Table of Contents

Overview

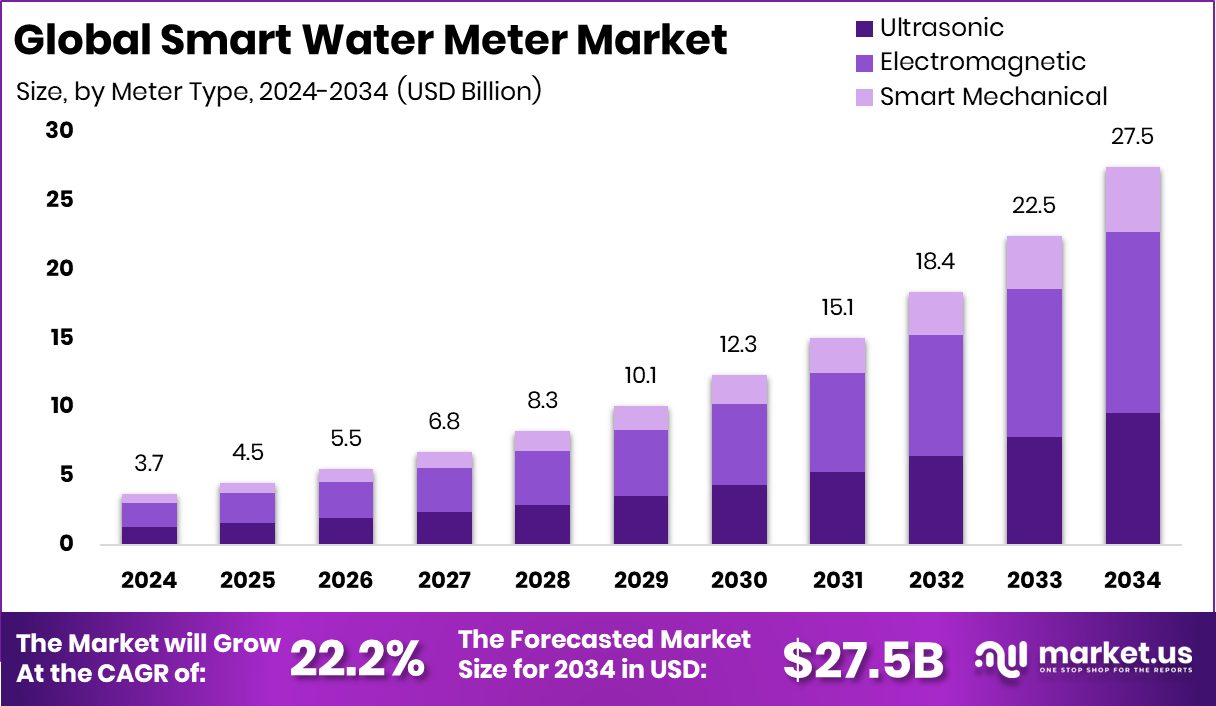

New York, NY – March 20, 2026 – The global smart water meter market is experiencing rapid growth, projected to rise from USD 3.7 billion in 2024 to around USD 27.5 billion by 2034, driven by strong adoption across utilities and infrastructure upgrades. These digital meters enable real-time monitoring of water usage, eliminating manual readings while improving leak detection, efficiency, and system transparency.

The market includes hardware, communication networks, and software solutions used across residential, commercial, and municipal systems. Large deployments—such as 1.4 million meters in Puerto Rico and projects saving up to 1.5 billion litres of water annually—highlight their role in conservation and operational efficiency. North America remains a dominant region, accounting for 46.3% of revenue, or USD 1.7 billion.

Government support is a major growth driver, with investments like $153 million for Arkansas water infrastructure and $80 million for Bahrain’s Al Dur expansion. Additional initiatives include Japan’s $3.5 million grant and deployment of 8,400 meters in Faisalabad.

