Table of Contents

Market Overview

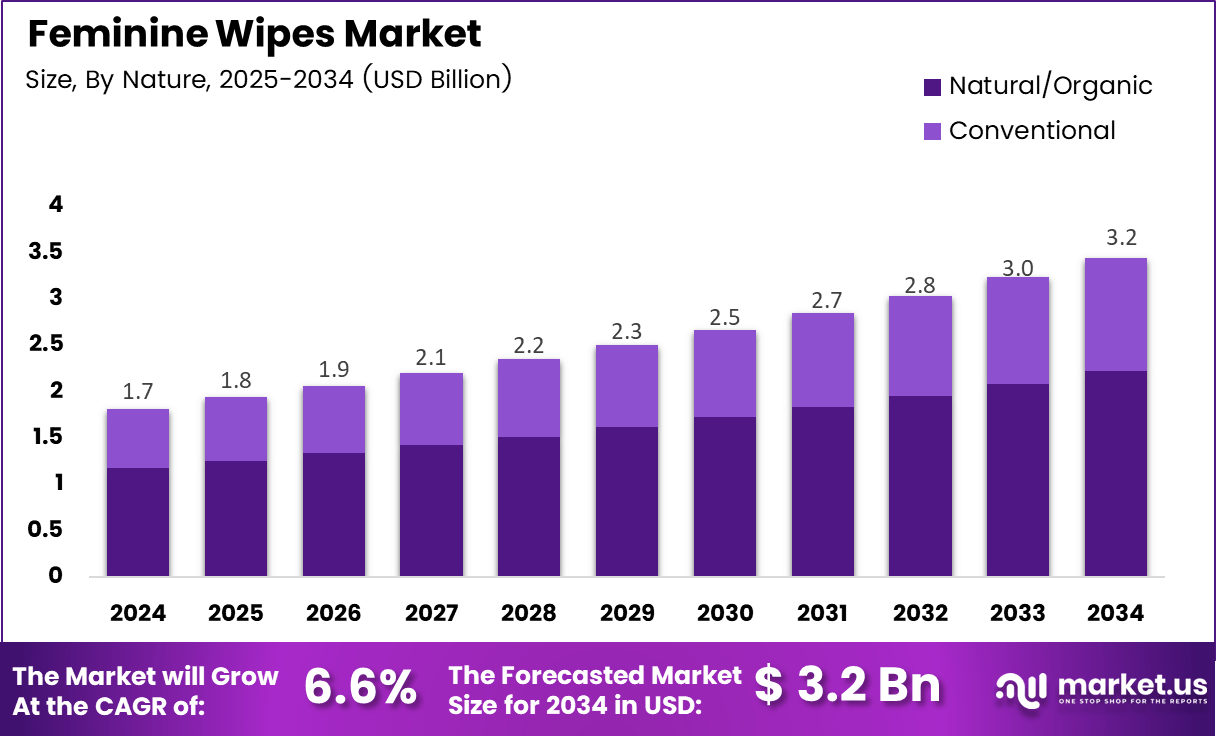

The global feminine wipes market is valued at USD 1.7 billion in 2024 and is projected to reach USD 3.2 billion by 2034. This expansion reflects a compound annual growth rate of 6.6% across the forecast period from 2025 to 2034. Rising intimate hygiene awareness, busy urban lifestyles, and demand for portable personal care solutions drive this sustained growth trajectory.

Feminine wipes are disposable, pre-moistened products designed for external intimate hygiene and daily cleanliness. They support odor control, skin comfort, and convenient personal care across a wide range of daily situations. Formulations typically include pH-balancing agents, soothing extracts, and skin-safe preservatives tailored for sensitive intimate skin. Both conventional and natural variants serve distinct consumer preferences across retail and digital channels.

Several sectors drive adoption of feminine wipes across diverse consumer demographics and geographies. Working women rely on them as portable on-the-go hygiene tools compatible with professional and travel schedules. Healthcare providers recommend them for hygiene maintenance during menstruation, pregnancy, and post-partum recovery. Organized retail, pharmacy chains, and e-commerce platforms collectively ensure broad product visibility across both urban and emerging markets.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Product innovation is reshaping competitive dynamics through material science and ingredient transparency. Manufacturers now engineer wipes using bamboo fiber, bio-nylon, and plant-based formulations that combine biodegradability with skin compatibility. Probiotic and prebiotic ingredients are entering product formulations to actively support healthy vaginal flora. These advances help brands differentiate on functional wellness credentials beyond basic cleansing performance.

