Table of Contents

Introduction

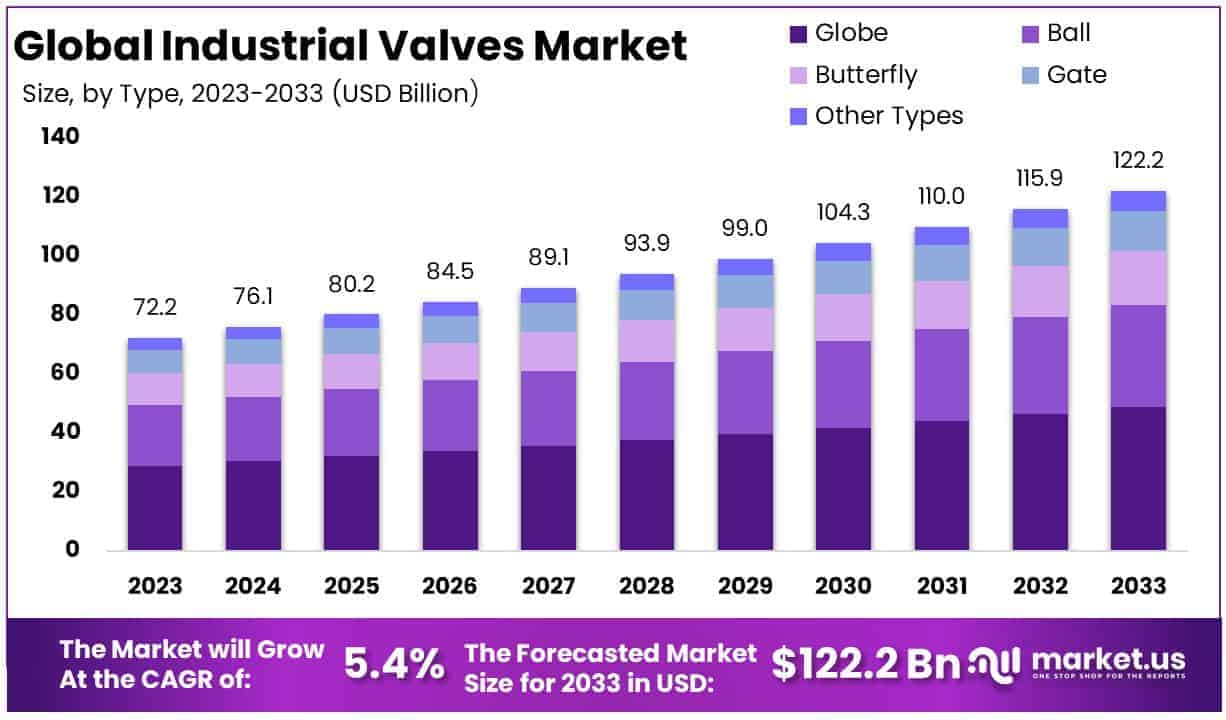

The Global Industrial Valves Market is projected to reach approximately USD 122.2 billion by 2033, up from USD 72.2 billion in 2023, reflecting a compound annual growth rate (CAGR) of 5.40% from 2024 to 2033. In 2023, the Asia Pacific region held the largest market share, accounting for 36% and generating a revenue of USD 25.9 billion within the industrial valves market.

Industrial valves are mechanical devices used to control the flow of fluids, gases, or slurries within pipelines, tanks, and other systems across various industrial applications. These valves play a critical role in regulating pressure, temperature, and fluid flow, ensuring safety and operational efficiency in industries such as oil and gas, chemical processing, water treatment, and power generation. The industrial valves market refers to the global industry that designs, manufactures, and sells these essential components to end-users.

Key growth drivers include rising industrial automation, increasing investments in infrastructure development, and the expanding demand for energy and water management solutions. The ongoing industrialization in emerging economies, coupled with the trend toward sustainable and energy-efficient systems, presents significant opportunities for market expansion. Furthermore, the growing adoption of smart valves and IoT integration to monitor and optimize flow control systems is expected to provide substantial growth potential, creating new avenues for innovation and market development.

Core Findings

- The global industrial valves market is projected to reach approximately USD 122.2 billion by 2033, growing from USD 72.2 billion in 2023, with a compound annual growth rate (CAGR) of 5.40% during the forecast period from 2024 to 2033.

