Table of Contents

Overview

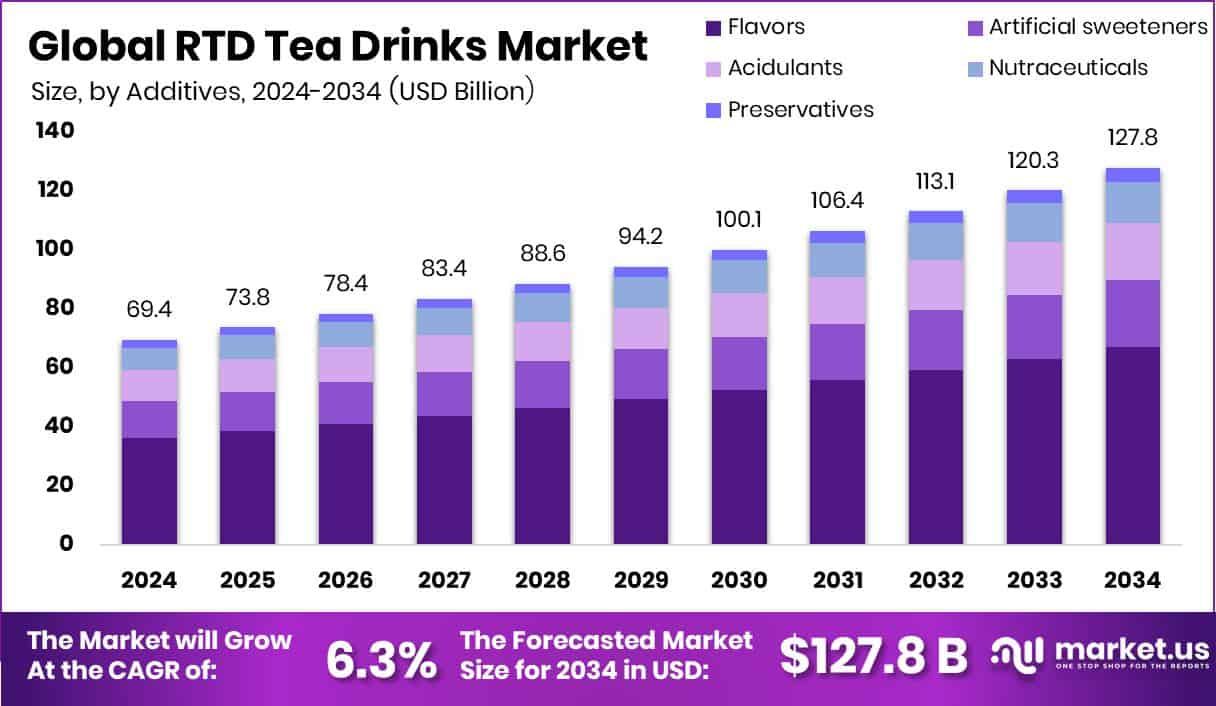

New York, NY – May 29, 2025 – The Global RTD Tea Drinks Market is booming, driven by rising health consciousness and demand for convenient beverages. With an expected jump from USD 69.4 billion in 2024 to USD 127.8 billion by 2034, the market is growing at a strong 6.3% CAGR.

Flavors held a commanding 52.4% share of the RTD Tea Drinks market in 2024, driven by growing consumer demand for diverse and exotic tea profiles, especially among younger consumers. Black Tea captured a leading 45.7% share of the RTD Tea Drinks market in 2024, driven by its widespread popularity as a traditional and refreshing choice, particularly in high tea-consuming regions.

PET bottles secured a 34.7% share of the RTD Tea Drinks market in 2024, favored for their lightweight, portable, and cost-effective attributes, ideal for on-the-go consumption. Off-trade channels dominated with a 71.9% share in 2024, driven by the widespread presence of retail outlets, supermarkets, and convenience stores.

US Tariff Impact on RTD Tea Drinks Market

The U.S. Tea Industry is facing challenges as President Trump’s tariff policies, initiated in February 2025, continue to evolve. A 10% universal tariff on all countries is currently in place, but a 90-day pause on additional reciprocal tariffs, effective from April 9, 2025, was introduced to allow the White House negotiations with other nations.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/global-rtd-tea-drinks-market/request-sample/

China, however, is an exception, facing a 145% reciprocal tariff imposed on April 9 following days of escalating trade tensions, with no pause applied. Observatory of Economic Complexity (OEC), the U.S. imported USD 550 million worth of tea in 2024, primarily from Japan (USD 107M), India (USD 65.1M), Argentina (USD 57.9M), China (USD 55.5M), and Sri Lanka (USD 46.7M). Imports rose 14.7% year-on-year in January 2025, driven by increases from India (+USD 3.3M, 86.2%) and China (+USD 1.38M, 25.2%).

