Table of Contents

Overview

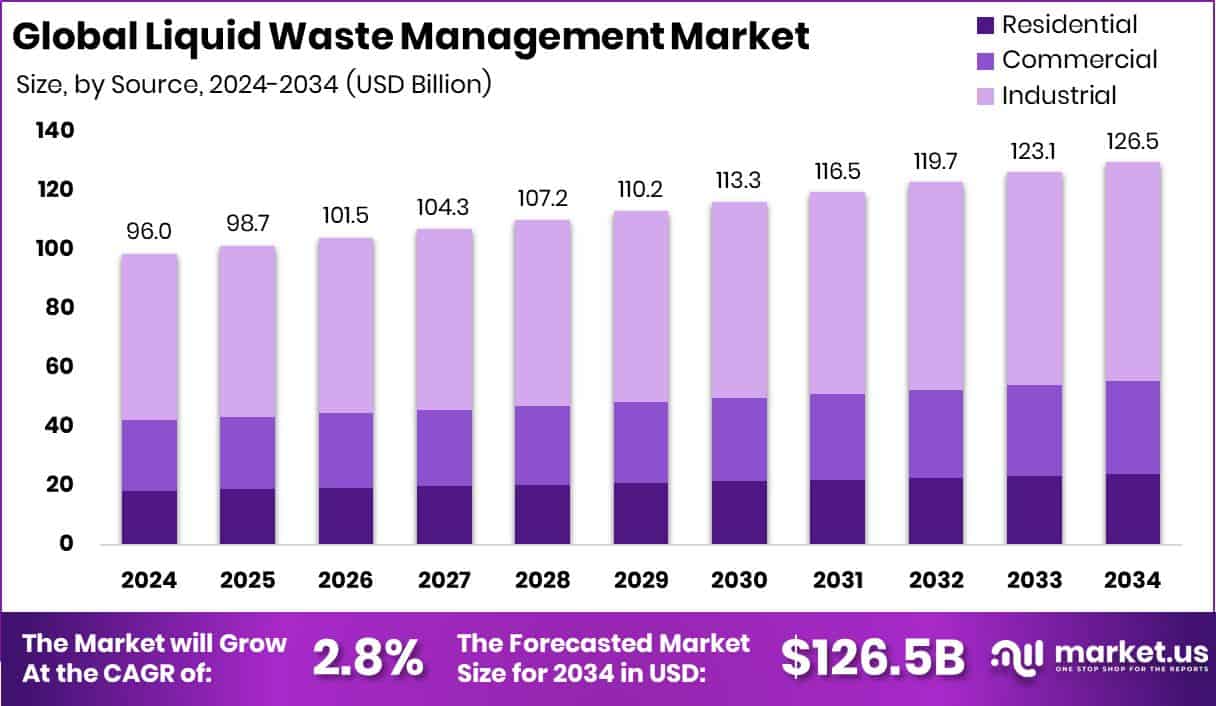

New York, NY – March 30, 2026 – The global liquid waste management sector is on a steady growth path, supported by stronger environmental remediation, public funding, and infrastructure modernization. The market is projected to rise from USD 96.0 billion in 2024 to nearly USD 126.5 billion by 2034, advancing at a 2.8% CAGR, with North America accounting for 41.20% or USD 39.5 billion in 2024.

The sector focuses on the collection, transport, treatment, recycling, and safe disposal of wastewater, sludge, oils, effluents, and other contaminated liquids from residential, industrial, agricultural, and commercial sources. These systems are essential for pollution prevention, water reuse, ecosystem restoration, and regulatory compliance.

Growth momentum is closely tied to major cleanup and restoration programs. The Sovjak rehabilitation project, involving the removal of 40,000 tons of liquid waste and soft tar, reflects increasing legacy-site remediation efforts. Additional environmental recovery support includes USD 40 million secured for restoration across three states and USD 4 million allocated for abandoned industrial site cleanup in Northeast Ohio. Infrastructure expansion is further strengthened by North Carolina’s USD 25 million in grants and a USD 1.34 million grant for a new recycling plant opening in 2024. A USD 5.6 billion environmental services business sale is also creating reinvestment opportunities and resilience.

➤ Click the sample report link for complete industry insights: https://market.us/report/liquid-waste-management-market/request-sample/

Key Takeaways

- The Global Liquid Waste Management Market is expected to be worth around USD 126.5 billion by 2034, up from USD 96.0 billion in 2024, and is projected to grow at a CAGR of 2.8% from 2025 to 2034.

- The liquid waste management market grows rapidly as non-hazardous liquid waste reaches a 65.2% share.

- Industrial activities dominate the liquid waste management market, contributing a strong 58.8% to global demand.

- Collection services lead the Liquid Waste Management Market, holding a considerable 39.5% market share worldwide.

- Physical treatment methods remain essential in the liquid waste management market, accounting for 38.1% overall usage.

- The chemical industry drives expansion of the liquid waste management market, representing 19.4% of the end-user share.

- North America dominated liquid waste management at 41.20%, reaching USD 39.5 Bn in 2024.

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=174969

Market Segments

By Waste Type:

Non-hazardous liquid waste dominated with a 65.2% share in 2024, driven by rising municipal wastewater, low-toxicity industrial effluents, and expanding residential infrastructure. Urbanisation and stricter discharge regulations pushed utilities and industries toward formal treatment systems. Easier handling, lower risk, and wider applicability across domestic and industrial streams strengthened this segment’s leadership, making it the largest contributor in the liquid waste management market.