Regulatory frameworks in major markets actively govern ingredient safety, microbiome protection, and cosmetic claim accuracy. Authorities scrutinize antibacterial, pH-balancing, and therapeutic product claims to protect consumer safety. This oversight encourages manufacturers to invest in ethical certifications including cruelty-free and vegan status that reinforce premium brand positioning. Compliance with these standards builds consumer trust while enabling sustainable premiumization across the category.

Consumer demand for clean formulations is supported by measurable ingredient transparency commitments from leading manufacturers. Products formulated without parabens or alcohol and carrying PETA-certified vegan and cruelty-free status represent the fastest-growing product tier. Maintaining a pH balance of 3.5 with lactic acid aligns with recommended intimate hygiene practices endorsed by gynecologists. These formulation credentials directly address the safety concerns that currently restrain broader category adoption.

Key Takeaways

- The global feminine wipes market will grow from USD 1.7 billion in 2024 to USD 3.2 billion by 2034, at a 6.6% CAGR.

- Synthetic wipes lead the material fabric segment with 44.8% share, supported by consistent texture, mass-production compatibility, and competitive pricing.

- Conventional feminine wipes dominate the nature segment with 69.1% share due to widespread availability and established consumer familiarity.

- General Wipes account for 61.2% of the application segment, driven by everyday freshness, travel use, and multi-lifestyle versatility.

- Supermarkets and Hypermarkets lead distribution with 39.9% share, benefiting from high product visibility and impulse-purchase dynamics.

- Asia Pacific dominates all regions with 46.8% market share, valued at USD 0.7 billion in 2024.

- Key growth trends include fragrance-free formulations, biodegradable materials, and probiotic-infused products targeting microbiome-conscious consumers.

Market Segmentation Overview

Synthetic wipes lead the material fabric segment with 44.8% share in 2024. Manufacturers prefer synthetic fabrics for their uniform absorbency, longer shelf stability, and compatibility with high-volume production and competitive retail pricing. Cotton-based wipes address sensitive skin users seeking gentler textures but face adoption limits due to higher cost and lower durability. Biodegradable materials represent a fast-growing premium niche as sustainability regulations and eco-conscious purchasing behaviors intensify.

Conventional feminine wipes hold 69.1% of the nature segment, backed by established supply chains, broad consumer recognition, and strong affordability across mass retail formats. Natural and organic wipes gain momentum among consumers transitioning toward cleaner personal care routines emphasizing plant-based ingredients. However, higher price points and limited awareness in developing markets moderate their near-term growth relative to conventional alternatives.

General Wipes dominate the application segment with 61.2% share, reflecting their versatility across daily freshness, travel hygiene, and routine personal care for multiple age groups. Sanitary Wipes serve the more targeted menstruation-related hygiene segment, benefiting from growing menstrual health awareness. Their lower usage frequency compared to general wipes currently limits overall volume, though rising awareness of cycle-specific hygiene needs supports gradual share expansion.

Supermarkets and Hypermarkets lead distribution at 39.9%, offering convenience, competitive pricing, and strong brand exposure that drives both impulse and repeat purchases. Pharmacy and drug stores reinforce trust-based purchase behavior among health-conscious consumers seeking safety-validated products. Online retail channels are growing rapidly through subscription services and discreet delivery models that reduce purchase hesitation, particularly among first-time buyers in conservative or rural markets.

Drivers

Rising awareness of intimate hygiene and its connection to daily health and comfort directly fuels feminine wipes demand. Health education campaigns, digital content, and gynecologist-led guidance have normalized intimate care routines across diverse age groups. Working women in particular drive consistent repeat purchasing as on-the-go hygiene tools fit naturally into commuting and travel schedules. Consequently, everyday usage occasions multiply as wipes shift from occasional to essential personal care items.

Expanding organized retail and e-commerce distribution networks accelerate product accessibility and consumer discovery. Supermarkets, pharmacies, and online platforms improve product comparison, brand visibility, and pricing transparency at scale. Online subscription models and healthcare professional recommendations reduce first-purchase hesitation among new users. Therefore, channel expansion plays an equally important role as product innovation in sustaining the market’s 6.6% CAGR through 2034.

Use Cases

Daily on-the-go hygiene represents the market’s highest-volume use case, particularly among working women and frequent travelers. Feminine wipes provide discreet, portable freshness without access to water or conventional cleansing facilities. Their compact format fits seamlessly into handbags, travel kits, and workplace essentials. This application drives general wipes’ dominant 61.2% application share and sustains strong repeat purchase frequency across urban consumer segments globally.