The US Census Bureau, via First Tea, notes that one-third of 2024 U.S. instant tea imports by value came from China (USD 21.5M), with China’s import volume surging over 44% from 2023 to 2024. As the second-largest global tea importer, the U.S. relies heavily on imports since domestic tea production remains minimal, making the industry particularly vulnerable to these tariff fluctuations, as World Tea News explores through discussions with industry stakeholders.

Key Takeaways

- Global RTD Tea Drinks Market is expected to be worth around USD 127.8 billion by 2034, up from USD 69.4 billion in 2024, and grow at a CAGR of 6.3% from 2025 to 2034.

- Flavors lead the RTD Tea Drinks Market, capturing a 52.4% share, driving consumer demand.

- Black Tea dominates the Product Types segment with a 45.7% share, reflecting consumer preferences.

- PET bottles hold a 34.7% share in packaging, emphasizing convenience and portability for consumers.

- Off-trade channels command 71.9% of the RTD Tea Drinks Market, highlighting retail dominance and accessibility.

- The USD 30.4 Bn RTD Tea Drinks market in North America dominated with 43.9%.

Report Scope

| Market Value (2024) | USD 69.4 Billion |

| Forecast Revenue (2034) | USD 127.8 Billion |

| CAGR (2025-2034) | 6.3% |

| Segments Covered | By Additives (Flavors, Artificial sweeteners, Acidulants, Nutraceuticals, Preservatives, Others), By Product Types (Black Tea, Herbal, Green tea, Others), By Packaging (Glass Bottle, Canned, Pet bottle, Fountain/Aseptic, Others), By Distribution Channel (Off-trade (Independent retailers, Supermarkets/Hypermarkets, Convenience stores, Others), On-trade (Food Service, Vending, Others)) |

| Competitive Landscape | Ajinomoto General Foods Inc., Asahi Group Holdings Ltd, Dr Pepper Snapple Group, Dunkin’ Brands Group, Hangzhou Wahaha Group, Ito En Ltd, Kirin Holdings Co. Ltd, Lotte Chilsung Beverage Co. Ltd, Monster Beverage Company, Nestle S.A., PepsiCo Inc., Pokka Group, Starbucks Corporation, Suntory Beverage & Food Ltd |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=148258

Key Market Segments

Flavors Analysis

- Flavors held a commanding 52.4% share of the RTD Tea Drinks market in 2024, driven by growing consumer demand for diverse and exotic tea profiles, especially among younger consumers. Manufacturers have responded by introducing innovative flavor combinations, boosting product appeal, and market reach.

- The rise in flavored RTD tea demand is fueled by expanded urban distribution networks, where convenient, ready-to-drink options thrive in both retail and on-trade channels. Limited-edition and seasonal flavors have further attracted consumers, driving market growth. Additionally, the use of natural and botanical extracts in flavored RTD teas aligns with the increasing preference for health-conscious, functional beverages, strengthening the segment’s dominance.

Product Types Analysis

- Black Tea captured a leading 45.7% share of the RTD Tea Drinks market in 2024, driven by its widespread popularity as a traditional and refreshing choice, particularly in high tea-consuming regions. The growing demand for flavored black tea variants has diversified offerings, catering to varied consumer tastes.

- Black tea’s perceived health benefits, including antioxidant properties and digestive support, have resonated with health-conscious consumers, reinforcing its market position. Manufacturers have emphasized premium black tea extracts to enhance product quality and brand differentiation. Available in both hot and cold formats, black tea appeals to diverse preferences, while effective marketing as a convenient, revitalizing beverage further drives its strong market penetration among urban consumers.

Packaging Analysis

- PET bottles secured a 34.7% share of the RTD Tea Drinks market in 2024, favored for their lightweight, portable, and cost-effective attributes, ideal for on-the-go consumption. The shift toward sustainability has prompted manufacturers to adopt recyclable PET bottles, meeting consumer demand for eco-friendly packaging.

- The durability and transparency of PET bottles enhance product visibility and brand appeal. Growth in the retail sector, particularly in emerging markets, has increased the availability of PET-packaged RTD teas, boosting market penetration. Multi-serve and family-sized PET bottles have also gained popularity among budget-conscious consumers, further solidifying the segment’s leading position in the market.

Distribution Channel Analysis

- Off-trade channels dominated with a 71.9% share in 2024, driven by the widespread presence of retail outlets, supermarkets, and convenience stores. The ease of purchasing RTD tea during routine grocery shopping has made off-trade the preferred channel for consumers. Bulk purchasing trends in hypermarkets and supermarkets, particularly for PET bottles and multi-packs, have further boosted demand.

