Table of Contents

Introduction

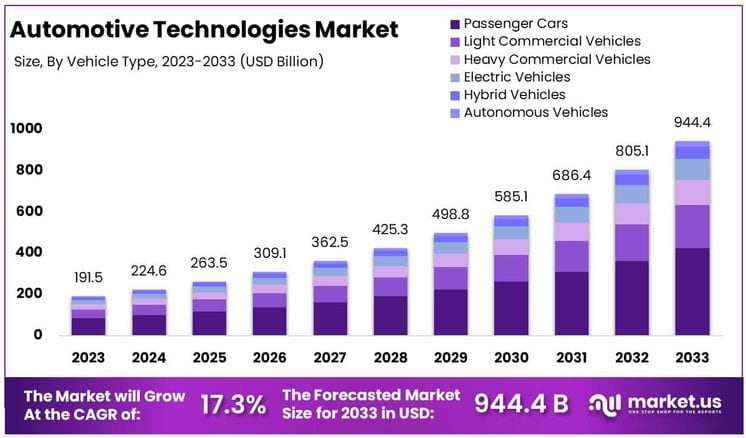

The Global Automotive Technologies Market is projected to reach approximately USD 944.4 billion by 2033, up from USD 191.5 billion in 2023, exhibiting a compound annual growth rate (CAGR) of 17.3% during the forecast period from 2024 to 2033.

The Automotive Technologies Market encompasses a broad range of innovations, including advanced driver-assistance systems (ADAS), electric and hybrid powertrains, connected vehicle technologies, and autonomous driving solutions. Automotive technologies refer to the integration of electronics, software, and artificial intelligence to enhance vehicle performance, safety, and user experience.

The market is witnessing significant growth, driven by stringent government regulations on vehicle emissions, rising consumer demand for fuel efficiency, and the rapid adoption of electrification and autonomous mobility solutions. Additionally, advancements in connectivity, such as vehicle-to-everything (V2X) communication, are revolutionizing transportation by enabling real-time data exchange between vehicles and infrastructure. The increasing adoption of electric vehicles (EVs) further propels market expansion, as automakers invest heavily in battery efficiency, charging infrastructure, and lightweight materials.

Rising demand for safer and more efficient transportation solutions, coupled with technological breakthroughs in artificial intelligence and machine learning, is accelerating innovation in autonomous and semi-autonomous vehicles. The market presents significant opportunities for automotive OEMs, Tier 1 suppliers, and technology firms to capitalize on smart mobility solutions, shared transportation models, and sustainable automotive technologies.

Emerging economies, particularly in Asia-Pacific, offer lucrative growth prospects due to rapid urbanization, rising disposable incomes, and government incentives for EV adoption. However, challenges such as high R&D costs, cybersecurity threats, and supply chain disruptions remain key concerns for market players. As the industry shifts towards software-defined vehicles and digital ecosystems, strategic partnerships, continuous innovation, and regulatory compliance will be critical for long-term success in the evolving automotive landscape.

Key Takeaways

- The global automotive technologies market, valued at USD 191.5 billion in 2023, is projected to reach USD 944.4 billion by 2033, growing at a CAGR of 17.3% 2024–2033.

- Remote Diagnostics holds the largest share 24.3%, enabling efficient vehicle maintenance and real-time monitoring. 3D Automotive Printing is transforming production processes through rapid prototyping and cost reduction.

- Passenger Cars lead the market with 45% share, driven by high sales volume and continuous technological advancements.

- Driver Assistance Systems account for 32%, supported by the rising focus on vehicle safety and semi-autonomous driving technologies.

- Asia Pacific Holds the largest market share 37.1%, driven by high vehicle production and rapid technology integration.

- North America Represents 25%, benefiting from strong adoption of advanced automotive technologies.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 191.5 Billion |

| Forecast Revenue (2033) | USD 944.4 Billion |

| CAGR (2024-2033) | 17.3% |

| Segments Covered | By Technologies (Remote Diagnostics, 3D Automotive Printing, On-Board Internet Services, Advanced Heads-Up Display, Automotive Security Systems, Biometric Vehicle Access Systems, Vehicle Intelligence Systems, Night Vision, Blind Spot Detection Systems, Other Technologies), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Electric Vehicles (EVs), Hybrid Vehicles, Autonomous Vehicles), By Application (Passenger Safety, Driver Assistance, Navigation and Telematics, Entertainment, Fleet Management, Vehicle Maintenance, Emission Control, Energy Management, Others) |

| Competitive Landscape | Delphi Automotive PLC , Continental AG , Robert Bosch GmbH , Agero Inc. , Airbiquity Inc. , and WirelessCar AB , AT&T Inc. , Verizon , Vodafone Group Plc , |

Automotive Technologies Statistics

- Global electric vehicle (EV) sales reached 14 million in 2023, rising from 10.5 million in 2022. EVs accounted for 14% of all new car sales, up from 8.3% in 2021.

