Table of Contents

Market Overview

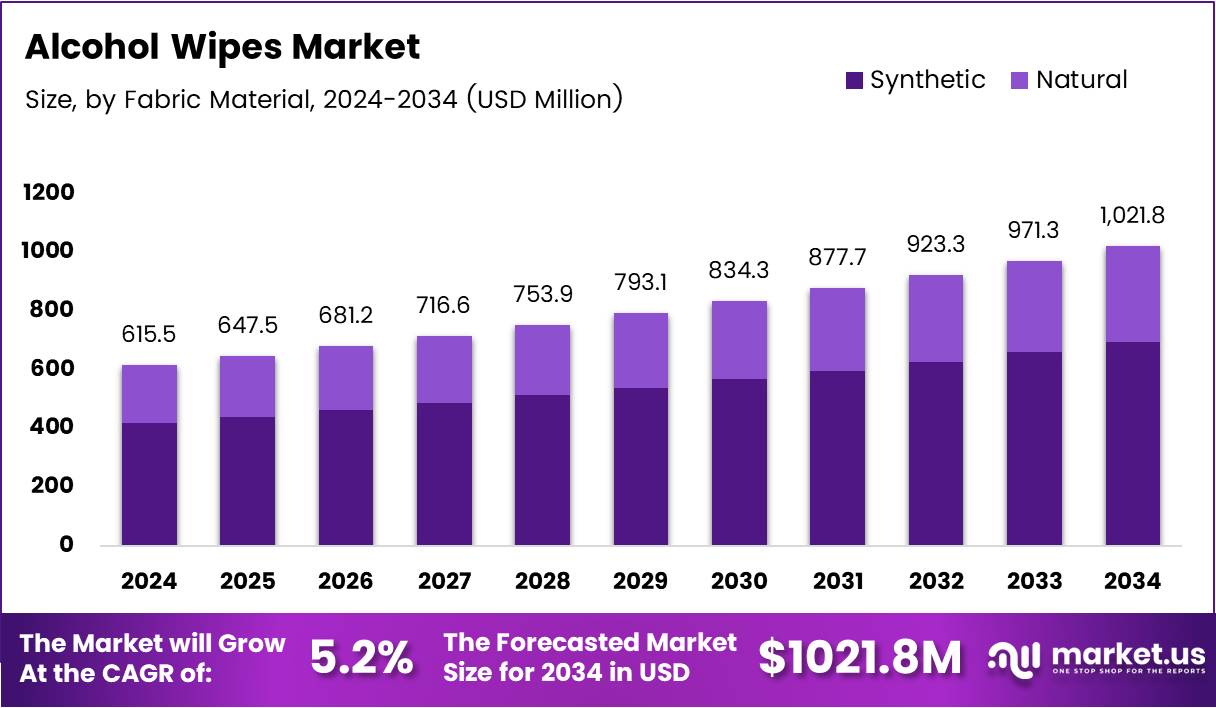

The global alcohol wipes market is valued at USD 615.5 Million in 2024 and is projected to reach USD 1021.8 Million by 2034. The market grows at a CAGR of 5.2% during the forecast period from 2025 to 2034. Rising hygiene awareness and expanding institutional demand drive this consistent upward trajectory.

Alcohol wipes are pre-moistened disposable sheets infused with isopropyl or ethyl alcohol. They deliver fast surface and hand disinfection across medical, household, and commercial environments. Healthcare professionals, households, and facility managers rely on them for reliable, rapid germ removal without requiring additional tools or water.

Healthcare institutions consume alcohol wipes extensively for infection control and surface decontamination. Food service operators, hospitality businesses, and manufacturing facilities integrate them into daily sanitation protocols. Personal care users adopt them for on-the-go hygiene, portable convenience, and multipurpose household cleaning tasks.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Manufacturers now integrate skin-conditioning agents such as aloe vera and vitamin E into formulations. These additions address user concerns about dryness and irritation, expanding the consumer base. Improved substrate technology also enables faster drying times and reduced lint, raising clinical performance expectations across both professional and consumer segments.

