Table of Contents

Introduction

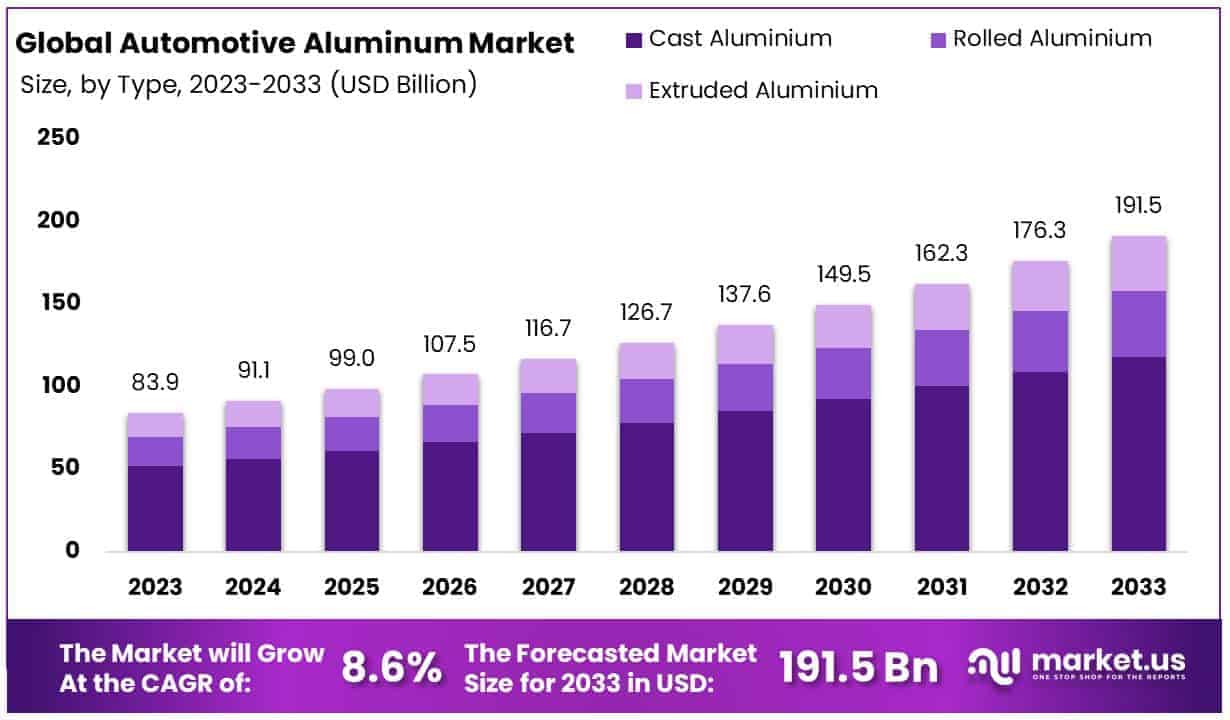

The Global Automotive Aluminum Market is projected to reach approximately USD 191.5 billion by 2033, up from USD 83.9 billion in 2023, reflecting a compound annual growth rate (CAGR) of 8.60% from 2024 to 2033.

Automotive aluminum refers to aluminum alloys specifically designed for use in the manufacturing of vehicles, primarily for components such as body panels, engines, wheels, and chassis. The automotive aluminum market encompasses the production, supply, and demand dynamics of aluminum materials used by automakers to reduce vehicle weight, enhance fuel efficiency, and comply with stringent emissions regulations. The market is poised for growth, driven by rising demand for lightweight materials in response to increasing fuel efficiency standards and consumer preference for sustainable vehicles.

Additionally, the growing adoption of electric vehicles (EVs), which require lightweight materials to offset battery weight, has significantly contributed to the demand for automotive aluminum. Opportunities within the market are further bolstered by technological advancements in aluminum production, enabling cost reduction and improved material properties. As automakers seek to meet regulatory requirements and improve vehicle performance, the automotive aluminum market is expected to expand, driven by innovation and sustainability trends.

Fundamental Insights

- The global automotive aluminum market is projected to grow significantly, reaching approximately USD 191.5 billion by 2033, up from USD 83.9 billion in 2023. This represents a compound annual growth rate (CAGR) of 8.60% during the forecast period from 2024 to 2033.

- Cast aluminum leads the market with the largest share of 61.8%, driven by its versatility and efficiency in manufacturing complex automotive components.

- The powertrain application category holds the largest market share at 39.8%, primarily due to the increasing emphasis on enhancing vehicle performance and fuel efficiency.

- The passenger car segment accounts for 59% of the market, reflecting strong consumer demand for fuel-efficient and high-performance vehicles.

