Table of Contents

Market Overview

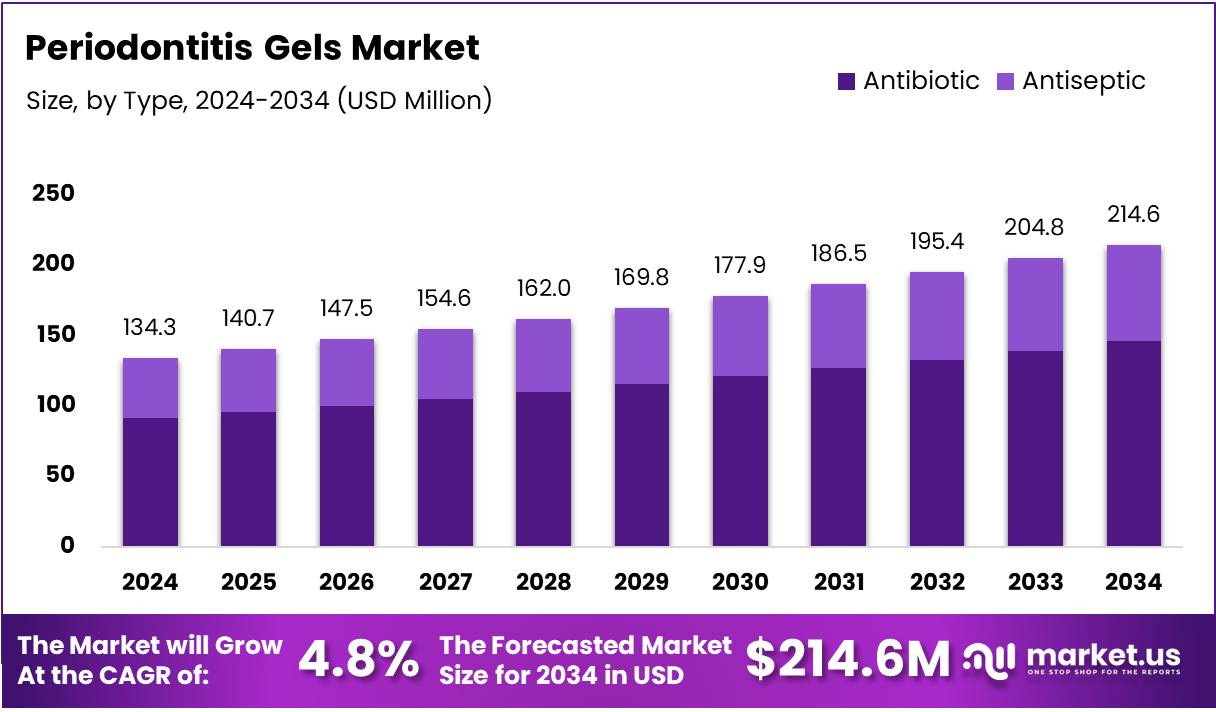

The global periodontitis gels market is valued at USD 134.3 Million in 2024 and is projected to reach USD 214.6 Million by 2034. This growth reflects a compound annual growth rate of 4.8% over the forecast period from 2025 to 2034. Expanding patient populations and rising clinical adoption drive this sustained upward trajectory.

Periodontitis gels are specialized pharmaceutical formulations applied directly to infected gum tissue. They contain antimicrobial agents, anti-inflammatory compounds, and tissue regeneration promoters. Dental professionals use them as minimally invasive alternatives to surgical periodontal intervention. Both prescription-grade and over-the-counter versions target varying levels of disease severity.

Multiple healthcare sectors actively adopt these therapeutic gels across diverse treatment settings. Hospital periodontal departments manage complex cases involving severe infections and post-surgical recovery. Private dental clinics deploy gels for routine preventive care and early-stage interventions. Community health centers increasingly distribute them to reach underserved patient populations.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Advanced drug delivery technologies are significantly improving gel performance and patient outcomes. Manufacturers now engineer bioadhesive gels that stay in periodontal pockets longer, extending antimicrobial action. Combination formulations integrate multiple active ingredients in a single application. These innovations reduce treatment frequency, improve compliance, and strengthen competitive differentiation among product developers.