- Seasonal promotions, discounts, and strategic placement in beverage aisles and chilled sections have enhanced product visibility and consumer engagement. The growing demand for low-calorie, flavored tea options has also led retailers to expand their RTD tea offerings, aligning with health-conscious trends and reinforcing off-trade dominance through accessibility and consumer-focused strategies.

Regional Analysis

- North America led the RTD Tea Drinks Market in 2024, securing a dominant 43.9% share, valued at USD 30.4 billion. This strong position is driven by robust consumer demand for convenient, refreshing beverages, supported by extensive retail networks and widespread product availability. The popularity of flavored and functional RTD teas, particularly in the United States and Canada, has significantly boosted market growth.

- Europe follows, with growing consumer preference for organic and health-focused RTD tea products. In the Asia Pacific, rising urbanization and shifting preferences toward ready-to-drink beverages are driving increased market penetration. The Middle East & Africa and Latin America, though smaller markets, are seeing steady growth, fueled by expanding retail infrastructure and the rising appeal of cold beverages in warm climates.

Top Use Cases

- On-the-Go Convenience: RTD teas are perfect for busy urban consumers seeking quick hydration. Packaged in portable PET bottles or cans, they fit fast-paced lifestyles, offering refreshing options like iced green or black tea during commutes, workouts, or breaks, appealing to millennials and Gen Z.

- Health-Conscious Choice: Health-focused consumers choose RTD teas for their low-sugar, antioxidant-rich profiles. Infused with natural ingredients like herbal extracts or probiotics, these beverages support wellness goals, such as improved digestion or immunity, attracting those prioritizing functional drinks.

- Flavor Exploration: RTD teas cater to adventurous palates with exotic flavors like peach, mango, or matcha. Seasonal and limited-edition blends draw younger consumers, enhancing brand appeal and encouraging trial through innovative taste profiles in retail and online channels.

- Sustainable Packaging Appeal: Eco-conscious consumers prefer RTD teas in recyclable PET bottles or cans. Brands adopting sustainable packaging align with environmental values, boosting loyalty among younger demographics and expanding market reach in eco-aware regions like North America and Europe.

- Social and Recreational Use: RTD teas are popular at social gatherings or as leisure drinks. Flavored options like bubble tea or kombucha enhance casual outings, appealing to Gen Z for their trendy, Instagram-worthy appeal, driving sales in cafes and convenience stores.

Recent Developments

1. Ajinomoto General Foods Inc

- Ajinomoto has expanded its “Wonda” brand RTD tea line in Japan, introducing new flavors like “Morning Shot Tea” with added caffeine for energy. The company focuses on health-oriented tea beverages, leveraging natural ingredients and reduced sugar content. They have also invested in sustainable packaging to align with environmental goals.

2. Asahi Group Holdings Ltd

- Asahi launched “Kuro Oolong Tea”, a dark-roasted oolong tea under its “Kuro” (Black) series, targeting health-conscious consumers. The company is also expanding RTD tea exports to Southeast Asia, emphasizing zero-sugar and antioxidant-rich variants. Asahi is incorporating recycled PET bottles for eco-friendliness.

3. Keurig Dr Pepper (formerly Dr Pepper Snapple Group)

- Keurig Dr Pepper introduced “Core Hydration + Tea”, a fusion of RTD tea with electrolytes. The company also expanded “Snapple Zero Sugar Tea” with new flavors like Peach and Raspberry. They are leveraging e-commerce and convenience store partnerships for wider distribution.

4. Inspire Brands (formerly Dunkin’ Brands Group)

- Dunkin’ (under Inspire Brands) launched “Dunkin’ Iced Tea” in RTD formats, including Sweet Tea and Unsweetened Black Tea, in retail stores. The brand focuses on convenience and quick consumption, partnering with supermarkets and gas stations for broader reach.

5. Hangzhou Wahaha Group

- Wahaha introduced “Fruit + Tea” RTD blends, combining traditional Chinese tea with fruit juices. They expanded distribution in China and Southeast Asia, emphasizing natural ingredients and no artificial additives. Wahaha is also investing in smart manufacturing for efficient production.

Conclusion

The RTD Tea Drinks market thrives due to strong consumer demand for convenient, health-focused, and flavorful beverages. North America leads with a 43.9% share, driven by robust retail networks and flavored tea popularity. Innovations in sustainable packaging, diverse flavors, and functional ingredients continue to fuel growth across regions, catering to evolving consumer preferences and ensuring sustained market expansion.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)