Table of Contents

Market Overview

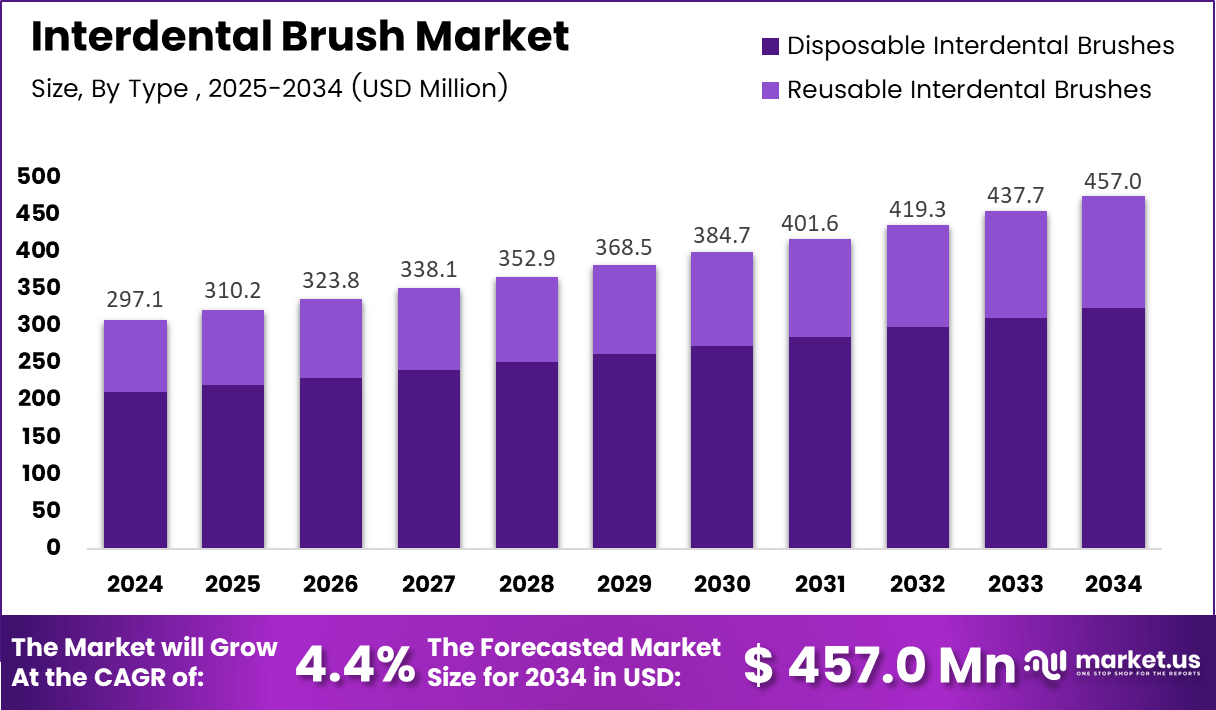

The global interdental brush market is valued at USD 297.1 million in 2024 and is projected to reach USD 457.0 million by 2034. This growth reflects a compound annual growth rate of 4.4% across the forecast period from 2025 to 2034. Rising preventive dental care adoption and expanding clinical recommendations underpin this steady upward trajectory.

Interdental brushes are precision oral hygiene tools engineered to clean the spaces between teeth that standard toothbrushes cannot reach. They come in reusable and disposable formats with varying bristle types, handle designs, and sizing systems for different interdental gaps. Dental professionals recommend them as essential adjuncts for plaque control and gum disease prevention. Consumers across general, orthodontic, and geriatric care segments rely on them daily.

Multiple healthcare and retail sectors actively drive interdental brush adoption worldwide. National oral health programs promote them as frontline tools for early gum disease prevention. Dental clinics prescribe them during routine hygiene visits and post-procedure care. Pharmacies, online platforms, and specialty health retailers collectively ensure broad product accessibility across urban and suburban consumer populations.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Manufacturers are investing in ergonomic innovation to improve comfort, compliance, and sustainability credentials. Silicone-coated wire handles, softer nylon bristles, and wire-free variants address diverse user comfort needs. Biodegradable materials including bamboo handles and bio-nylon bristles respond to growing eco-conscious consumer demand. These product upgrades attract both first-time users and existing buyers trading up to premium interdental care formats.