- In 2023, the globe valve type led the market, accounting for a 40% share in the industrial valves segment.

- Steel was the dominant material in the industrial valves market in 2023, holding a 35% share.

- The oil and power sectors together commanded a dominant 43% share of the industrial valves market in 2023, reflecting their significant demand for these components.

- The Asia Pacific region accounted for 36% of the global industrial valves market in 2023, generating USD 25.9 billion in revenue.

Emerging Trends

- Automation Integration: The industrial valve market is increasingly influenced by automation technologies, especially with the rise of smart valves. These valves are equipped with sensors and actuators, enabling real-time monitoring, diagnostics, and remote control. This trend has been driven by the need for increased operational efficiency and predictive maintenance in industries such as oil & gas, water treatment, and manufacturing.

- Focus on Energy Efficiency: With a growing emphasis on sustainability, the demand for energy-efficient industrial valves has surged. Manufacturers are designing valves that minimize energy losses by reducing friction and optimizing flow control, contributing to energy savings in processes such as heating, cooling, and fluid transport. This aligns with global efforts to reduce carbon footprints and operational costs.

- Use of Advanced Materials: There is a notable shift toward the use of advanced materials in valve manufacturing, including high-performance alloys, composites, and corrosion-resistant coatings. These materials extend the lifespan of valves, particularly in harsh environments like chemical plants and offshore oil rigs, where durability is crucial. The demand for such materials has grown in response to the need for more robust and reliable equipment.

- Increased Demand for Cryogenic Valves: Cryogenic valves, designed to handle extremely low temperatures, are becoming increasingly important, particularly in industries such as liquefied natural gas (LNG) production and transportation. As global demand for LNG continues to rise, so does the demand for specialized valves capable of maintaining the integrity of gas storage and transport at cryogenic temperatures.

- 3D Printing Technology: The application of 3D printing in industrial valve manufacturing is gaining traction. This technology allows for the production of custom-designed valves with complex geometries and enhanced performance features. By enabling rapid prototyping and reducing lead times, 3D printing offers significant advantages, particularly in industries where specialized valve designs are required for unique operational needs.

Top Use Cases

- Oil & Gas Industry: Industrial valves are critical in the oil and gas sector, particularly for controlling the flow of crude oil, natural gas, and other liquids. In upstream operations, valves are used in drilling operations, while in downstream operations, they play a key role in refining processes. The global oil and gas industry consumes a significant proportion of industrial valves, with safety and reliability being paramount in preventing hazardous leaks and explosions.

- Water and Wastewater Treatment: Valves in water and wastewater treatment plants control the flow of water and chemicals used in the purification process. The efficient regulation of water flow ensures that treatment systems operate optimally, while valves help manage pressure levels, chemical dosing, and the release of treated water into rivers or other bodies. The need for water conservation and efficient resource management is driving the demand for specialized valves in this sector.

- Power Generation: In the power generation industry, industrial valves regulate the flow of steam, gas, and water in power plants. Whether in coal, nuclear, or renewable energy plants, valves are essential for controlling temperature, pressure, and fluid dynamics within turbines and reactors. The rise of renewable energy sources such as geothermal and solar thermal has also increased demand for valves that can operate efficiently in these specialized environments.

- Chemical Processing: Valves are heavily utilized in chemical manufacturing to control the flow of raw materials, chemicals, and gases within production lines. Industrial valves need to withstand aggressive chemicals and extreme temperatures. This sector also requires valves that can provide precise control to ensure safe reactions, preventing overpressure situations and chemical spills that could harm the environment or production process.

- Food and Beverage Industry: In the food and beverage sector, valves are crucial for controlling the flow of liquids, gases, and solids during production and packaging processes. They are often designed to meet strict sanitary standards to avoid contamination. The increasing trend toward automation in this industry has spurred the demand for more sophisticated, hygienic, and easy-to-maintain valve solutions that can handle food-grade materials and ensure compliance with safety regulations.

Major Challenges

- Regulatory Compliance: Compliance with stringent regulations and standards is one of the biggest challenges facing the industrial valve market. Different industries, such as pharmaceuticals, chemicals, and food processing, are subject to strict regulations on valve materials, safety, and operation. Non-compliance can result in costly penalties, product recalls, and safety hazards. Manufacturers must continually update valve designs to meet evolving industry standards and certifications.