Additionally, menstruation-related sanitary hygiene represents a targeted and growing application category. Sanitary wipes address specific cleansing needs during menstrual cycles, supporting comfort and infection prevention. Healthcare providers increasingly recommend them as safe complements to standard period care products. As menstrual health awareness expands through public health campaigns and digital education, this application segment is positioned to capture a greater share of total market volume.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Major Challenges

Consumer concerns about synthetic fragrances, alcohol, and chemical preservatives present a significant adoption barrier. These ingredients are frequently associated with skin irritation, allergic reactions, and potential disruption of natural vaginal microbiome balance. Sensitive skin users in particular avoid conventional formulations, creating a trust deficit that limits category-wide penetration. Brands must invest in clean-label reformulation and clinical safety validation to overcome this resistance among health-conscious buyers.

However, social stigma and cultural discomfort around feminine hygiene topics restrain market growth in conservative regions. Limited open discussion, restricted retail promotion, and insufficient healthcare provider outreach collectively suppress awareness and adoption in these markets. Women in such regions often lack reliable information about product safety or necessity. Without targeted education programs and culturally sensitive marketing, these structural barriers will continue to slow penetration in high-potential emerging geographies.

Business Opportunities

Developing gynecologist-approved, plant-based formulations creates a strong premium growth opportunity aligned with consumer safety expectations. Products that combine clean-label credentials, pH-balanced formulations, and clinical endorsements address the primary concerns restraining mainstream adoption. Brands that achieve recognized certifications — cruelty-free, vegan, and dermatologist-tested — can command higher price points while building lasting loyalty. This opportunity is particularly strong in North America and Europe, where ingredient transparency commands measurable purchase premiums.

Moreover, subscription-based and direct-to-consumer digital platforms unlock powerful recurring revenue pathways by addressing privacy and convenience barriers simultaneously. Online models deliver products discreetly to consumers in markets where in-store purchasing feels socially uncomfortable. Subscription services generate predictable demand streams while enabling brands to educate consumers directly and gather product feedback for faster innovation cycles. Emerging economies in Asia Pacific and Latin America offer additional upside as digital commerce infrastructure matures and disposable incomes continue rising.

Regional Analysis

Asia Pacific leads the global feminine wipes market with 46.8% share and revenues of USD 0.7 billion in 2024. A growing urban female population, improving hygiene education, and rapid expansion of supermarket and online retail channels underpin this regional dominance. Rising lifestyle aspirations and healthcare awareness across China, India, and Southeast Asia sustain strong volume consumption. Consequently, Asia Pacific will remain the market’s largest and most dynamic regional engine through 2034.

North America demonstrates steady growth supported by high consumer awareness, premium product acceptance, and strong preventive hygiene culture. Working women actively integrate feminine wipes into daily self-care routines, sustaining consistent demand across pharmacy and e-commerce channels. The U.S. market benefits from wide product availability and health-education initiatives that reinforce routine usage. Additionally, growing preference for dermatologically tested and clean-label formulations continues to drive premiumization across the region’s established consumer base.

Recent Developments

- November 2025 — Edgewell Personal Care Company entered into a definitive agreement to sell its feminine care business to Essity, a Sweden-based global health and hygiene company, for USD 340 million. The transaction allows Edgewell to streamline its portfolio while strengthening Essity’s global position in feminine hygiene solutions.

- January 2024 — The Honey Pot Company, an Atlanta-based and Black-founded feminine care brand, was acquired by Compass Diversified in an all-cash transaction valued at USD 380 million. The acquisition supports the brand’s next growth phase through expanded distribution, accelerated innovation, and broader market reach within the feminine wellness category.

Conclusion

The global feminine wipes market is on a well-supported growth trajectory driven by intersecting demand forces across health, lifestyle, and sustainability. A 6.6% CAGR through 2034 reflects structural tailwinds including rising female workforce participation, expanding hygiene awareness, and growing e-commerce accessibility. Clean-label innovation and gynecologist-endorsed positioning are rapidly redefining competitive standards across the category.

Synthetic and conventional formats currently lead their segments, but natural, organic, and biodegradable alternatives are gaining measurable momentum. Asia Pacific holds regional leadership at 46.8% share and USD 0.7 billion in revenues, while North America sustains premium-tier growth through health-conscious consumer demand. General wipes and supermarket channels dominate consumption today, though online subscription and sanitary-specific products represent the fastest-growing sub-segments.

Brands that prioritize clean formulations, clinical safety certifications, and culturally sensitive digital distribution strategies will capture the greatest share of future growth. Addressing ingredient safety concerns and social stigma barriers in emerging markets will unlock substantial untapped demand. The market is projected to reach USD 3.2 billion by 2034, rewarding companies that act decisively on these strategic imperatives now.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)