Government oral health initiatives and evolving regulatory standards actively support market expansion. Agencies establish material quality, sterility, and device safety guidelines that raise consumer trust in category products. Public campaigns targeting early gum disease prevention expand product visibility in markets where interdental cleaning remains underutilized. Consequently, regulatory compliance becomes a competitive differentiator for manufacturers serving clinical and retail channels.

Clinical research confirms the measurable impact driving this market’s commercial case. Studies show interdental brush users experienced significantly reduced plaque levels with an odds ratio of 0.73 and lower gum bleeding with an odds ratio of 0.69. Among orthodontic patients with fixed appliances, 58% used interdental brushes regularly, with 72.4% reporting daily usage. These compliance figures validate strong habitual demand and long-term repeat purchase potential.

Key Takeaways

- The global interdental brush market will grow from USD 297.1 million in 2024 to USD 457.0 million by 2034, at a 4.4% CAGR.

- Reusable Interdental Brushes dominated the type segment with 71.2% share in 2024, driven by cost efficiency and sustainability preferences.

- Nylon Bristles led the bristle segment with 77.8% share in 2024, reflecting superior flexibility and strong dental professional endorsement.

- Wire Handles accounted for 61.3% of the handle segment in 2024, valued for bendability and precision access.

- Pharmacies and Drug Stores held the largest distribution channel share at 36.9% in 2024.

- North America led all regions with 45.8% market share, valued at USD 136.0 million in 2024.

- Among orthodontic patients with fixed appliances, 58% used interdental brushes regularly, with 72.4% reporting daily usage.

Market Segmentation Overview

Reusable Interdental Brushes command 71.2% of the type segment in 2024. Consumers choose reusable formats for their lower long-term cost and reduced plastic waste compared to single-use alternatives. Rising sustainability awareness reinforces this preference across demographic groups. Consequently, manufacturers prioritize durable, recyclable designs that meet both hygiene standards and eco-conscious purchasing expectations.

Disposable Interdental Brushes serve users who value travel convenience and ease of use during orthodontic treatment. Manufacturers have expanded single-use lines with slender profiles and softer bristles targeting sensitive gum users. Their inclusion in travel-sized oral care kits supports casual adoption among consumers new to interdental cleaning routines. Additionally, disposables serve short-term clinical post-procedure needs where sterility is a priority.

Nylon Bristles dominate the bristle segment with 77.8% share due to their flexibility, cleaning efficiency, and broad compatibility across brush sizes. Dental professionals frequently recommend nylon-based options, accelerating consumer trust and category-wide adoption. Plastic Bristles retain relevance for users requiring firmer texture and longer durability when cleaning wider interdental gaps. Ongoing tip refinement and shaping improvements continue to expand plastic bristle usability.

Wire Handles lead the handle segment at 61.3%, prized for their bendability and ability to navigate complex interdental angles, particularly around orthodontic brackets. Dental practitioners routinely endorse wire-handled brushes for precision plaque control in difficult-to-reach spaces. Plastic Handles attract users who prefer lightweight ergonomic tools with reduced gum irritation risk. Textured grip designs and compact travel formats have broadened plastic handle acceptance across all age groups.

Pharmacies and Drug Stores hold the largest distribution share at 36.9%, driven by consumer reliance on pharmacist guidance and consistent in-store brand availability. Dental clinics serve patients seeking professional-grade solutions for complex conditions. Online sales channels are growing rapidly, supported by easy product comparison, home delivery, and subscription-based replenishment services. Together, these channels ensure comprehensive consumer reach across clinical, retail, and digital touchpoints.

Drivers

Growing clinical integration of interdental brushes into national oral-health guidelines directly strengthens market demand. Dental associations across key markets now classify these tools as essential rather than optional components of daily gum-care routines. Professional recommendations during hygiene visits build consumer confidence and drive consistent repeat purchases. This clinical validation accelerates adoption among patients managing braces, gum disease, and early-stage periodontal conditions.

The expanding global geriatric population creates a structurally growing customer base for interdental brushes. Older adults experience wider interdental spacing and heightened periodontal risk, making precision cleaning tools a practical daily necessity. Demographic aging in North America, Europe, and Asia Pacific reinforces long-term demand consistency. Manufacturers respond by developing brushes with softer bristles and ergonomic handles specifically engineered for sensitive and aging gum tissue.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Use Cases

Orthodontic patients with fixed braces or retainers represent one of the most consistent and high-frequency use cases in the market. Standard toothbrushes cannot effectively clean around brackets and wires, making interdental brushes an essential daily tool. Research confirms that 58% of patients with fixed appliances use them regularly, with 72.4% doing so daily. This captive user base generates reliable repeat purchasing and long-term category loyalty.