Government health programs and regulatory frameworks are actively expanding market access and product standards. Public oral health initiatives increase treatment infrastructure in emerging economies. Regulatory agencies such as the FDA and EMA establish quality and safety benchmarks that protect patients while encouraging innovation. Compliance with these frameworks helps manufacturers build credibility in professional dental channels.

Clinical data confirms the scale of the unmet need driving this market. Research shows 42.2% of adults aged 30 or older experience some form of periodontitis. Severe periodontitis affects 7.8% of this group, while nonsevere forms account for 34.4%. Among all dentate adults, periodontitis prevalence reaches approximately 62%. These figures establish a massive patient base validating long-term commercial opportunity.

Key Takeaways

- The global periodontitis gels market is projected to reach USD 214.6 Million by 2034, up from USD 134.3 Million in 2024, at a 4.8% CAGR.

- By type, the Antibiotic segment dominated in 2024 with a market share of 65.9%, reflecting strong clinical preference for targeted bacterial elimination.

- By category, Degradable gels led the market in 2024, accounting for 59.1% share due to patient convenience and bio-absorbable design.

- By application, the Hospital segment held the largest share of 48.3% in 2024, driven by complex periodontal case management.

- North America led all regions with a market share of 34.8%, generating revenue of USD 46.7 Million.

- Asia Pacific is the fastest-growing region, supported by urbanization and rising private dental clinic expansion.

- Natural and herbal-based gel formulations are gaining traction, with neem, aloe vera, and tea tree oil emerging as key ingredients.

Market Segmentation Overview

The Antibiotic segment commands 65.9% of the type-based market in 2024. This dominance reflects dental professionals’ strong preference for targeted bacterial elimination using agents like doxycycline and minocycline. Sustained-release mechanisms reduce treatment frequency, improving patient compliance. Consequently, manufacturers continue prioritizing antibiotic-based development in their periodontal product pipelines.

Antiseptic gels serve a complementary role using chlorhexidine to reduce bacterial load with broader coverage. Their lower resistance risk and prescription-free availability make them suitable for preventive and mild-condition management. They function effectively as maintenance therapy following initial antibiotic treatment. Moreover, their accessibility supports adoption in community and over-the-counter settings.

Degradable gels hold 59.1% of the category segment, driven by superior patient convenience. These bio-absorbable formulations dissolve naturally inside periodontal pockets, eliminating the need for professional removal. Consistent drug release supports optimal healing throughout recovery. Their alignment with natural tissue regeneration makes them a preferred choice among modern dental practitioners.

Non-degradable gels remain relevant for cases requiring precise therapeutic control. Dentists choose them when close monitoring of drug release duration is clinically necessary. They allow custom treatment protocols for complex or atypical periodontal conditions. Additionally, their removal procedure provides a structured endpoint, which supports treatment planning in institutional settings.

Hospitals account for 48.3% of application-based demand due to their infrastructure for severe disease management. These facilities handle multi-disciplinary cases involving systemic conditions that complicate periodontal health. Therefore, hospitals represent the primary clinical channel for aggressive periodontitis treatment using gel-based therapies. Clinics and alternative channels serve the balance of demand across preventive and moderate-severity cases.

Drivers

The rising global burden of periodontal disease creates sustained and scalable demand for therapeutic gels. Research confirms that 42.2% of adults aged 30 and older experience periodontitis, generating massive patient volumes. Aging populations further expand this base, particularly in developed markets with longer life expectancies. Dental professionals respond by adopting gel therapies as routine adjuncts to standard periodontal care.

Advances in bioactive and controlled-release gel technology are directly improving clinical outcomes. Modern formulations deliver active compounds over extended periods directly within periodontal pockets. This targeted approach reduces systemic exposure while maximizing local therapeutic impact. Consequently, practitioners gain greater confidence in prescribing gel therapies as evidence of superior efficacy grows across clinical settings.

Use Cases

Hospital periodontal departments use these gels extensively to manage severe and complex gum infections. Patients with systemic conditions such as diabetes often experience worsened periodontitis requiring intensive topical treatment. Gels applied post-surgically support tissue regeneration and prevent bacterial recurrence. This clinical application drives nearly half of all market demand across global healthcare facilities.