- High Maintenance and Downtime Costs: In critical industries such as oil & gas and power generation, the failure of valves can result in significant downtime and maintenance costs. These industries often deal with harsh operating conditions, including high pressures and temperatures, which can accelerate wear and tear. The maintenance of valves in these environments can be expensive and time-consuming, leading to lost productivity and increased operational costs.

- Material and Supply Chain Issues: The industrial valve industry is highly reliant on specialized materials, such as corrosion-resistant alloys and high-strength steels, which can be expensive and subject to supply chain fluctuations. In recent years, disruptions in global supply chains have led to material shortages and delays in production. This has affected the ability of manufacturers to meet demand for valves, especially those with advanced material requirements for demanding applications.

- Adoption of New Technologies: The integration of advanced technologies such as IoT and AI in industrial valves requires significant investment and expertise. Many manufacturers face challenges in adopting these innovations due to the high costs of R&D and the need for skilled labor to implement and maintain these systems. Additionally, there can be resistance from traditional industries where operators are accustomed to legacy systems, creating barriers to technological upgrades.

- Environmental and Sustainability Pressures: As industries face increasing pressure to reduce their environmental impact, there is a growing demand for more sustainable valve solutions. Manufacturers must invest in the development of eco-friendly materials and energy-efficient valve designs. However, the balancing of performance, durability, and environmental sustainability remains a challenge, particularly in industries that require heavy-duty valves capable of withstanding harsh operating conditions.

Top Opportunities

- Expansion in Emerging Markets: There is substantial growth potential for industrial valves in emerging markets, particularly in Asia-Pacific, Latin America, and parts of Africa. Rapid industrialization, increasing urbanization, and infrastructural developments in these regions are creating new demand for valves in sectors such as oil & gas, water treatment, and manufacturing. Local demand for energy-efficient and cost-effective valve solutions is driving market opportunities.

- Increase in Renewable Energy Projects: The global shift towards renewable energy presents significant growth opportunities for industrial valves, especially in wind, solar, and geothermal power plants. Valves are essential in the regulation of fluids and gases used in energy production. As governments and corporations increasingly focus on reducing carbon emissions, there is a growing demand for valves that support sustainable energy generation, creating a new niche within the valve market.

- Digitalization and Smart Valves: The trend toward digitalization is opening up new opportunities for smart valves that offer remote monitoring, data analytics, and predictive maintenance capabilities. As industries seek to optimize operations and reduce downtime, smart valve solutions are increasingly being adopted. Manufacturers who can provide valves with built-in IoT capabilities and real-time performance tracking will be well-positioned to capitalize on this growing demand.

- Water Management and Conservation: Water scarcity issues are driving the adoption of advanced valve solutions for water management and conservation. As governments and industries focus on efficient water usage and wastewater treatment, valves that provide precise flow control, reduce leakage, and minimize water wastage are in high demand. Companies offering innovative solutions for managing water systems in agriculture, municipalities, and industrial plants stand to benefit from this growing market.

- Customization and 3D Printing: The rise of 3D printing offers an exciting growth opportunity in the industrial valve market. The technology enables manufacturers to produce highly customized valves with unique geometries, optimized for specific operational needs. This approach allows for faster production times and greater flexibility in valve design, opening up opportunities to meet niche market demands and cater to industries requiring specialized solutions.

Key Player Analysis

- AVK Holding: AVK Holding is a leading manufacturer of valves, hydrants, and fittings, catering to the water, wastewater, and industrial sectors. The company has a strong global presence, with a focus on high-quality products and reliable solutions. The company’s ability to offer tailored valve solutions for critical applications has contributed significantly to its market position. AVK’s robust distribution network and commitment to innovation have enabled it to expand its footprint across multiple industries.

- Avcon Controls Pvt. Ltd: Avcon Controls Pvt. Ltd, based in India, specializes in manufacturing industrial valves for diverse sectors including chemicals, oil & gas, and power plants. The company’s products are known for their durability and performance in harsh environments.The company’s strong R&D capabilities and cost-effective production techniques have helped it secure a solid position in both the domestic and international markets.

