and jet fuels.

- By application, vacuum gas oil accounted for the majority of the market share at 56.3%. Owing to its widespread use as a preferred feedstock in FCC units.

- Asia Pacific is estimated as the largest market for FCC catalyst with a share of 37.3% of the market share.

How Growth is Impacting the Economy

The FCC catalyst market’s growth significantly influences the global economy by supporting the petroleum refining industry, a cornerstone of energy production. As demand for cleaner fuels rises, refineries invest heavily in advanced catalysts, boosting job creation in the manufacturing and R&D sectors. The market’s expansion, particularly in Asia-Pacific, drives economic activity in emerging economies like China and India, where increased refining capacity fuels industrial growth and infrastructure development. Additionally, the shift toward biofuels creates new economic opportunities through innovation in catalyst formulations. However, high investment costs and regulatory compliance challenges may strain smaller refineries, potentially impacting local economies.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/global-fcc-catalyst-market/request-sample/

Strategies for Businesses

Businesses in the FCC catalyst market should focus on innovation, developing advanced catalysts with higher selectivity and environmental compliance to meet stringent regulations. Strategic partnerships with refineries can enhance market reach and foster collaborative R&D for biofuel-compatible catalysts. Expanding into high-growth regions like Asia-Pacific, particularly China and India, can capitalize on rising refining capacities. Additionally, investing in nanotechnology and sustainable production processes can improve catalyst efficiency and reduce emissions, aligning with global sustainability goals. Companies should also prioritize cost optimization to address high operational expenses, ensuring competitive pricing and market resilience.

Report Scope

| Market Value (2024) | USD 4.3 Billion |

| Forecast Revenue (2034) | USD 3.0 Billion |

| CAGR (2025-2034) | 3.6% |

| Segments Covered | By Zeolite Type (Natural, Synthetic), By FCC Unit Type (Side-by-side Type, Stacked-Type), By Process (Gasoline Sulfur Reduction, Maximum Light Olefins, Maximum Middle Distillates, Maximum Bottoms Conversion, Others), By Application (Vacuum Gas Oil, Residue, Others) |

| Competitive Landscape | BASF SE, W. R. Grace and Company, Albemarle Corporation, Johnson Matthey, Equilibrium Catalyst, Inc., Topsoe, JGC C&C, Sinopec, Clariant AG, Rezel Catalysts Corporation, Anten Chemical Co., Ltd., SINOCATA, KNT Group, Nouryon, Other Key Players |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=150474

Key Market Segments

Zeolite Type Analysis: Synthetic Zeolites Lead FCC Catalyst Market

- The FCC catalyst market is divided by zeolite type into natural and synthetic categories. In 2024, synthetic zeolites captured a commanding 87.2% revenue share, driven by their superior catalytic performance, selectivity, and durability compared to natural zeolites.

- Engineered with tailored pore structures and acidity levels, synthetic zeolites excel in cracking heavy hydrocarbons into high-value products like gasoline and olefins. Advancements in synthetic zeolite technology have further enhanced product yields, minimized coke formation, and supported compliance with strict environmental regulations, solidifying their dominance in modern refining.

FCC Unit Type Analysis: Side-by-Side Units Hold Market Lead

- The FCC catalyst market is segmented by unit type into side-by-side and stacked configurations. In 2024, side-by-side units led with a 68.3% market share, attributed to their proven design, operational reliability, and ease of maintenance.

- Featuring separate cracking and regeneration reactors, this setup offers precise control over the cracking process and catalyst regeneration. The widespread use of side-by-side units in existing refineries, coupled with their compatibility with diverse feedstocks, reinforces their market dominance and drives demand for compatible FCC catalysts.

Process Analysis: Maximum Middle Distillates Segment Tops Market

- The FCC catalyst market is categorized by process into Gasoline Sulfur Reduction, Maximum Light Olefins, Maximum Middle Distillates, Maximum Bottoms Conversion, and others. In 2024, Maximum Middle Distillates held the largest share at 34.5%, fueled by rising demand for cleaner diesel and jet fuels.

