Table of Contents

Overview

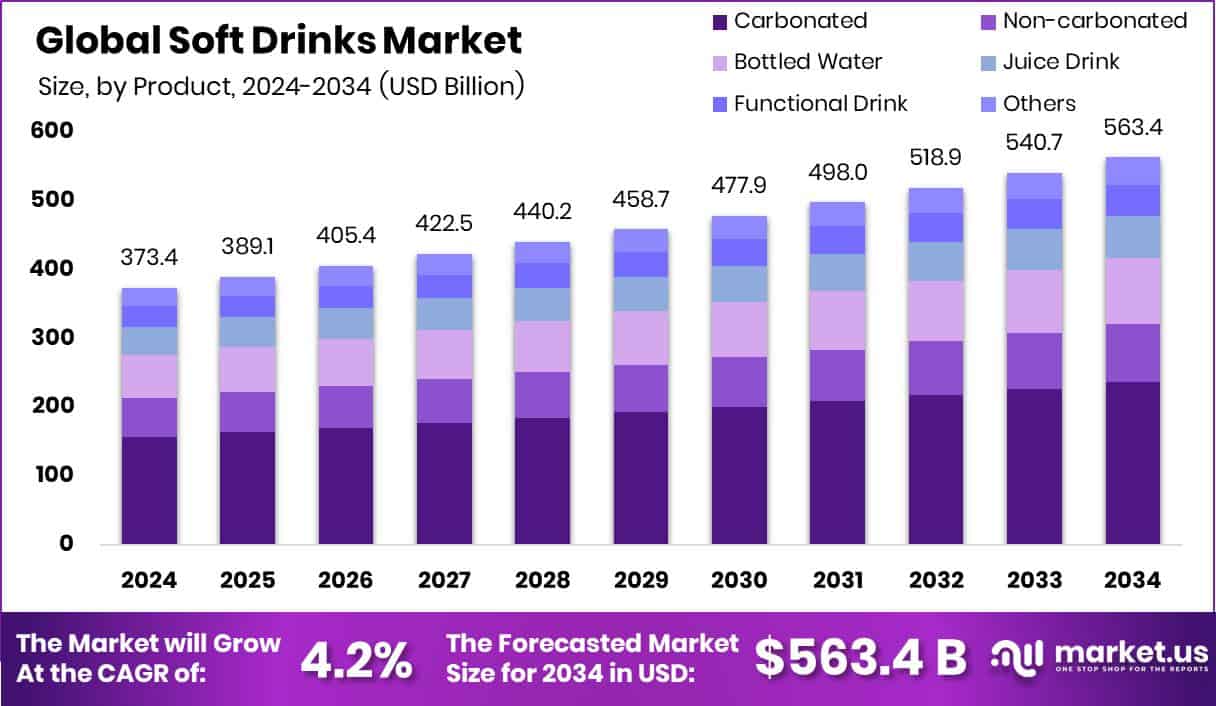

New York, NY – July 03, 2025 – The Global Soft Drinks Market is thriving, driven by strong consumer demand and evolving preferences. Valued at USD 373.4 billion in 2024, the market is projected to reach USD 563.4 billion by 2034, growing at a CAGR of 4.2% from 2025 to 2034. This growth is fueled by urbanization, rising disposable incomes, and changing lifestyles, particularly among younger consumers who seek convenient, ready-to-drink beverages.

In 2024, Carbonated Beverages commanded a leading 42.5% share in the By Product segment of the Soft Drinks Market. This dominance stems from strong consumer demand for fizzy, flavored drinks, particularly in urban areas where fast-paced lifestyles drive the need for quick refreshment. Cola secured a commanding 47.4% share in the By Flavour segment of the Soft Drinks Market.

Its enduring global popularity is driven by a classic taste and strong brand recognition, resonating across generations. Hypermarkets and Supermarkets led the distribution Channel segment of the Soft Drinks Market with a 53.3% share. Their dominance is fueled by the convenience, variety, and competitive pricing these outlets provide.

Key Takeaways

- Global Soft Drinks Market is expected to be worth around USD 563.4 billion by 2034, up from USD 373.4 billion in 2024, and grow at a CAGR of 4.2% from 2025 to 2034.

- Carbonated soft drinks hold a 42.5% share, driven by strong consumer preference and fizzy refreshment.

- Cola dominates the soft drinks market with 47.4%, remaining the top choice across all regions.

- Hypermarkets and supermarkets lead sales with 53.3%, offering a wide product variety and easy accessibility.

- The North American soft drinks market reached a value of USD 143.3 billion.

How Growth is Impacting the Economy

The Soft Drinks Market’s robust growth significantly influences the global economy. Its expansion creates jobs in production, distribution, and retail, particularly in hypermarkets and supermarkets, which account for 53.3% of sales. In North America, the market generated USD 143.3 billion in 2024, boosting local economies through increased consumer spending and tax revenues.

The rise in demand for healthier beverages drives R&D investments, fostering innovation and technological advancements in manufacturing and packaging. However, supply chain disruptions, like those during COVID-19, highlight vulnerabilities, impacting global trade. The market’s growth also supports ancillary industries, such as advertising and logistics, while encouraging sustainable practices, aligning with economic and environmental goals.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/global-soft-drinks-market/request-sample/

Strategies for Businesses

Businesses in the soft drinks market should focus on innovation, sustainability, and targeted marketing. Developing low-sugar, functional, and plant-based beverages aligns with consumer health trends. Adopting eco-friendly packaging, like recyclable or biodegradable materials, enhances brand appeal and meets regulatory demands. Leveraging digital marketing and social media engages younger demographics, while partnerships with fast-food chains and e-commerce platforms expand market reach. Investing in R&D for unique flavors and premium products can differentiate brands in a competitive landscape. Additionally, strategic mergers and acquisitions, as seen with major players like Coca-Cola and PepsiCo, can strengthen market presence and global distribution networks.