Additionally, older adults managing gum sensitivity and food retention between teeth rely on interdental brushes as part of their daily oral hygiene protocols. Wider interdental gaps common in geriatric patients require specialized cleaning tools that standard floss cannot navigate comfortably. Interdental brushes provide effective, gentle plaque removal without the dexterity demands of traditional flossing. Therefore, this application supports both preventive gum health and post-treatment maintenance across aging patient populations.

Major Challenges

Limited consumer awareness in rural and developing regions remains a significant barrier to market growth. Many individuals rely exclusively on standard toothbrushing due to lack of dental education or limited access to professional consultations. This knowledge gap is particularly pronounced in low-income markets where preventive oral care behaviors are still emerging. Expanding community-level dental education programs is essential to unlock adoption potential in these underserved geographies.

However, the higher long-term cost of interdental brushes compared to conventional floss deters price-sensitive consumers in cost-conscious segments. Regular brush replacement increases cumulative spending, creating a perceived affordability barrier over time. Consumers in regions with limited disposable income often default to lower-priced floss alternatives despite clinically inferior plaque control outcomes. Therefore, value-positioning strategies and accessible entry-level product tiers remain critical for broader market penetration.

Business Opportunities

Rapid product premiumization through ergonomic design upgrades presents strong near-term revenue opportunity. Silicone-coated wire handles, advanced grip texturing, and color-coded sizing systems enhance both usability and user confidence. Consumers increasingly pay premium prices for tools that combine comfort, durability, and guided sizing clarity. Manufacturers investing in these upgrades can capture higher margins while reducing the sizing-related discomfort that currently discourages repeat usage.

Moreover, pharmacy retail partnerships and online subscription models offer scalable recurring revenue pathways. Auto-replenishment services simplify reordering for high-frequency users, increasing customer lifetime value and reducing churn. E-commerce platforms facilitate educational content delivery alongside purchase, improving consumer knowledge and compliance. Consequently, brands that embed interdental brushes into subscription-based oral wellness bundles can secure predictable long-term demand streams.

Regional Analysis

North America leads the global interdental brush market with 45.8% share and revenues of USD 136.0 million in 2024. High dental visit frequency, strong consumer awareness of gum disease risks, and active promotion of preventive oral hygiene protocols drive regional dominance. Consumer preference for reusable and eco-friendly formats aligns well with leading product innovations. The US market in particular benefits from robust pharmacy retail networks and direct dental professional recommendations.

Asia Pacific is emerging as the fastest-growing regional market, propelled by rising urbanization and expanding middle-class spending on oral hygiene. Increasing orthodontic treatment volumes across China, Japan, and South Korea generate a growing patient base requiring precision interdental cleaning tools. Shifting consumer preferences toward cost-effective and reusable oral care solutions further support category growth. Additionally, improving dental awareness in emerging economies positions Asia Pacific as the most dynamic expansion opportunity through 2034.

Recent Developments

- April 2025 — DD Group announced the acquisition of Eli Dent, a leading dental consumables supplier headquartered in Borgo San Lorenzo, Tuscany. Eli Dent serves more than 7,000 dental customers across Italy, supplying dental brands, pharmaceutical products, and small equipment, strengthening DD Group’s presence in the Italian dental market.

Conclusion

The global interdental brush market is on a steady and well-supported growth path, driven by clinical endorsement, aging demographics, and expanding preventive dental care culture. A 4.4% CAGR through 2034 reflects durable structural demand rather than short-term trend activity. Rising orthodontic treatment volumes and growing gum disease awareness across key markets reinforce long-term revenue foundations.

Reusable brushes, nylon bristles, and wire handles dominate their respective segments, reflecting strong alignment between clinical recommendations and consumer product preferences. North America maintains regional market leadership at 45.8% share and USD 136.0 million in revenues. Asia Pacific adds the greatest growth momentum as dental awareness and orthodontic treatment rates accelerate across emerging economies.

Brands that invest in premium ergonomic designs, eco-friendly materials, and subscription-based distribution models will be best positioned to capture long-term market share. Closing the awareness gap in rural and emerging markets through dental education partnerships will unlock substantial untapped demand. The market is projected to reach USD 457.0 million by 2034, rewarding manufacturers and retailers who act on these strategic priorities now.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)