- North America is the leading region, commanding 44.2% of the market share. Europe follows with a notable 24.8% share, driven by efforts to reduce vehicle weight in line with CO2 emission reduction targets.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 83.9 Billion |

| Forecast Revenue (2033) | USD 191.5 Billion |

| CAGR (2024-2033) | 8.60% |

| Segments Covered | By Product Type (Cast Aluminium, Rolled Aluminium, Extruded Aluminium), By Application (Powertrain, Chassis, Suspension), By Vehicle Type (Passenger Cars, LCVs, HCV) |

| Competitive Landscape | Alcoa Corporation, UACJ Corporation, Norsk Hydro ASA, Constellium, Rio Tinto Group, Aleris Corporation, Autoneum Holding AG, Dana Limited, ElringKlinger AG, Jindal Aluminium ltd, Kaiser Aluminium, Lorin Industries |

Key Segments Analysis

The Automotive Aluminum Market is primarily driven by three product types: cast aluminum, rolled aluminum, and extruded aluminum. Cast aluminum dominates with a 61.8% market share, favored for its versatility in producing complex, high-precision parts like engine blocks and wheels, while offering a balance of strength and lightweight properties that enhance fuel efficiency and performance. Rolled aluminum, used for body sheets and plates, is gaining traction due to its ductility, which is crucial for lightweight, durable exterior panels. Extruded aluminum is key for structural components, providing an optimal balance between strength and weight. Although cast aluminum leads, the growth of rolled and extruded aluminum is essential in meeting the automotive industry’s demand for lighter materials to improve fuel economy and comply with emissions regulations.

The powertrain segment leads the Automotive Aluminum Market, accounting for 39.8% of the market share, driven by the automotive industry’s emphasis on improving vehicle performance and fuel efficiency. Aluminum’s lightweight properties are crucial in enhancing engine and transmission designs, reducing vehicle weight, and improving fuel economy. Other significant segments, such as chassis and suspension, also contribute to weight reduction and vehicle handling, but with a lesser impact on fuel efficiency. The growing adoption of electric vehicles (EVs) is expected to further boost demand for aluminum in powertrains, as manufacturers prioritize lightweight components to improve range and meet stringent emissions standards, ensuring the continued dominance of the powertrain segment.

The Automotive Aluminum Market is predominantly driven by passenger cars, which account for 59% of the market, due to rising consumer demand for fuel-efficient, high-performance vehicles that comply with stringent emissions standards. Aluminum’s lightweight properties improve fuel economy and reduce CO2 emissions, making it a key material for body panels, powertrain components, and more. While Light Commercial Vehicles (LCVs) and Heavy Commercial Vehicles (HCVs) also use aluminum for similar reasons, the volume of aluminum in passenger cars is higher due to their greater production numbers and focus on lightweighting. As the industry shifts toward electric and hybrid vehicles, aluminum demand in passenger cars is expected to grow further, driven by the need to offset battery weight and enhance vehicle range. LCVs and HCVs are also likely to see gradual growth in aluminum usage as they adopt lightweighting and electrification strategies.

Emerging Trends

- Lightweighting and Fuel Efficiency: A primary driver in the automotive industry is the demand for lightweight vehicles to improve fuel efficiency. Aluminum is being increasingly adopted due to its high strength-to-weight ratio, making it ideal for reducing vehicle weight. This trend is in response to stricter fuel economy regulations and consumer preferences for more fuel-efficient vehicles. The shift to electric vehicles (EVs) is also boosting the demand for lightweight materials, as it contributes to extending the range of EVs.

- Sustainability and Recycling: The automotive industry is moving towards more sustainable practices, with aluminum being a key material due to its recyclability. Approximately 75% of all aluminum ever produced is still in use today, largely driven by its ability to be recycled without losing quality. This sustainability aspect is making aluminum more attractive as manufacturers aim to reduce their carbon footprint and meet environmental regulations.

- Advanced Manufacturing Techniques: The adoption of new manufacturing techniques such as advanced casting, 3D printing, and high-pressure die-casting is enabling more complex and efficient use of aluminum in automotive parts. These innovations allow for the production of lighter, stronger, and more precise components, which enhance vehicle safety and performance. As technology improves, the use of aluminum in both structural and aesthetic components is expected to increase.

- Use of Aluminum in Electric Vehicles (EVs): The rise of electric vehicles is influencing the adoption of aluminum as a key material for battery enclosures, body panels, and frames. Aluminum’s lightweight nature helps mitigate the heavy weight of battery packs, improving the overall performance and efficiency of EVs. As the EV market grows, so does the demand for aluminum components.

- Automotive Aluminum Alloys: The development of new, high-strength aluminum alloys is expanding the use of aluminum in more critical automotive applications. Alloys like 7xxx and 5xxx are being developed to offer enhanced durability and performance for automotive applications that require high structural integrity. These alloys are being incorporated into the body, chassis, and suspension systems of vehicles, improving crashworthiness and overall vehicle safety.