- Schlumberger Limited: Schlumberger is one of the largest providers of oilfield services and industrial valves. The company offers a wide range of valves used in the oil & gas and petrochemical sectors. Its extensive product portfolio includes valves that meet stringent industry standards, which has enabled the company to build a strong reputation for reliability in critical infrastructure applications. Schlumberger’s focus on technological advancements and its global service network continues to drive its success.

- Crane Co.: Crane Co. is a diversified manufacturer with a broad portfolio of industrial valves serving industries like aerospace, transportation, and energy. Crane’s valve products are widely used in the chemical, power, and water treatment sectors. The company focuses on innovative valve designs, enhanced by its extensive experience in fluid control systems. Crane’s established presence in both mature and emerging markets contributes to its steady growth.

- Emerson Electric Co.: Emerson Electric Co. is a global technology and engineering company, providing a comprehensive range of industrial valves for various sectors, including oil & gas, power, and chemical industries. The company’s valves are known for their precision and ability to handle complex applications, with a strong focus on automation and IoT integration. Emerson’s extensive global network and commitment to innovation place it among the top players in the industrial valve market.

Regional Analysis

Asia Pacific Leading Region in Industrial Valves Market with Largest Market Share of 36%

The Asia Pacific region is poised to maintain its dominant position in the industrial valves market, holding the largest market share of 36% in 2023, valued at USD 25.9 billion. This substantial share can be attributed to the region’s rapid industrialization, significant infrastructure development, and increasing investments in manufacturing sectors such as oil and gas, power generation, water treatment, and chemical processing. The high demand for industrial valves in Asia Pacific is driven by the region’s extensive industrial activities, particularly in countries like China, India, Japan, and South Korea.

These countries have consistently been the epicenters of industrial growth, contributing to a strong and stable demand for advanced valve technologies, including globe valves, ball valves, and gate valves. Moreover, the growing emphasis on automation and control systems in industrial processes is further fueling the adoption of industrial valves in this region. Asia Pacific’s robust economic growth, along with its expanding manufacturing base and the implementation of large-scale infrastructure projects, ensures the region’s continued leadership in the global industrial valves market.

Recent Developments

- In 2023, Weir, a leader in mining technology, announced the acquisition of SentianAI, a Swedish firm known for its artificial intelligence solutions that enhance mineral processing. This acquisition will allow Weir to speed up its technological advancements and improve its digital capabilities, supporting more efficient and sustainable practices for its customers.

- In 2024, Emerson revealed that its Fisher™ FIELDVUE™ DVC7K Digital Valve Controller received the Product of the Year award from Control Engineering magazine. The DVC7K enhances performance with its innovative features, including real-time data analysis, user-friendly controls, and flexible connectivity, offering better control and efficiency for industrial operations.

- In 2024, Flowserve Corporation completed the acquisition of MOGAS Industries, expanding its portfolio of severe service valves and related services. This move strengthens Flowserve’s position in the critical valve market and broadens its capabilities to serve demanding industrial applications more effectively.

- In 2023, KSB Group introduced the Aporis double-offset butterfly valve, featuring an elastomer sealing element. This new product is specifically designed for large-scale water transport and treatment, providing reliable shutoff performance in high-volume industrial applications such as water systems and cooling circuits.

- In April 2024, Emerson launched the ASCO™ Series 148/149 safety valve and motorized actuator for fuel oil burner systems. This solution is designed to prevent overpressure and leaks, offering industrial users a reliable and versatile option for maintaining safety and efficiency in combustion applications.

Conclusion

The industrial valves market is experiencing significant growth driven by factors such as industrial automation, rising energy demands, and increasing infrastructure investments, particularly in emerging economies. The adoption of advanced technologies like smart valves, automation systems, and energy-efficient designs is reshaping the market landscape, offering substantial opportunities for innovation and market expansion. While challenges such as regulatory compliance, high maintenance costs, and material shortages remain, the ongoing development of specialized valve solutions for critical industries, along with a growing emphasis on sustainability and digitalization, presents a promising future for the sector. The industrial valves market is well-positioned for steady growth, particularly in regions with high industrial activity, where demand for reliable and efficient valve systems continues to rise.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)