Rising water scarcity and accountability concerns are increasing demand, though cases like Greece’s €500 million overspending probe demonstrate the importance of efficient execution. Innovation is also accelerating, supported by funding such as $35 million for an Israeli leak-detection startup, $6 million in Series A IoT funding, $2 million raised by Comminent in India, and over Rs 3 crore granted to an IIT Kanpur-incubated startup.

➤ Click the sample report link for complete industry insights: https://market.us/report/global-smart-water-meter-market/request-sample/

Key Takeaways

- The Global Smart Water Meter Market is expected to be worth around USD 27.5 billion by 2034, up from USD 3.7 billion in 2024, and is projected to grow at a CAGR of 22.2% from 2025 to 2034.

- In the Smart Water Meter Market, electromagnetic meters dominate with 47.8% share.

- Within Smart Water Meter Market applications, water utilities lead adoption at 67.2%.

- AMI technology drives Smart Water Meter Market growth, accounting for 58.9% deployments.

- Radio-frequency proprietary RF dominates Smart Water Meter Market communication technologies at 49.3%.

- Retrofit and replacement deployments lead Smart Water Meter Market implementation with 67.9%.

- Residential usage represents the major Smart Water Meter Market application segment, holding 59.5%.

- North America’s dominance reflects strong adoption, holding 46.3% share and USD 1.7 Bn.

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=174449

Market Segments

By Meter Type Analysis

Electromagnetic meters dominate the Smart Water Meter Market with a 47.8% share in 2024, driven by superior accuracy, durability, and ability to measure both low and high flow rates. Their design, which excludes moving parts, minimizes maintenance and ensures long-term performance. Utilities favor these meters for large pipelines and seamless integration with digital monitoring systems.

Increasing focus on reducing non-revenue water and improving billing precision further strengthens demand. Additionally, growing investments in water infrastructure and stricter regulations for accurate measurement continue to support the widespread adoption of electromagnetic technology across both developed and emerging markets.

By Application Analysis

Water utilities lead the Smart Water Meter Market with a 67.2% share, driven by global infrastructure modernization efforts. Utilities are adopting smart meters to enhance efficiency, detect leaks early, and improve demand forecasting. Real-time monitoring and remote reading capabilities reduce manual work and billing inaccuracies.

Government funding and digital water initiatives are accelerating adoption, particularly in regions facing water scarcity and aging systems. As utilities shift toward data-driven operations and sustainability goals, smart metering has become essential for improving service quality, optimizing resource management, and ensuring reliable water distribution, reinforcing the segment’s dominant market position.

By Technology Analysis

Advanced Metering Infrastructure (AMI) leads the market with a 58.9% share due to its ability to provide real-time, two-way communication between meters and utilities. AMI enables remote readings, faster issue detection, and advanced data analytics for better water distribution management. Utilities are increasingly transitioning from traditional AMR systems to AMI for improved efficiency and transparency.

Its compatibility with smart city platforms and utility management software enhances its value. Long-term cost savings, improved operational control, and the ability to reduce water losses are key factors driving widespread AMI adoption across modern water networks.

By Communication Technology Analysis

Proprietary radio-frequency (RF) communication dominates with a 49.3% share, supported by its reliability, secure data transmission, and strong performance in complex environments such as dense urban areas. Utilities prefer RF systems due to lower operational costs compared to cellular networks and reduced reliance on external telecom providers. These networks offer scalability, allowing easy expansion of smart metering systems while maintaining consistent data flow. Their ability to function effectively in underground and challenging conditions makes them ideal for large-scale deployments, ensuring uninterrupted communication and reinforcing their leading position in smart water metering projects globally.

By Deployment Analysis

Retrofit and replacement deployments hold a 67.9% share, reflecting utilities’ focus on upgrading existing infrastructure. Aging mechanical meters are being replaced with smart meters to improve accuracy and reduce water losses. This approach is cost-effective and minimizes disruption compared to new installations.