Top Use Cases

- Body Panels and Structure: Aluminum is widely used for outer body panels, hoods, doors, and fenders due to its lightweight properties. By replacing steel with aluminum, automakers can reduce the vehicle’s overall weight, improving fuel efficiency and handling. Aluminum body panels make up approximately 15-20% of the total weight of a typical vehicle.

- Engine Components: Aluminum is a preferred material for engine blocks, cylinder heads, pistons, and other engine components due to its ability to withstand high temperatures and reduce weight. This contributes to improved vehicle performance and fuel economy. Aluminum engine components account for up to 40% of the total weight of an engine.

- Wheels: Aluminum wheels are a common use case in automotive manufacturing. They are used not only for their lightweight properties but also for their ability to dissipate heat, which improves braking performance. Aluminum wheels are estimated to account for around 12-15% of the total vehicle weight, contributing to better fuel efficiency and performance.

- Battery Enclosures for Electric Vehicles: In electric vehicles, aluminum is increasingly being used for battery enclosures. It helps to protect the battery from external damage while also contributing to weight reduction, which is critical for maximizing range. In EVs, aluminum makes up about 25% of the battery pack’s housing.

- Chassis and Suspension Systems: The chassis, suspension arms, and other underbody components are often made from high-strength aluminum alloys. These components benefit from the material’s strength-to-weight ratio, offering improved handling, durability, and safety. In some cases, aluminum can reduce the weight of the chassis by up to 30%, making it an essential part of modern automotive design.

Major Challenges

- Cost of Production: The production cost of aluminum is relatively high compared to other materials like steel, which makes it a costly option for automakers. Despite the benefits, the expense of sourcing and processing aluminum can be a barrier to its widespread adoption, especially in low-cost vehicle segments. The price volatility of aluminum due to global supply chains also impacts manufacturers’ budgeting.

- Difficulties in Joining Aluminum Parts: One significant challenge is the difficulty in joining aluminum parts with traditional welding techniques. Aluminum requires specialized welding processes, such as laser or friction stir welding, which can increase production costs and complexity. Moreover, these advanced techniques require specific expertise and equipment, which may not be available in all manufacturing facilities.

- Corrosion Resistance Issues: While aluminum is naturally resistant to corrosion, the surface may still degrade when exposed to harsh environmental conditions, leading to premature aging of vehicle parts. To combat this, manufacturers must invest in additional protective coatings or treatments, such as anodizing, which increases the overall cost of aluminum components.

- Limited Material Knowledge and Skills: The transition to aluminum requires automakers to adopt new knowledge and skills. Many technicians and engineers are more familiar with working with steel, and there is a learning curve when it comes to aluminum fabrication, joining, and finishing. A shortage of skilled labor and training programs can delay the full integration of aluminum in production.

- Recycling Challenges: Although aluminum is highly recyclable, the process can still be inefficient and costly. Recycling aluminum from end-of-life vehicles (ELVs) presents challenges, particularly in separating aluminum from other materials like plastic and steel. Additionally, the energy required for recycling, though lower than the production of primary aluminum, still poses challenges to sustainability goals.

Top Opportunities

- Rising Demand for Electric Vehicles (EVs): The growing popularity of electric vehicles offers significant opportunities for aluminum. With EVs typically being heavier due to their battery packs, the demand for lightweight materials like aluminum is expected to increase. The need for aluminum in EV body panels, battery enclosures, and structural components is likely to rise as manufacturers aim to increase range and efficiency.

- Automotive Lightweighting Initiatives: The global push for fuel efficiency and regulatory requirements on emissions are driving automotive manufacturers to adopt lightweighting technologies. As aluminum offers a superior strength-to-weight ratio, it is increasingly used in the production of body panels, engine components, and structural parts to reduce the weight of vehicles and improve fuel efficiency.

- Government Regulations and Sustainability Initiatives: Government regulations mandating lower emissions and improved fuel economy are likely to create more opportunities for the use of aluminum in the automotive sector. Aluminum’s recyclability and lower environmental impact in comparison to other metals provide an avenue for automakers to meet these stringent regulations while lowering overall lifecycle emissions.

- Technological Advancements in Aluminum Alloys: The development of new, high-strength aluminum alloys can expand the material’s use in more critical automotive applications. These alloys offer better performance in high-stress environments, such as suspension systems and chassis components. As new alloy technologies continue to evolve, the scope for aluminum in the automotive industry will increase, particularly in high-performance vehicles.