Additionally, private dental clinics deploy periodontitis gels as frontline tools for preventive and early-stage care. Practitioners prescribe them at the first signs of gum disease to prevent progression to surgical intervention. Patients benefit from easy self-application and minimal discomfort. This use case supports growing adoption as clinics shift toward minimally invasive treatment philosophies.

Major Challenges

Stringent regulatory approval processes in major markets create significant barriers for manufacturers. Obtaining FDA or EMA clearance requires lengthy clinical trials, extensive documentation, and substantial financial investment. These requirements delay product launches by several years and disproportionately burden smaller companies. Consequently, innovation cycles slow and market entry costs remain high across the global competitive landscape.

However, limited patient awareness of advanced periodontal gel therapies restrains demand growth, especially in developing regions. Many patients first learn about gel-based treatments only after reaching advanced disease stages. This knowledge gap reduces early adoption rates and limits revenue potential in high-prevalence markets. Improved patient education and dental outreach programs remain essential to closing this awareness gap.

Business Opportunities

Growing consumer preference for personalized healthcare creates strong opportunity for targeted periodontal gel development. Patients increasingly seek formulations tailored to specific disease severity, lifestyle, or ingredient preferences. Manufacturers that offer specialized products for different periodontitis stages can capture premium pricing. Therefore, investment in customized gel portfolios aligns directly with shifting patient expectations and clinical demand.

Moreover, the expansion of e-commerce and direct-to-consumer platforms opens new distribution pathways for oral care products. Online channels bypass traditional retail intermediaries, reducing cost and expanding reach into underserved markets. Digital platforms also enable manufacturers to educate consumers about early-stage treatment options. This distribution shift supports broader adoption and accelerates revenue growth, particularly in regions with limited physical dental retail access.

Regional Analysis

North America leads the global periodontitis gels market with 34.8% share and revenues of USD 46.7 Million in 2024. High periodontal disease awareness, strong preventive dental care habits, and well-established clinical infrastructure underpin this dominance. Regular dental visits and active diagnosis of gum conditions drive consistent gel usage. The region’s mature regulatory environment further supports stable product availability and healthcare provider trust.

Asia Pacific is emerging as the highest-growth region, propelled by rising urbanization and expanding middle-class incomes. Increasing prevalence of periodontal disease among urban populations accelerates demand for non-invasive treatments. Private dental clinics are proliferating across key economies including China, India, and South Korea. This infrastructure growth, combined with rising oral health awareness, positions Asia Pacific as the most dynamic opportunity region through 2034.

Recent Developments

- October 2025 — Phibro Animal Health Corporation launched Restoris™, a piezoelectric dental gel designed to treat periodontal disease in dogs by stimulating bone growth and reducing pocket depth.

- January 2025 — Orocidin A/S, a subsidiary of Nordicus Partners Corporation, introduced a novel dental gel for long-term periodontitis treatment featuring a bioadhesive matrix with sustained release of active peptides in periodontal pockets.

- July 2024 — Oral Biolife announced a strategic partnership with Phibro Animal Health to co-develop the Ambrilux Dental Gel, targeting periodontal disease treatment in companion animals through innovative dental formulations.

Conclusion

The global periodontitis gels market is on a steady and well-supported growth path through 2034. Rising disease prevalence, an aging global population, and growing clinical preference for minimally invasive therapies all reinforce sustained demand. Technological improvements in drug delivery further strengthen the market’s long-term growth fundamentals across both developed and emerging regions.

Antibiotic gels and degradable formulations dominate their respective segments, reflecting strong clinical and patient-centric preferences. Hospitals lead application-based demand, while North America maintains regional market leadership with USD 46.7 Million in revenues. Asia Pacific adds incremental growth momentum as dental infrastructure and awareness levels continue rising across key economies.

Companies that invest in personalized formulations, streamlined regulatory pathways, and digital distribution channels will be best positioned to capture share. Early movers in Asia Pacific and underserved developing markets can unlock substantial untapped revenue. The market is projected to reach USD 214.6 Million by 2034, rewarding strategic participants who act decisively now.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)