By Source:

Industrial sources led the market with a 58.8% share, making them the dominant waste generation segment in 2024. High wastewater discharge from chemicals, textiles, pharmaceuticals, food processing, and oil & gas sectors supported this leadership. Growing manufacturing output, plant expansions, and stricter zero-liquid-discharge requirements encouraged industries to invest in specialised treatment systems and outsourcing partnerships, reinforcing industrial dominance across collection, recycling, and reuse activities.

By Service:

Collection services dominated with a 39.5% share in 2024, highlighting their critical role as the first step in liquid waste management. Safe pickup and transport of domestic and industrial wastewater remained essential for preventing contamination and ensuring regulatory compliance. Expansion of tanker fleets, pipeline systems, and scheduled pickup services by municipalities and private operators supported rising waste volumes, especially in dense urban zones and industrial clusters.

By Treatment Method:

Physical treatment methods held the dominant 38.1% share, making them the most widely used treatment approach in 2024. Processes such as filtration, sedimentation, flotation, and screening remained essential for removing suspended solids, oils, and debris before advanced treatment stages. Their affordability, scalability, and compatibility with municipal and industrial plants, alongside growing membrane filtration adoption, helped this segment maintain its leading market position.

By End User:

The chemical industry dominated the end-user segment with a 19.4% share in 2024, supported by large volumes of complex effluents requiring specialised treatment. Waste streams containing solvents, acids, and organic residues increased demand for advanced purification and recycling systems. Rising chemical production capacity, tighter discharge monitoring, and stronger adoption of water-reuse practices further reinforced the industry’s leading role in the liquid waste management landscape.

Regional Analysis

In 2024, North America dominated the liquid waste management market with a 41.20% share, valued at USD 39.5 billion, supported by strong industrial wastewater output and advanced municipal treatment systems. Europe followed with stable growth driven by strict environmental regulations and wastewater reuse initiatives. Asia Pacific saw rising demand due to rapid industrialisation and dense urban populations.

Meanwhile, the Middle East & Africa and Latin America showed steady progress through expanding industrial zones, stronger municipal systems, and increased investments in structured wastewater collection and treatment capacity.

Top Use Cases

- Industrial Wastewater Treatment: Factories such as chemical, textile, food, and oil plants create dirty water with chemicals, solids, and metals. Liquid waste systems clean this water before discharge or reuse, helping industries meet pollution laws and protect rivers. The EPA highlights this as one of the most important uses in industrial environmental protection.

- Municipal Sewage and City Wastewater: Cities use liquid waste management to treat sewage from homes, offices, hotels, and public buildings. It removes harmful bacteria, sludge, and suspended waste before water is safely released or reused for gardening and cleaning. This is essential for public health and cleaner urban water systems.

- Oil and Grease Removal: Refineries, workshops, food plants, and transport hubs produce oily wastewater. Liquid waste management separates oil, grease, and sludge using oil-water separators, flotation, and filtration systems. Recovered oil can often be reused as fuel, reducing waste and disposal costs.

- Groundwater and Soil Pollution Cleanup: Old industrial sites, chemical dumping zones, and contaminated lagoons generate harmful liquid waste that can leak into soil and groundwater. Treatment systems remove toxic liquids, sludge, and leachate to stop long-term environmental damage and support land restoration projects.

- Water Recycling and Reuse: Many industries and cities now treat liquid waste so it can be reused for cooling, washing, irrigation, and process water. This reduces freshwater use and supports sustainable operations, especially in water-stressed regions.

- Hazardous Chemical and Pharma Effluent Treatment: Pharmaceutical, laboratory, and specialty chemical plants generate toxic liquid waste containing solvents, acids, and residues. Special treatment methods such as neutralization, oxidation, and membrane filtration are used to make this waste safe.

Notable Company Developments

- In February 2024, Clean Harbors announced the acquisition of HEPACO for USD 400 million. HEPACO is known for environmental field services and emergency response work. This deal expanded Clean Harbors’ network for liquid waste cleanup, spill response, and contaminated wastewater handling, especially across the eastern United States. It strengthened the response for industrial liquid waste incidents and remediation projects.

- In June 2024, Befesa acquired full ownership of its French Recytech joint venture. This development strengthens its recycling network in Europe and improves its ability to process hazardous industrial residues more efficiently. The move supports wider waste treatment capacity and helps Befesa expand circular recycling services across the region.

- In January 2024, Bion received a new patent expansion for its ARS technology, extending use beyond livestock waste into industrial and municipal wastewater streams. This is an important technology development because it broadens Bion’s reach into city sewage and factory wastewater applications.

Conclusion

The liquid waste management market is growing steadily as industries, cities, and governments focus more on safe wastewater treatment, recycling, and environmental protection. Rising industrial discharge, urban sewage volumes, and stricter pollution rules continue to increase demand for collection, treatment, and reuse services. Growth is further supported by infrastructure upgrades, remediation projects, and investments in advanced technologies such as filtration, nutrient recovery, and waste-to-resource systems.

Strong progress in North America, Europe, and Asia Pacific highlights global expansion opportunities. As sustainability and water reuse become priorities, the market will remain essential for protecting ecosystems, public health, regulatory compliance, and long-term resource efficiency worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)