- China led the global EV market, making up over 50% of sales. The U.S. and Europe followed, with Norway reaching 90% EV adoption in new car sales.

- Public EV chargers worldwide increased to 2.7 million in 2022, growing by 55% from the previous year.

- Nearly half of U.S. consumers remain hesitant about autonomous vehicles. Younger generations show greater acceptance.

- Autonomous vehicle technology faces regulatory and safety challenges. The sector is projected to generate $13 billion in revenue by 2030.

- By 2023, there were 192 million connected cars globally. In the U.S., 80% of new vehicles supported Apple CarPlay and Android Auto.

- The number of connected cars is set to reach 367 million by 2027 as connectivity becomes standard.

- Lithium-ion battery production accounts for 40-60% of total EV manufacturing emissions. This surpasses emissions from other vehicle materials.

- Road transport contributes over 15% of global energy-related emissions. EVs are essential for reducing this impact.

- SUV sales in the U.S. have surged, while sedan sales have dropped by 25% over the past five years.

Emerging Trends

- Electric Vehicle (EV) Adoption: The global shift towards electric vehicles is accelerating, with EV sales reaching approximately 14 million units in 2023, accounting for about 18% of total vehicle sales.

- Vehicle-to-Everything (V2X) Communication: Advancements in V2X technologies enable vehicles to communicate with each other and infrastructure, enhancing road safety and traffic efficiency.

- Integration of Artificial Intelligence (AI): AI is being incorporated into vehicles to improve functionalities such as voice recognition, driver assistance systems, and autonomous driving capabilities.

- Connected Vehicles: The rise of connected cars, equipped with internet access and capable of sharing data with external devices, is transforming the driving experience and enabling new services.

- Digital Transformation in Manufacturing: The automotive industry is embracing digital technologies to enhance manufacturing processes, improve efficiency, and reduce costs.

Top Use Cases

- Advanced Driver Assistance Systems (ADAS): These systems utilize sensors and cameras to assist drivers in tasks such as lane-keeping, adaptive cruise control, and collision avoidance, enhancing safety.

- Predictive Maintenance: Connected vehicles can monitor their own health and predict potential failures, allowing for proactive maintenance and reducing downtime.

- In-Vehicle Infotainment Systems: Modern vehicles offer integrated infotainment systems that provide navigation, entertainment, and connectivity features to enhance the user experience.

- Fleet Management: Telematics and connectivity enable fleet operators to monitor vehicle locations, optimize routes, and improve operational efficiency.

- Autonomous Parking: Self-parking technologies allow vehicles to park themselves without driver intervention, improving convenience and reducing parking-related accidents.

Major Challenges

- Cybersecurity Risks: As vehicles become more connected, they are increasingly vulnerable to cyber-attacks, necessitating robust security measures.

- Infrastructure Development: The widespread adoption of EVs requires significant investment in charging infrastructure to meet growing demand.

- Regulatory Compliance: Automakers must navigate complex and varying regulations across different regions, particularly concerning emissions and safety standards.

- Consumer Acceptance: There is a need to build consumer trust and acceptance of new technologies, especially autonomous driving features.

- Supply Chain Disruptions: Global events and economic fluctuations can disrupt the automotive supply chain, affecting production and delivery schedules.

Top Opportunities

- Development of Sustainable Materials: Innovations in materials science can lead to lighter, more efficient vehicles with reduced environmental impact.

- Expansion of Mobility-as-a-Service (MaaS): Integrating various forms of transportation into a single accessible service presents opportunities for growth in urban mobility solutions.

- Advancements in Battery Technology: Improving battery efficiency and reducing costs can accelerate EV adoption and enhance vehicle performance.

- Integration of 5G Technology: The deployment of 5G networks can enhance vehicle connectivity, enabling faster data transmission and more reliable communication.

- Development of Autonomous Vehicles: Progress in autonomous driving technologies offers opportunities to revolutionize transportation, improve safety, and reduce congestion.

Key Player Analysis

The Global Automotive Technologies Market in 2024 is shaped by key players driving innovation in connectivity, automation, and electrification. Delphi Automotive PLC and Robert Bosch GmbH remain at the forefront with advancements in powertrain solutions and ADAS (Advanced Driver Assistance Systems), strengthening their market dominance. Continental AG continues to lead in intelligent mobility, leveraging sensor technologies and software-defined vehicle capabilities.

