Overview

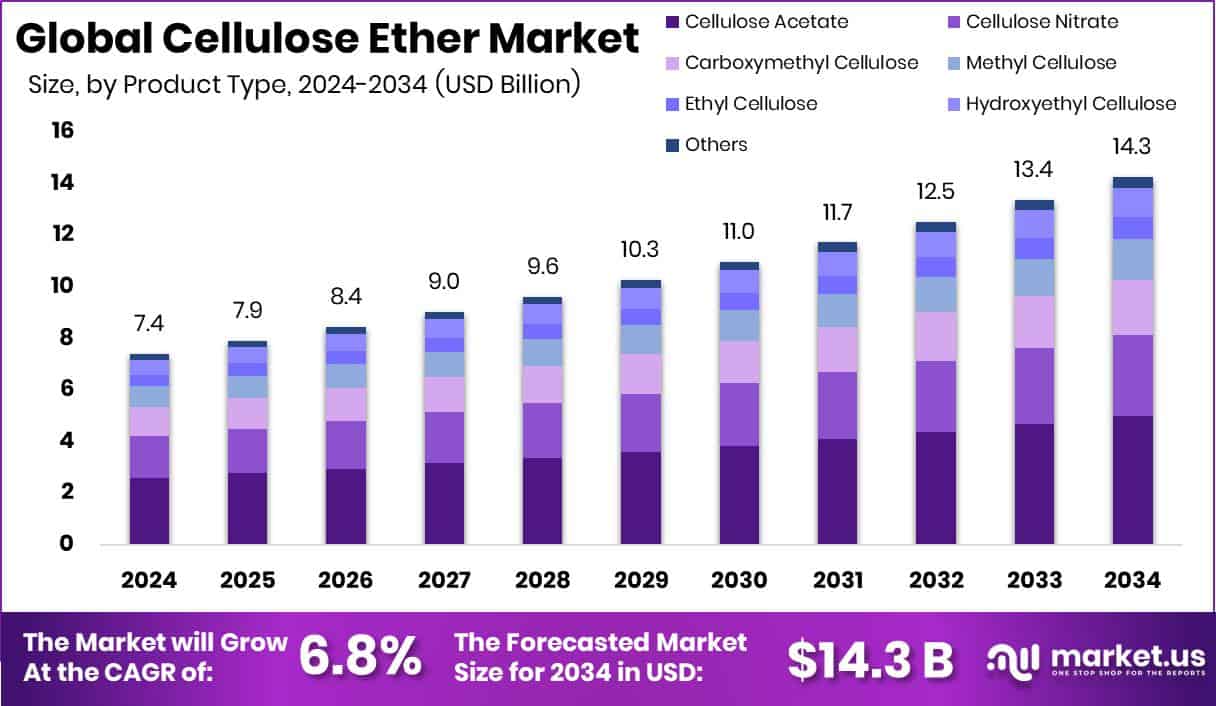

New York, NY – June 20, 2025 – The Global Cellulose Ether Market is projected to soar from USD 7.4 billion in 2024 to an impressive USD 14.3 billion by 2034, achieving a robust CAGR of 6.8% during the 2025–2034 forecast period.

In 2024, Cellulose Acetate led the Cellulose Ether Market’s product type segment, commanding a 39.3% share. Its prominence is driven by extensive use in construction, pharmaceuticals, and personal care industries. The Powder Form dominated the Cellulose Ether Market’s physical form segment with a 76.1% share.

Its preference stems from ease of handling, long shelf life, and compatibility with dry formulations. The Kraft process held a 65.9% share in the Cellulose Ether Market’s process segment. Renowned for producing high-purity cellulose with minimal impurities, it is the preferred method for cellulose ether manufacturing.

Key Takeaways

- Global Cellulose Ether Market is expected to be worth around USD 14.3 billion by 2034, up from USD 7.4 billion in 2024, and grow at a CAGR of 6.8% from 2025 to 2034.