Government sanitation mandates across hospitals, clinics, and food-service environments reinforce purchasing obligations. Infection-prevention compliance programs increase institutional procurement volumes. Additionally, public health campaigns promoting personal hygiene create sustained household demand, supporting stable revenue growth for producers supplying both regulated and consumer retail channels.

A clinical study found that alcohol-based wipes reduced transient hand bacteria by 90% among 75 study participants, validating their medical utility. A consumer survey also confirmed that 92% of users engage with disinfecting wipes, while 83% of households use them weekly. These figures confirm deep market penetration and reinforce long-term demand fundamentals.

Key Takeaways

- The global alcohol wipes market grows from USD 615.5 Million in 2024 to USD 1021.8 Million by 2034, at a CAGR of 5.2%.

- The synthetic fabric segment leads by material type with a 69.2% market share in 2024.

- The personal and household end-use segment dominates with a 67.1% share, driven by daily hygiene habits.

- Supermarkets and hypermarkets hold the largest distribution channel share at 44.8%.

- North America leads all regions with a 44.2% market share, valued at USD 272.0 Million.

- Clinical evidence shows alcohol wipes reduce transient hand bacteria by 90%, reinforcing healthcare adoption.

- Weekly household use reaches 83% penetration, confirming strong recurring consumer demand.

Market Segmentation Overview

The synthetic fabric segment holds a dominant 69.2% share of the alcohol wipes market in 2024. Manufacturers favor synthetic materials for their high tensile strength, quick-drying properties, and reliable compatibility with alcohol-based formulations. These qualities allow brands to consistently meet rising hygiene performance standards across both clinical and consumer applications.

The natural fabric segment grows steadily as eco-conscious buyers seek biodegradable alternatives. Regulatory encouragement and retailer sustainability commitments accelerate adoption of plant-based substrates. Although synthetics maintain dominance, natural fabric wipes build incremental market share as environmental awareness reshapes purchasing priorities globally.

The personal and household end-use segment captures 67.1% of total market share. Consumers prioritize convenience, portability, and multipurpose functionality, driving consistent replenishment cycles. Product innovation including travel-sized packs, fragrance-free variants, and skin-safe formulations sustains this segment’s leadership across retail and e-commerce channels.

The commercial segment expands steadily across healthcare, hospitality, and food service industries. Regulatory compliance requirements mandate regular disinfection routines, creating predictable institutional demand. Moreover, businesses increasingly standardize alcohol wipes within facility hygiene protocols, broadening the segment’s scope beyond traditional medical environments.

Supermarkets and hypermarkets lead distribution with a 44.8% share, benefiting from high product visibility and impulse-buy placement. Shoppers encounter wipes during routine grocery trips, reducing the need for dedicated hygiene store visits. Competitive shelf pricing and bulk formats further encourage household stockpiling behavior.

The online channel grows rapidly as consumers embrace digital purchasing for convenience and variety. E-commerce platforms offer subscription models, bulk discounts, and doorstep delivery, accelerating repeat purchases. Convenience stores supplement both channels by serving on-the-go users seeking immediate access at transit and residential locations.

Data-Driven Insights for Smarter Business Decisions: Explore the Full Report

Drivers

Consumers increasingly demand portable, no-rinse disinfection solutions for travel, commuting, and outdoor activity. Compact alcohol wipe packs address this preference directly, enabling fast sanitation without water access. Manufacturers respond by launching single-use sachets and resealable pouches, expanding product reach into vending machines, pharmacies, and impulse-buy retail formats.

Healthcare institutions enforce strict infection-control protocols that mandate alcohol wipe use at every patient contact point. Rising hospital admission rates and growing clinic networks amplify purchasing volumes across North America, Europe, and Asia Pacific. Consequently, medical procurement programs generate stable bulk orders that support consistent revenue for leading wipe manufacturers.

Use Cases

Hospitals use alcohol wipes to disinfect medical equipment, examination surfaces, and IV insertion sites between patient interactions. This application reduces healthcare-associated infection risks and meets regulatory cleanliness standards. Rapid-action formulations enable clinical staff to maintain high-frequency disinfection routines without disrupting patient care workflows.