Utilities and municipalities are prioritizing replacement programs to meet regulatory standards and sustainability goals. The ability to integrate smart meters into existing pipelines and billing systems accelerates adoption. As budget constraints persist, retrofit strategies remain the preferred method for modernizing water networks while maintaining operational efficiency.

By Application Analysis

The residential segment leads with a 59.5% share, driven by urbanization, smart city initiatives, and rising awareness of water conservation. Smart meters provide households with real-time consumption data, helping reduce waste and manage utility expenses. Utilities benefit from improved billing accuracy and fewer disputes.

Government programs promoting digital infrastructure and efficient resource usage further support residential adoption. As concerns over water scarcity grow and smart home technologies expand, residential smart water metering continues to see steady demand, making it the largest and most consistent application segment in the overall market.

Regional Analysis

North America leads the Smart Water Meter Market with a 46.3% share, valued at USD 1.7 billion, driven by early adoption, advanced utility infrastructure, and strong regulatory focus on efficiency and leakage control. Europe follows with steady growth supported by sustainability goals, conservation policies, and the modernization of urban water systems.

Asia Pacific is a fast-growing region, driven by rapid urbanization, expanding residential sectors, and rising awareness of water loss management in developing economies.

The Middle East & Africa region is gaining traction as water scarcity drives demand for efficient monitoring solutions. Meanwhile, Latin America shows gradual adoption, supported by infrastructure upgrades and rising interest in digital technologies to enhance service reliability and reduce water losses.

Top Use Cases

- Leak Detection and Prevention: Smart water meters help detect leaks quickly by tracking unusual water usage patterns in real time. If there is continuous or abnormal flow, the system sends alerts so problems can be fixed early. This prevents water loss and damage.

- Accurate Billing for Consumers: These meters record exact water usage and send data automatically, so users are billed only for what they consume. This reduces billing errors and improves fairness for households and businesses.

- Real-Time Water Monitoring: Smart meters provide live data on water consumption through apps or dashboards. Users and utilities can track usage anytime, helping them make better decisions and reduce wastage.

- Reducing Water Waste and Saving Resources: By identifying excessive use and leaks, smart meters help conserve water. Utilities can act quickly to stop losses, improving overall water efficiency.

- Remote Meter Reading and Lower Costs: Smart meters remove the need for manual meter reading. Data is sent automatically, saving labor time and reducing operational costs for utilities.

- Better Water Management for Utilities: Utilities use smart meter data to plan water supply, predict demand, and improve system performance. This helps in managing networks more efficiently and reducing non-revenue water losses.

Notable Company Developments

- In May 2025, Hubbell (through its Aclara brand) supported a smart water project in Santa Barbara using RF-based AMI systems. This helped reduce manual meter reading and gave customers tools to track water usage easily, improving efficiency and transparency in water management.

- In September 2024, BMETERS upgraded its Bmetering Keygenerator portal by adding LoRaWAN key visibility features. This allows users to view and manage device data securely, improving connectivity and smart meter system management.

- In May 2024, Diehl Metering (a company that provides smart water and energy metering solutions) launched the HYDRUS 2.0 ultrasonic water meter with LoRaWAN connectivity. This new meter improves data transmission range and supports remote monitoring, helping utilities manage water usage more efficiently.

Conclusion

The Smart Water Meter Market is growing rapidly as utilities and governments focus on efficient water management, cost reduction, and sustainability. Advanced technologies like AMI, IoT connectivity, and real-time monitoring are improving accuracy, reducing water losses, and enabling better decision-making. Strong public investments and infrastructure upgrades continue to support adoption worldwide. Increasing water scarcity and the need for transparent billing further drive demand across residential and utility sectors. While challenges like high initial costs and implementation issues remain, ongoing innovation and funding are creating new opportunities. Overall, smart water meters are becoming essential for modern, data-driven water management systems globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)