Table of Contents

Overview

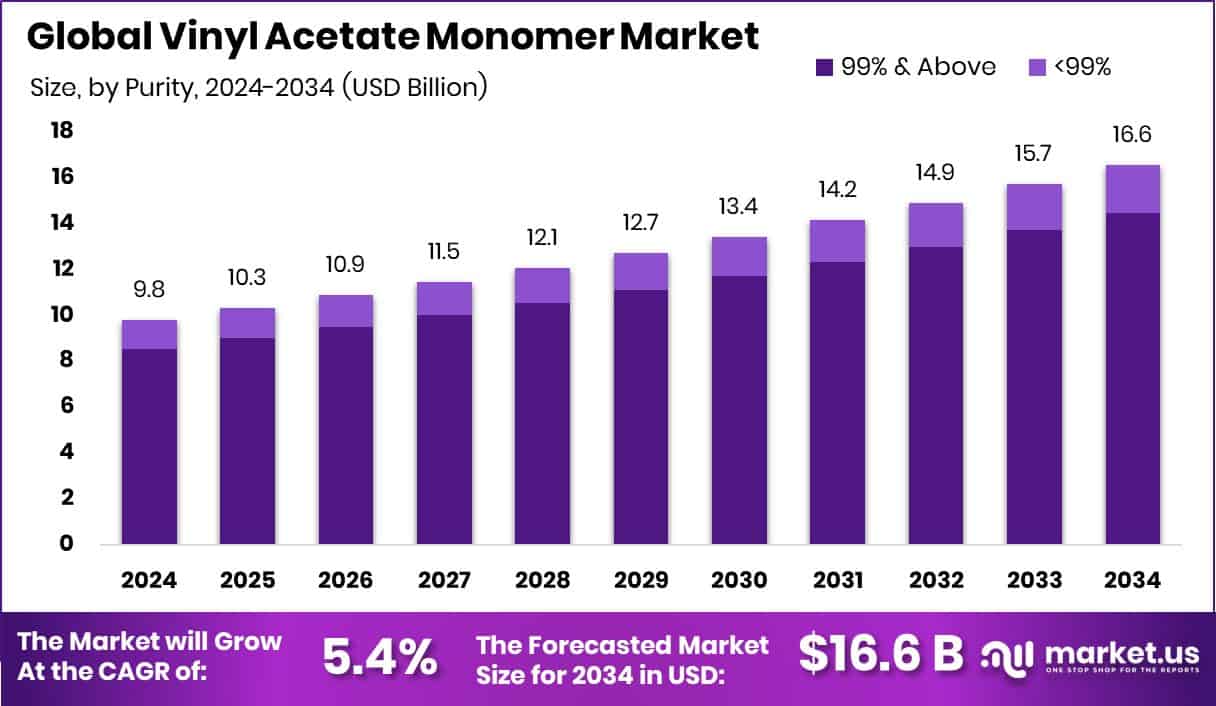

New York, NY – July 25, 2025 – The Global Vinyl Acetate Monomer (VAM) Market is set for steady growth, projected to rise from USD 9.8 billion in 2024 to USD 16.6 billion by 2034, expanding at a CAGR of 5.4%. This growth is driven by increasing demand from key industries like adhesives, paints & coatings, and textiles, where VAM is widely used as a raw material.

The 99% and above purity grade of Vinyl Acetate Monomer (VAM) led the market in 2024, commanding an 87.2% share in the purity segment. Polyvinyl Alcohol (PVOH) dominated the VAM application segment, capturing a 46.8% share of global demand.

PVOH’s widespread use in adhesives, textiles, packaging, and paper processing stems from its excellent film-forming, emulsifying, and adhesive properties, coupled with high water solubility and biodegradability. The Packaging Sector led VAM consumption in 2024, accounting for a 38.7% share in the end-use segment. The demand for flexible, durable packaging solutions in food and beverage, pharmaceuticals, and personal care drives this dominance.

Key Takeaways

- Global Vinyl Acetate Monomer Market is expected to be worth around USD 16.6 billion by 2034, up from USD 9.8 billion in 2024, and grow at a CAGR of 5.4% from 2025 to 2034.

- In the Vinyl Acetate Monomer market, 99% and above purity accounted for 87.2% share.

- Polyvinyl alcohol led the application segment in the Vinyl Acetate Monomer market with 46.8% contribution.

- The packaging industry dominated end-use in the Vinyl Acetate Monomer market, holding a 38.7% market share.

- The North American market value reached approximately USD 3.7 billion during the same year.

How Growth is Impacting the Economy

The VAM market’s growth significantly influences the global economy by fostering job creation and industrial expansion. In construction, VAM-based adhesives and coatings support infrastructure projects, boosting employment in manufacturing and supply chains, particularly in the Asia-Pacific, where urbanization drives demand. The automotive sector benefits from VAM’s use in lightweight, durable adhesives, enhancing fuel efficiency and reducing production costs.

Packaging industry growth, spurred by e-commerce, increases VAM demand for sustainable films, contributing to GDP in emerging markets. However, raw material price volatility, like ethylene and acetic acid, poses challenges, potentially raising costs for manufacturers. Investments in sustainable production technologies mitigate environmental concerns, aligning with global regulations and attracting eco-conscious investments, further stimulating economic activity.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/vinyl-acetate-monomer-market/request-sample/

Strategies for Businesses

Businesses in the VAM market should prioritize innovation by investing in R&D for eco-friendly, low-VOC formulations to meet regulatory demands and consumer preferences. Strategic partnerships with construction and automotive firms ensure stable demand. Expanding production capacities in high-growth regions like Asia-Pacific, as seen with Celanese’s Edmonton facility, enhances market presence. Leveraging cost-effective raw material sourcing, such as shale gas in the U.S., can mitigate price volatility. Additionally, adopting advanced catalytic processes reduces production costs and environmental impact, strengthening competitiveness. Companies should also explore mergers and acquisitions to consolidate market share and enhance supply chain resilience.

