Table of Contents

Lactulose Market Overview

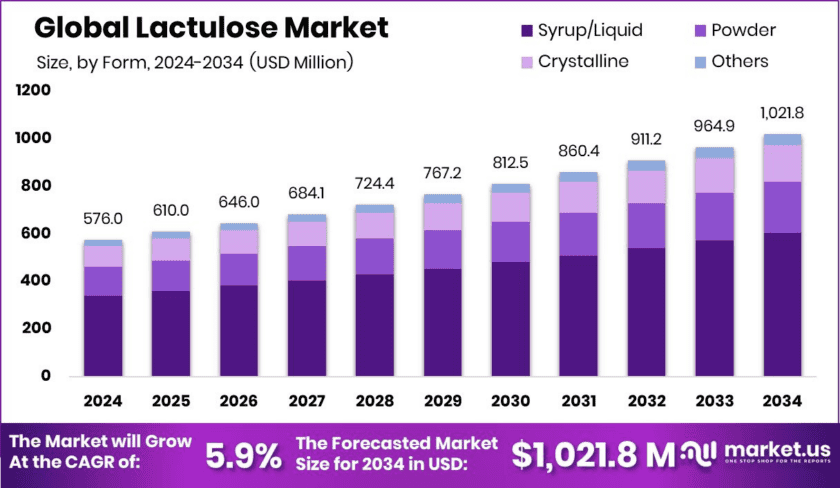

The Lactulose Market is set for steady expansion as global digestive and liver care needs rise. Industry demand is projected to reach USD 1,021.8 million by 2034 from USD 576.0 million in 2024, reflecting a 5.9% CAGR. Consequently, manufacturers are increasing production and healthcare partnerships to meet broader therapeutic demand.

Lactulose therapies support chronic constipation treatment and hepatic encephalopathy management across hospitals and retail channels. Moreover, physicians favor this synthetic sugar because it safely reduces ammonia absorption and improves bowel movement consistency. This clinical reliability strengthens prescription rates across aging populations and liver disease patient groups worldwide.

Healthcare systems increasingly recommend lactulose as a first-line solution for long-term constipation relief. Additionally, liver specialists use it widely in cirrhosis-linked cognitive complications. This dual therapeutic role improves product resilience because demand comes from both routine digestive care and high-value hospital-based liver treatment protocols.

Patient-friendly formulations further support growth, especially syrup and liquid variants. However, affordability gaps remain in some developing regions where repeated use raises therapy costs. Even so, healthcare access improvements and broader reimbursement policies are expected to sustain future market momentum.

Key Takeaways

- The Global Lactulose Market will reach USD 1,021.8 million by 2034 from USD 576.0 million in 2024, growing at 5.9% CAGR.

- Syrup and liquid formulations lead with 59.2% share due to easy dosing and stronger compliance.

- Laxative use dominates functional demand with 49.1%, reflecting rising constipation treatment needs.

- Pharmaceutical applications hold 56.9% share, confirming healthcare as the core revenue engine.

- Asia Pacific generated USD 263.8 million and captured 45.8% global share.

➤ Download Exclusive Sample Of This Premium Report (Including Full TOC, Table & Figures)- https://market.us/report/global-lactulose-market/request-sample/

Market Segmentation Overview

Syrup and liquid lactulose dominate the form segment with 59.2% share. Healthcare providers prefer these oral formats because they simplify dosing for children and older adults. Consequently, hospitals and home-care settings continue increasing usage where fast administration and flexible intake volumes matter most.

Laxative applications contribute 49.1% of functional demand, driven by chronic constipation cases linked to sedentary lifestyles and aging. Additionally, pharmaceutical use leads with 56.9% share because lactulose remains central in digestive and hepatic care guidelines. This combination makes healthcare applications the strongest growth pillar.

Drivers

Digestive disorders remain the strongest market driver. Chronic constipation cases are increasing due to poor diet, stress, low physical activity, and aging demographics. Therefore, physicians continue prescribing lactulose as a safe long-term bowel regulator, supporting repeat demand through clinics, pharmacies, and elderly care channels.

Liver disease incidence also accelerates market expansion. Alcohol consumption, obesity, and viral infections are raising cirrhosis and hepatic encephalopathy cases globally. Consequently, hospitals rely on lactulose to lower ammonia toxicity, which directly improves neurological outcomes and increases its use in emergency and inpatient care.

Use Cases

Constipation management remains the most established use case across adult and geriatric patients. Liquid lactulose softens stools by drawing water into the colon, enabling gentle relief without dependency risks. Moreover, this benefit improves physician trust for long-duration treatment plans in recurring digestive disorders.

Hepatic encephalopathy treatment represents a high-value clinical use case. Lactulose reduces gut ammonia absorption and supports toxin removal in patients with severe liver dysfunction. Therefore, liver specialists use it to improve cognition, reduce hospital readmissions, and enhance the quality of life for chronic liver disease patients.

Major Challenges

Treatment affordability remains a major barrier in low- and middle-income economies. Repeated use increases cumulative therapy costs, which discourages adherence among cost-sensitive patients. However, this challenge also signals unmet demand that generic suppliers and public health reimbursement models can address.

Limited insurance coverage creates another adoption hurdle. Many healthcare systems prioritize acute therapies over digestive maintenance products, reducing patient access. Consequently, some consumers shift toward cheaper alternatives, slowing premium pharmaceutical lactulose penetration despite its strong long-term safety profile.

Business Opportunities

Liver disease treatment expansion offers a major revenue opportunity for pharmaceutical manufacturers. Hospital admissions for cirrhosis complications continue rising globally, increasing demand for ammonia-lowering therapies. Therefore, companies that strengthen hepatology distribution and specialist partnerships can unlock faster prescription-led growth.

Functional nutrition and gut-health innovation also create new pathways. Companies can extend lactulose into food, beverage, and clinical nutrition applications where prebiotic benefits support digestive wellness. Additionally, this diversification reduces dependence on prescription channels and expands recurring consumer health revenue streams.

Regional Analysis

Asia Pacific leads the Lactulose Market with 45.8% share and USD 263.8 million revenue in 2024. China, India, and Japan drive this growth through larger patient pools, expanding healthcare infrastructure, and rising digestive care awareness. Consequently, the region remains the strongest long-term volume opportunity.

North America and Europe maintain strong positions through advanced healthcare systems and broader diagnosis rates for constipation and liver disease. Meanwhile, Latin America and the Middle East are gradually improving access through pharmacy expansion and hospital modernization, creating emerging growth clusters beyond mature markets.

Top Key Players in the Market

- Fresenius Kabi

- Orion Lifescience

- Morinaga Milk Industry Co., Ltd.

- Illovo

- Biofac

- Daiichi Sankyo

- Inalco SpA

- Casca Remedies

- Enrich Pharma

Conclusion

The Lactulose Market shows reliable long-term growth supported by digestive health needs, liver disease treatment demand, and strong pharmaceutical adoption. Moreover, liquid formulations, hospital prescribing trends, and Asia Pacific expansion continue to strengthen the competitive landscape for established and emerging suppliers. Future growth will depend on affordability improvements, broader reimbursement, and expansion into liver-focused and gut-health applications.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)