- In 2024, Cellulose Acetate led the Cellulose Ether Market by Product Type with 39.3% share.

- Powder form dominated the Physical Form segment of the Cellulose Ether Market, accounting for 76.1% in 2024.

- The Kraft process held a strong 65.9% share in the Cellulose Ether Market by Process in 2024.

- The Asia-Pacific cellulose ether industry reached a market value of USD 3.2 billion.

How Growth is Impacting the Economy

- The Cellulose Ether Market’s robust growth significantly impacts global economies. In construction, cellulose ethers enhance material performance, supporting infrastructure projects in emerging markets like China and India, creating jobs and boosting GDP. In pharmaceuticals, their use in drug formulations drives healthcare advancements, increasing employment in R&D and manufacturing.

- The food and personal care sectors benefit from eco-friendly stabilizers, aligning with consumer sustainability demands, thus stimulating retail and green economies. Asia-Pacific’s 43.3% market share underscores regional economic growth, with investments in production facilities enhancing trade and industrial output. However, raw material price volatility may challenge cost stability, necessitating strategic supply chain management to sustain economic benefits.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/global-cellulose-ether-market/request-sample/

Strategies for Businesses

- Businesses in the cellulose ether market should focus on innovation, developing high-purity, customized products for niche applications in pharmaceuticals and cosmetics. Expanding production in Asia-Pacific, leveraging low-cost labor and high demand, can enhance competitiveness. Strategic partnerships with raw material suppliers can mitigate price volatility risks.

- Emphasizing sustainability through bio-based products aligns with consumer trends, boosting brand value. Investing in R&D for advanced manufacturing processes, like the Kraft method, ensures quality and efficiency. Finally, diversifying applications into emerging sectors like oil drilling and textiles can capture new revenue streams, strengthening market position.

Report Scope

| Market Value (2024) | USD 7.4 Billion |

| Forecast Revenue (2034) | USD 14.3 Billion |

| CAGR (2025-2034) | 6.8% |

| Segments Covered | By Product Type (Cellulose Acetate, Cellulose Nitrate, Carboxymethyl Cellulose, Methyl Cellulose, Ethyl Cellulose, Hydroxyethyl Cellulose, Others), By Physical Form (Flake (Coarse Flake, Fine Flake), Granule, Powder), By Process (Kraft, Sulfite) |

| Competitive Landscape | The Dow Chemical Company, Shin-Etsu Chemical Co., Ltd., DKS Co., Ltd., Daicel Corporation, Ashland, AkzoNobel N.V. |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=149876

Key Market Segments

By Product Type Analysis

- In 2024, Cellulose Acetate led the Cellulose Ether Market’s product type segment, commanding a 39.3% share. Its prominence is driven by extensive use in construction, pharmaceuticals, and personal care industries. With superior film-forming, thickening, and stabilizing properties, Cellulose Acetate excels in water-based formulations like paints, wall putties, and drug delivery systems. In construction, it enhances moisture retention and workability in cement and gypsum products, particularly in rapidly urbanizing developing economies.

- The pharmaceutical industry bolsters its dominance, leveraging Cellulose Acetate in sustained-release drug formulations for improved stability and patient compliance. In personal care, it’s safe, skin-friendly thickening properties that cater to growing hygiene and skincare demand. As a bio-based, biodegradable material, Cellulose Acetate aligns with global sustainability trends, ensuring its continued leadership through reliability and regulatory compliance.

By Physical Form Analysis

- In 2024, the powder form dominated the Cellulose Ether Market’s physical form segment with a 76.1% share. Its preference stems from ease of handling, long shelf life, and compatibility with dry formulations. Powdered cellulose ether is widely used in construction for dry-mix mortars, tile adhesives, and plasters, offering uniform dispersion and precise dosing critical for performance.