Additionally, households apply alcohol wipes to high-touch surfaces including door handles, remote controls, and kitchen counters. Parents use them for quick child hygiene management during travel or outdoor meals. This daily-use pattern creates consistent replenishment demand, ensuring that personal care retail shelves sustain reliable sell-through velocity throughout the year.

Major Challenges

Isopropyl and ethyl alcohol prices fluctuate based on petrochemical supply chains and seasonal demand shifts. These cost swings compress manufacturer margins and complicate stable retail pricing strategies. Producers who cannot absorb input cost increases risk losing competitiveness to private-label alternatives, particularly in price-sensitive emerging market retail environments.

However, repeated alcohol wipe use causes skin dryness, redness, and irritation among sensitive users, including healthcare workers on long shifts. This concern leads some consumers to substitute non-alcoholic wipes or foam-based alternatives. Manufacturers must invest in skin-conditioning formulations to retain these users, which raises production complexity and may limit margin improvement potential.

Business Opportunities

Brands that develop certified biodegradable wipes using compostable substrates unlock access to a rapidly growing eco-conscious consumer segment. Retailers increasingly allocate dedicated shelf space for sustainable hygiene products, creating favorable distribution opportunities. Companies that achieve credible environmental certifications gain brand differentiation in markets where sustainability messaging drives purchasing decisions.

Moreover, the expansion of home healthcare and telehealth services generates demand for medical-grade wipes suitable for patient self-care. Caregivers and chronic disease patients require hospital-quality disinfection at home, creating a premium product category. Manufacturers who develop dermatologist-approved, clinical-strength formulations for direct-to-consumer retail channels can capture significant incremental revenue.

Regional Analysis

North America leads the global alcohol wipes market with a 44.2% share, valued at USD 272.0 Million in 2024. A well-established healthcare infrastructure, high consumer hygiene awareness, and strong institutional procurement programs underpin this dominance. Continuous product innovation and broad retail availability across supermarkets and e-commerce further entrench the region’s leadership position.

Asia Pacific emerges as the fastest-growing regional market, fueled by expanding hospital networks, rapid urbanization, and rising per-capita incomes. Countries including China, India, and South Korea accelerate retail penetration as disposable hygiene products gain mainstream acceptance. Pharmaceutical distribution growth and government public-health investments amplify demand for both consumer and clinical-grade alcohol wipes across the region.

Recent Developments

- June 2025 — DUDE Wipes secured a strategic growth investment from TSG Consumer, strengthening financial backing and accelerating retail expansion and product innovation plans.

- February 2025 — Harrisons completed the acquisition of Ecotech (Europe) LTD.’s business and assets, extending its European footprint in sustainability and hygiene technology markets.

- November 2025 — Essity acquired Edgewell’s North American feminine care business, adding the Carefree, Stayfree, and Playtex brands to reinforce its position across hygiene and personal care categories.

Conclusion

The alcohol wipes market advances steadily, driven by infection-control mandates, rising consumer hygiene expectations, and expanding commercial disinfection requirements. A 5.2% CAGR over the 2025–2034 forecast period reflects durable structural demand rather than cyclical growth. Both institutional and household channels contribute to balanced revenue expansion across all major global regions.

The synthetic fabric segment and personal-household end-use category anchor market performance with shares of 69.2% and 67.1% respectively. North America maintains regional leadership at 44.2% share, while Asia Pacific accelerates as urbanization and healthcare investment intensify. Supermarkets remain the primary distribution gateway, though online channels grow increasingly influential.

Companies must prioritize sustainable formulation development, skin-safe innovation, and omnichannel distribution strategies to capture emerging demand. Strategic acquisitions and private-label partnerships will intensify competitive pressure across retail and institutional segments. Businesses that align product portfolios with both eco-conscious and clinical-grade requirements are best positioned as the market approaches USD 1021.8 Million by 2034.

Looking for data tailored to your specific market, region, or business need? Request a custom report or consultation — write to us at sales@market.us

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)