Report Scope

| Market Value (2024) | USD 9.8 Billion |

| Forecast Revenue (2034) | USD 16.6 Billion |

| CAGR (2025-2034) | 5.4% |

| Segments Covered | By Purity (99% and Above, <99%), By Application (Polyvinyl Alcohol, Polyvinyl Acetate, Ethylene Vinyl Acetate, Others), By End-use (Packaging, Construction, Textile, Adhesives, Others) |

| Competitive Landscape | Arkema, Celanese Corporation, Chang Chun Group, DCC, Dow Chemical, Exxon Mobil Corporation, Innospec, Japan VAM & Poval Co Ltd, Kuraray Co Ltd, LyondellBasell Industries N.V., Sinopec China Petrochemical Corporation, Sipchem, Solventis, Wacker Chemie AG |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=151907

Key Market Segments

By Purity Analysis

The 99% and above purity grade of Vinyl Acetate Monomer (VAM) led the market in 2024, commanding an 87.2% share in the purity segment. This high-purity VAM is favored for its exceptional quality, reliability, and consistent performance in polymer production, making it the top choice for industries requiring precision and minimal impurities.

Key applications, such as adhesives, coatings, and high-performance films, drive demand due to the need for stable chemical behavior during polymerization. The preference for high-purity VAM is further fueled by manufacturers of water-based adhesives and eco-friendly emulsions, who prioritize regulatory compliance and quality standards.

By Application Analysis

In 2024, Polyvinyl Alcohol (PVOH) dominated the VAM application segment, capturing a 46.8% share of global demand. PVOH’s widespread use in adhesives, textiles, packaging, and paper processing stems from its excellent film-forming, emulsifying, and adhesive properties, coupled with high water solubility and biodegradability.

The shift toward sustainable, water-based materials in packaging and construction bolsters PVOH’s prominence, as it aligns with environmental regulations and enhances product performance. Its versatility in producing specialty films, emulsions, and coatings further solidifies its leadership. With rising demand for eco-friendly and low-toxicity polymers, PVOH remains a cornerstone of the VAM value chain, driven by its reliability and expanding applications across industrial and consumer goods sectors.

By End-Use Analysis

The Packaging Sector led VAM consumption in 2024, accounting for a 38.7% share in the end-use segment. The demand for flexible, durable packaging solutions in food and beverage, pharmaceuticals, and personal care drives this dominance. VAM-based polymers, such as polyvinyl alcohol and ethylene-vinyl acetate, provide strength, flexibility, and superior sealing properties critical for product integrity and extended shelf life.

Consumer demand for lightweight, protective, and sustainable packaging materials, combined with global emphasis on hygiene and convenience, fuels the growth of VAM in innovative packaging formats. As sustainability and performance requirements intensify, VAM’s role in high-performance packaging materials ensures the segment’s continued significance.

Regional Analysis

North America held the largest share of the VAM market in 2024, with a 38.1% share valued at USD 3.7 billion. This leadership is driven by robust demand from well-established industries like packaging, construction, and adhesives, alongside a focus on eco-friendly materials and advanced polymer processing technologies.

Other regions, including Europe, Asia Pacific, the Middle East & Africa, and Latin America, contribute significantly to the global market. Asia Pacific shows strong growth potential due to rapid urbanization and expanding manufacturing capacity. Europe emphasizes eco-compliant materials, while the Middle East & Africa and Latin America see steady growth from local production and consumer goods expansion. North America’s dominance reflects its industrial strength and innovation in VAM applications.

Recent Developments

1. Arkema

- Arkema has been focusing on sustainable VAM production, investing in bio-based alternatives to reduce its carbon footprint. The company expanded its VAM capacity in Asia to meet growing demand in adhesives and coatings. Arkema is also enhancing its emulsion polymers portfolio for eco-friendly applications.

2. Celanese Corporation

- Celanese announced a price increase for VAM due to rising raw material costs. The company is optimizing production efficiency and expanding its acetyl chain business, including VAM derivatives. Celanese is also investing in green chemistry initiatives for sustainable VAM solutions.

3. Chang Chun Group

- Chang Chun Group has been expanding its VAM and EVA copolymers production in China to cater to the booming packaging and solar panel industries. The company is also focusing on high-purity VAM for specialty chemical applications.

4. DCC

- DCC, through its subsidiary Sasol, exited the VAM business in 2023, selling its stake to focus on core energy operations. This shift has impacted regional VAM supply dynamics, creating opportunities for other producers.

5. Dow Chemical

- Dow is innovating in low-carbon VAM production and expanding its derivatives for adhesives and paints. The company is collaborating with partners to enhance recyclable and bio-based materials using VAM. Dow’s investments aim to strengthen its position in North America and Europe.

Conclusion

The VAM market’s robust growth, driven by industrial demand and sustainable innovations, underscores its economic significance. While challenges like raw material volatility persist, strategic investments in eco-friendly technologies and regional expansions offer opportunities for businesses to thrive. As industries like construction and automotive continue to rely on VAM, its role in fostering economic growth and sustainability will strengthen, positioning the market as a vital contributor to global industrial and environmental progress.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)