- In pharmaceuticals, it serves as a binder and disintegrant in tablets, ensuring quality and stability. In food processing, it acts as a thickener and stabilizer in ready-mix products. The powder form’s versatility, cost-effective packaging, storage, and transport advantages solidify its lead across high-volume, moisture-sensitive applications in multiple industries.

By Process Analysis

- In 2024, the Kraft process held a 65.9% share in the Cellulose Ether Market’s process segment. Renowned for producing high-purity cellulose with minimal impurities, it is the preferred method for cellulose ether manufacturing. The process extracts long cellulose fibers from wood pulp, yielding high-quality raw material ideal for construction, pharmaceuticals, food, and cosmetics.

- Its reliability, consistency, and scalability meet industrial demands, with Kraft-derived cellulose ether enhancing viscosity and water retention in mortars and adhesives for construction and ensuring low contaminant levels for pharmaceutical compliance. The process’s efficient chemical recovery and reduced waste align with sustainability goals, while its established global supply chain reinforces its dominance in 2024.

Regional Analysis

- In 2024, the Asia-Pacific region led the Cellulose Ether Market, capturing a 43.3% share with a market value of USD 3.2 billion. This dominance stems from robust growth in construction and pharmaceuticals, especially in China, India, and Southeast Asia, fueled by infrastructure projects and generic drug production. Rising demand for construction chemicals, personal care products, and food additives further drove cellulose ether consumption.

- North America and Europe held stable market positions, supported by consistent demand in pharmaceuticals, processed foods, and premium cosmetics, aided by strict regulations and a focus on sustainable, bio-based materials. Latin America and the Middle East & Africa saw modest growth, with increasing industrial activity and urbanization in countries like Brazil, the UAE, and South Africa. Asia-Pacific’s edge lies in its manufacturing strength, abundant raw materials, and expanding end-use industries, solidifying its market leadership.

Recent Developments

1. The Dow Chemical Company

- Dow has been advancing its METHOCEL cellulose ethers, focusing on sustainability and performance in construction, pharmaceuticals, and food. Recent innovations include low-viscosity grades for better workability in tile adhesives and gypsum-based products. Dow emphasizes eco-friendly solutions, reducing carbon footprints in building materials.

2. Shin-Etsu Chemical Co., Ltd.

- Shin-Etsu has expanded its CELNY methyl cellulose and hydroxypropyl methylcellulose (HPMC) production to meet rising demand in Asia. The company is enhancing product purity for pharmaceutical applications, including controlled-release tablets and ophthalmic solutions.

3. DKS Co. Ltd.

- DKS has introduced CELOGEN, a new cellulose ether series for construction, improving water retention and adhesion in mortars. The company is also optimizing production processes to reduce environmental impact while maintaining high-performance standards.

4. Daicel Corporation

- Daicel is innovating in CEOLUS microcrystalline cellulose and ether derivatives for pharmaceuticals, enhancing excipient performance in tablet formulations. The company is also investing in bio-based materials to support greener manufacturing.

5. Ashland

- Ashland’s AQUALON and BENECEL cellulose ethers are seeing increased adoption in plant-based meat alternatives as texture stabilizers. The company has also launched new HPMC grades for improved drug solubility in solid-dose medications.

6. AkzoNobel N.V.

- AkzoNobel (via Nouryon) has been developing Ethocel ethyl cellulose for advanced drug delivery systems. They are also focusing on sustainable cellulose ethers for coatings and construction materials, aligning with circular economy goals.

Conclusion

The Cellulose Ether Market is growing due to rising demand in construction, pharmaceuticals, and food industries. Companies like Dow, Shin-Etsu, and Ashland are focusing on sustainable, high-performance products, such as low-viscosity grades for construction and excipients for drug formulations. Asia-Pacific is a key growth region, driven by construction and pharmaceutical needs. Innovations in bio-based and eco-friendly cellulose ethers are gaining traction as industries push for greener solutions.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)