- Stricter environmental regulations on sulfur and nitrogen oxide emissions have increased the need for high-quality middle distillates. The growing transportation and industrial sectors, along with a focus on ultra-low sulfur diesel (ULSD) and fuel efficiency, have made catalysts optimized for middle distillate production critical for refineries.

Application Analysis: Vacuum Gas Oil Segment Dominates

- By application, the FCC catalyst market is segmented into Vacuum Gas Oil, Residue, and others. In 2024, Vacuum Gas Oil accounted for 56.3% of the market share, owing to its widespread use as a preferred feedstock in FCC units. Its balanced quality and cost make it ideal for producing valuable lighter products like gasoline and olefins. Additionally, Vacuum Gas Oil’s lower sulfur content aligns with stringent environmental standards, enabling cleaner fuel production. Its availability and favorable processing traits drive strong demand for FCC catalysts tailored to its conversion.

Regional Analysis

- Asia Pacific led the global FCC catalyst market, capturing a 37.3% share, fueled by rapid industrialization and rising demand for transportation fuels like gasoline and diesel. Growing economies such as China and India are expanding refinery capacities to meet energy demands, adopting advanced FCC units to optimize yields from heavier crude feedstocks. Stringent environmental regulations, particularly for ultra-low sulfur diesel (ULSD), are driving refiners to use high-performance FCC catalysts that support cleaner fuel production with lower emissions.

- Innovations in catalyst formulations are boosting refinery efficiency, improving selectivity for high-value products like butylene and propylene while reducing coke and dry gas output. The growing petrochemical sector also increases demand for advanced FCC catalysts, essential for chemical production. Supported by government policies, evolving feedstock qualities, and a focus on cleaner, more efficient fuel production, the Asia Pacific FCC catalyst market is poised for continued growth.

Recent Developments

1. BASF SE

- BASF has introduced Futuria, a next-generation FCC catalyst designed to maximize propylene yield while maintaining gasoline production. The catalyst incorporates advanced zeolite technology to enhance selectivity and stability. BASF is also focusing on sustainability, reducing CO₂ emissions in refinery operations. Their innovations aim to meet the rising demand for petrochemical feedstocks.

2. W. R. Grace and Company

- Grace has launched Aster, a novel FCC catalyst platform that improves bottom-upgrading and increases light olefin yields. Their MIDAS technology enhances metal resistance, extending catalyst life. Grace is also advancing carbon reduction initiatives, aligning with refineries’ decarbonization goals.

3. Albemarle Corporation

- Albemarle’s Action 400 FCC catalyst series boosts gasoline and alkylate yields while reducing coke formation. Their HYDEX E catalysts improve LCO (Light Cycle Oil) quality for diesel production. Albemarle is investing in R&D to optimize catalysts for renewable feedstocks.

4. Johnson Matthey

- Johnson Matthey’s Jupiter FCC catalysts enhance propylene and butylene yields for petrochemical integration. Their SOxGETTER additives reduce sulfur emissions. The company is also developing solutions for co-processing biofeeds in FCC units.

5. Equilibrium Catalyst, Inc.

- Equilibrium Catalyst specializes in E-CAT recycling and rejuvenation, offering cost-effective alternatives to fresh catalysts. Their services help refiners optimize FCC performance while reducing waste. They also provide catalyst testing and evaluation for process improvements.

Conclusion

The FCC Catalyst Market is poised for steady growth, driven by demand for cleaner fuels and regulatory pressures. Its economic impact is profound, fostering job creation and industrial expansion, particularly in Asia-Pacific. Businesses can thrive by innovating and targeting high-growth regions, while analysts remain optimistic about the market’s future due to technological advancements and sustainability trends. Despite challenges like high costs, the market’s trajectory supports a resilient refining industry, ensuring continued economic contributions and alignment with global energy goals.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)