Report Scope

| Market Value (2024) | USD 373.4 Billion |

| Forecast Revenue (2034) | USD 563.4 Billion |

| CAGR (2025-2034) | 4.2% |

| Segments Covered | By Product (Carbonated, Non-carbonated, Bottled Water, Juice Drink, Functional Drink, Others), By Flavour (Cola, Citrus, Others), By Distribution Channel (Hypermarkets and Supermarkets, Convenience Store, Online, Others) |

| Competitive Landscape | Pepsico, Inc., Nestlé, The Coca-Cola Company, Keurig Dr Pepper Inc (KDP), Red Bull GmbH, Unilever PLC, Monster Energy Company, Appalachian Brewing Company, ITO EN INC., AriZona Beverages USA LLC, Dr Pepper Snapple Group, ITO EN INC., AriZona Beverages USA LLC, Appalachian Brewing Company, Asahi Group Holdings |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=150691

Key Market Segments

By Product Analysis

- In 2024, Carbonated Beverages commanded a leading 42.5% share in the By Product segment of the Soft Drinks Market. This dominance stems from strong consumer demand for fizzy, flavored drinks, particularly in urban areas where fast-paced lifestyles drive the need for quick refreshment. Carbonated soft drinks remain a top choice for social events, dining establishments, and convenience stores, bolstered by their high visibility and widespread availability.

By Flavour Analysis

- In 2024, Cola secured a commanding 47.4% share in the By Flavour segment of the Soft Drinks Market. Its enduring global popularity is driven by a classic taste and strong brand recognition, resonating across generations. Cola remains a preferred choice for both individual consumption and large social gatherings, maintaining its cultural relevance. The availability of cola in various packaging formats, from single cans to family-sized bottles, caters to diverse consumer needs, while its versatility as a food pairing drives repeat purchases, cementing its dominance in the flavor segment.

By Distribution Channel Analysis

- In 2024, Hypermarkets and Supermarkets led the By Distribution Channel segment of the Soft Drinks Market with a 53.3% share. Their dominance is fueled by the convenience, variety, and competitive pricing these outlets provide. As one-stop shopping destinations, they offer a wide array of soft drink brands and flavors, often enhanced by discounts and bundled promotions.

- Spacious store layouts and visible soft drink sections drive higher footfall and purchase frequency. Widely accessible in urban and semi-urban areas, these retailers are trusted for product freshness and authenticity. Additionally, bulk purchasing for households and events further boosts sales volume through this channel, reinforcing its market leadership.

Regional Analysis

- North America led the global Soft Drinks Market, capturing 38.3% of the share, valued at USD 143.3 billion. High per capita consumption, robust retail infrastructure, and steady demand for carbonated and flavored drinks in the U.S. and Canada drive this dominance. Convenience, brand loyalty, and lifestyle preferences fuel sales in urban and suburban areas.

- Europe plays a key role in the global market, with strong consumer awareness and a growing preference for sugar-free and flavored beverages, though specific figures are unavailable. In Asia Pacific, increasing disposable incomes, a youthful population, and rapid urbanization are boosting demand for packaged soft drinks.

- The Middle East & Africa region shows consistent growth, supported by expanding retail networks and hot climates driving year-round consumption. Latin America, while smaller, sees gradual growth in soft drink sales, fueled by evolving lifestyles and the rising popularity of flavored beverages.

Recent Developments

1. PepsiCo, Inc.

- PepsiCo acquired Poppi, a prebiotic soda brand, aiming to strengthen its position in the functional drinks market. Poppi’s year-over-year sales growth and share of the U.S. soft drink market highlight its appeal among health-conscious consumers. PepsiCo continues to diversify its portfolio, focusing on healthier, low-sugar options to align with shifting consumer preferences.

2. Nestlé

- Nestlé, a major player in bottled water and non-carbonated beverages, continues to compete with Coca-Cola in the bottled water segment with brands like Perrier and S. Pellegrino. Nestlé has focused on expanding its premium water offerings, emphasizing natural and flavored varieties to meet growing demand for healthier hydration options.

3. The Coca-Cola Company

- Coca-Cola remains the global soft drink leader with a U.S. market share. In February 2025, it launched Simply Pop, a prebiotic soda with 6 grams of fiber and no added sugar, targeting the growing functional beverage market. Available in five fruit-forward flavors, it caters to health-conscious consumers.

4. Keurig Dr Pepper Inc (KDP)

- Keurig Dr Pepper (KDP) overtook Pepsi as the No. 2 U.S. soda brand in 2023, driven by Dr Pepper’s brand value increase. In October 2024, KDP acquired GHOST Energy, a fast-growing energy drink brand, to bolster its presence in the energy drink market. KDP’s diverse portfolio, including Dr Pepper, 7Up, and Snapple, benefits from strong distribution networks.

5. Red Bull GmbH

- Red Bull, a leader in the energy drink segment. In 2025, the company continues to focus on its high-caffeine energy drinks, targeting extreme sports enthusiasts and younger demographics. Red Bull’s distinct flavor profile and bold marketing keep it competitive, though it doesn’t challenge Coca-Cola or PepsiCo in traditional sodas.

Conclusion

The Soft Drinks Market, poised for steady growth, reflects dynamic consumer trends and economic contributions. Businesses must adapt through health-focused products and eco-friendly practices to stay competitive. As consumer preferences evolve, the market’s ability to innovate and expand into emerging regions like Asia-Pacific ensures its resilience and economic significance, promising a vibrant future for stakeholders and the global beverage industry.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)