Agero Inc. and Airbiquity Inc. are enhancing vehicle telematics and cloud-based software integration, accelerating the adoption of connected car services. WirelessCar AB, a subsidiary of Volkswagen Group, plays a crucial role in developing digital vehicle services and fleet management solutions. In telecommunications, AT&T Inc., Verizon, and Vodafone Group Plc drive the 5G-enabled automotive ecosystem, facilitating V2X (Vehicle-to-Everything) communication and enhancing in-vehicle connectivity. As competition intensifies, strategic collaborations, AI-driven innovations, and cybersecurity enhancements will remain pivotal in shaping the market landscape and ensuring long-term growth.

Market Key Players

- Delphi Automotive PLC

- Continental AG

- Robert Bosch GmbH

- Agero Inc.

- Airbiquity Inc.

- WirelessCar AB

- AT&T Inc.

- Verizon

- Vodafone Group Plc

Regional Analysis

The Asia Pacific region dominates the global automotive technologies market, accounting for 37.1% of the market share in 2024. This dominance is primarily driven by the strong presence of key automotive manufacturing hubs, including China, Japan, South Korea, and India, which collectively contribute to high vehicle production and technological advancements.

China, as the world’s largest automotive market, has been a key driver, supported by government incentives for electric vehicles (EVs) and autonomous driving technologies. Japan and South Korea lead in automotive electronics, ADAS (Advanced Driver Assistance Systems), and hybrid vehicle technologies, with major automakers such as Toyota, Honda, Hyundai, and Nissan spearheading innovation. Additionally, India’s expanding automotive sector, supported by favorable policies such as the Faster Adoption and Manufacturing of Electric Vehicles (FAME) initiative, is fostering growth in EV adoption and smart mobility solutions.

The region benefits from a robust supply chain, lower production costs, and rapid urbanization, further accelerating the adoption of connected, autonomous, shared, and electric (CASE) vehicles. With increasing investments in AI-driven mobility solutions, battery manufacturing, and smart transportation infrastructure, Asia Pacific is expected to maintain its leadership position in the global automotive technologies market.

Recent Developments

- In 2025, American Axle & Manufacturing (AAM) (NYSE: AXL) confirmed an agreement with Dowlais Group plc (LON: DWL) for a strategic cash and share acquisition valued at approximately $1.44 billion. This combination aims to strengthen AAM’s global presence and enhance its technological capabilities in the automotive sector.

- In 2024, Rivian Automotive (NASDAQ: RIVN) and Volkswagen Group (XETRA: VOW / VOW3) announced a joint venture, “Rivian and VW Group Technology, LLC,” with a deal worth up to $5.8 billion. The collaboration will drive innovation in electric vehicle software and architecture, expanding both companies’ reach across multiple vehicle segments.

- In 2024, Hyundai Motor Group committed $923 million to Motional, its self-driving joint venture with Aptiv PLC. The investment highlights Hyundai’s ongoing efforts to advance autonomous vehicle technology despite challenges in deploying robotaxi services at scale.

- In 2024, Nissan, Honda, and Mitsubishi Motors signed an MOU to assess Mitsubishi Motors’ potential participation in a joint holding company initiative spearheaded by Nissan and Honda. This agreement focuses on exploring synergies to drive efficiency and collaboration within the automotive industry.

- In 2025, Zeekr (NYSE: ZK) finalized its integration of Lynk & Co and unveiled its 2025 product strategy. The move is set to consolidate resources and position Zeekr as a major automotive player with an annual production target of one million units.

- In 2023, Stellantis N.V. invested approximately €1.5 billion to acquire a 20% stake in Leapmotor, forming Leapmotor International, a 51/49 Stellantis-led joint venture. This agreement grants exclusive rights for exporting, selling, and manufacturing Leapmotor vehicles outside Greater China, marking a new phase in global EV collaborations.

Conclusion

The automotive technologies market is set for strong growth, driven by the rising adoption of electric vehicles, advancements in autonomous driving, and increasing connectivity in vehicles. Innovations in AI, telematics, and software-defined vehicles are reshaping mobility, enhancing safety, and improving efficiency. Asia-Pacific remains the dominant region due to high vehicle production and rapid technology integration. However, cybersecurity risks, infrastructure challenges, and regulatory complexities persist. To stay competitive, industry players must prioritize continuous innovation, strategic collaborations, and regulatory compliance while leveraging emerging trends in smart mobility and sustainable automotive solutions.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)