- Collaborations with Recycling Industry: As the automotive industry faces mounting pressure to reduce carbon emissions, collaborations with the recycling industry offer substantial growth potential. With advancements in recycling technology and infrastructure, automakers can source more recycled aluminum, which is both environmentally and economically advantageous. Such practices not only reduce raw material costs but also align with sustainability goals, further boosting aluminum’s role in the industry.

Key Player Analysis

- Alcoa Corporation: Alcoa Corporation is a global leader in the aluminum industry, with a strong focus on sustainable practices and innovations. The company has a significant presence in the automotive aluminum market, providing lightweight, high-strength aluminum solutions to the automotive sector. The company is known for its high-performance aluminum alloys, which are used in vehicle body structures, engine components, and wheels. Alcoa’s focus on reducing carbon emissions in aluminum production further enhances its market position.

- UACJ Corporation: UACJ Corporation, a leading player in the automotive aluminum market, is recognized for its advanced manufacturing capabilities. The company offers a wide range of aluminum products, including rolled products, castings, and extrusions, which are used extensively in automotive applications. The company has been instrumental in supplying aluminum sheets for lightweight car bodies, thereby contributing to fuel efficiency and sustainability.

- Norsk Hydro ASA: Norsk Hydro ASA is a Norwegian multinational aluminum company that has a strong presence in the global automotive market. Hydro’s aluminum solutions are widely used for various automotive applications, including body panels, heat exchangers, and suspension components. The company is also focusing on increasing the use of recycled aluminum to minimize environmental impact.

- Constellium: Constellium is a key player in the production of aluminum products for the automotive industry, known for its expertise in high-strength aluminum alloys. The company supplies a wide range of aluminum products, including rolled and extruded solutions, to major automakers. The company’s innovative technologies contribute to reducing vehicle weight, improving fuel efficiency, and meeting stringent environmental regulations.

- Rio Tinto Group: Rio Tinto Group is a multinational mining and metals company with a significant share in the aluminum production sector. Through its subsidiary, Rio Tinto Aluminium, the company produces aluminum products used across various industries, including automotive. The company focuses on developing new aluminum production technologies that reduce greenhouse gas emissions and support the automotive industry’s transition to greener alternatives.

Regional Analysis

North America: Automotive Aluminum Market with Largest Market Share of 44.2% in 2023

The automotive aluminum market in North America is the largest and most dominant in terms of both market share and value, accounting for 44.2% of the global market in 2023, with an estimated market size of USD 37 billion. The region’s leadership can be attributed to the growing adoption of lightweight materials in automotive manufacturing, primarily driven by stringent fuel efficiency and emission regulations.

The increasing demand for electric vehicles (EVs), which require lighter materials to enhance range and battery efficiency, has further bolstered the use of aluminum in the automotive sector. Additionally, North America’s well-established automotive industry, particularly in the U.S. and Canada, along with a strong presence of key industry players, contributes significantly to the region’s substantial share of the market.

The extensive investment in research and development for advanced aluminum alloys and manufacturing technologies also plays a critical role in maintaining North America’s dominant position. Furthermore, the region’s robust infrastructure, well-developed supply chains, and substantial demand for automotive components support continued market growth, positioning North America as a key driver in the global automotive

Recent Developments

- In 2023, Arconic Corporation (NYSE: ARNC) announced a definitive agreement to be acquired by Apollo Global Management, Inc. (NYSE: APO) in a cash transaction valued at approximately $5.2 billion. The deal also includes a minority investment from Irenic Capital Management.

- In February 2024, Kaiser Aluminum Corporation (NASDAQ: KALU) revealed plans to release its financial and operational results for the fourth quarter and full year of 2023 on February 21, 2024, after market close. A conference call will be held the following day at 9:00 a.m. Central Time.

- In May 2023, Novelis Inc. announced the launch of its new roll forming development line, aimed at addressing growing demand for high-strength aluminum auto parts. The line is part of Novelis’ ongoing efforts to meet industry requirements for sustainable and efficient aluminum production.

- In 2023, Magna International, in collaboration with the Pacific Northwest National Laboratory (PNNL), introduced a more sustainable manufacturing process for aluminum auto parts. This new process aims to reduce dependence on newly sourced aluminum, offering environmental and cost benefits to suppliers.

Conclusion

The automotive aluminum market is positioned for sustained growth as the demand for lightweight materials continues to rise, driven by the need for improved fuel efficiency, enhanced vehicle performance, and stricter environmental regulations. The increasing adoption of electric vehicles further accelerates this trend, as aluminum’s strength-to-weight ratio helps offset the weight of battery packs, improving range and efficiency. Technological advancements in manufacturing and the development of high-strength aluminum alloys are expected to expand the material’s use in more critical automotive applications, reinforcing aluminum’s role in the industry. As automakers increasingly focus on sustainability and regulatory compliance, the market for automotive aluminum is set to evolve, offering numerous opportunities for growth and innovation.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)