Table of Contents

Overview

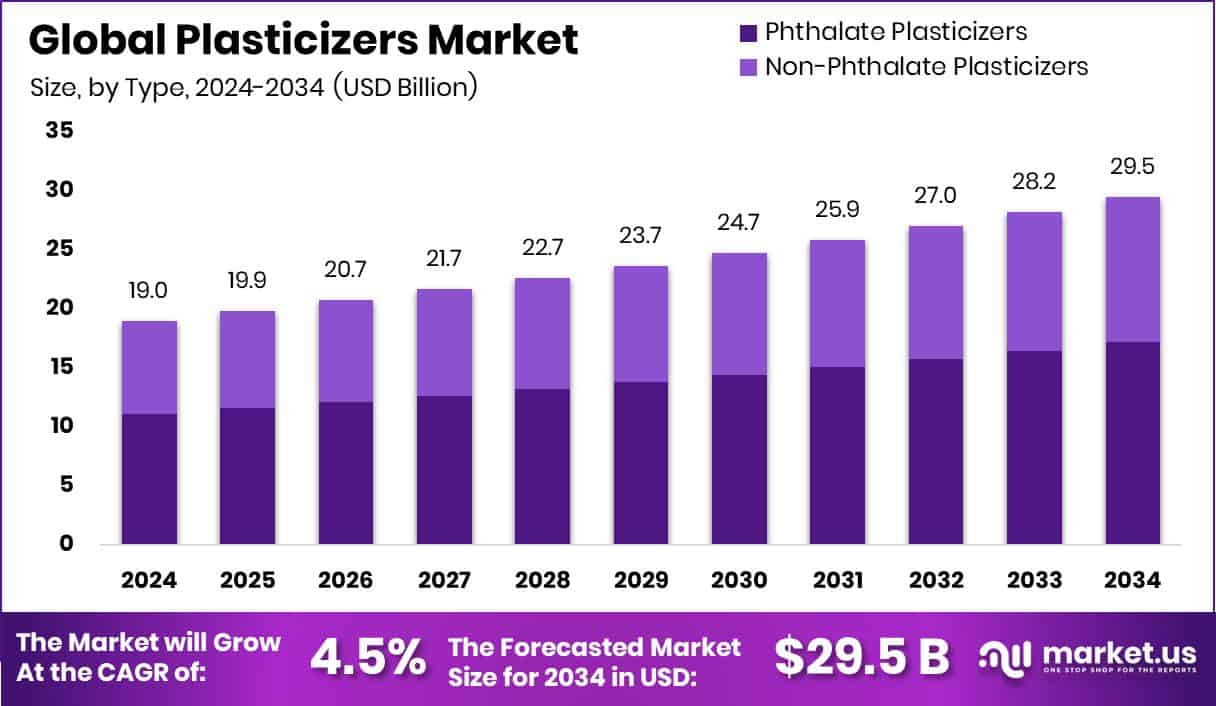

New York, NY – May 23, 2025 – The Global Plasticizers Market is set for steady growth, projected to reach USD 29.5 billion by 2034, up from USD 19.0 billion in 2024, with a 4.5% CAGR from 2025 to 2034.

Phthalate Plasticizers led the Plasticizers Market in 2024, capturing a 58.3% share globally. Their dominance is driven by extensive use in flexible PVC applications, including cables, flooring, and synthetic leather. Flooring and Wall Coverings accounted for 28.4% of the Plasticizers Market demand. This significant share reflects the high reliance on flexible PVC in residential, commercial, and industrial construction. The Building and Construction sector dominated the Plasticizers Market in 2024, holding a 32.2% share of end-use consumption.

US Tariff Impact on Plasticizers Market

New tariffs on imported polyethylene (PE), polypropylene (PP), and polyvinyl chloride (PVC) will raise costs for U.S. manufacturers supplementing domestic production, with a 10% tariff on plastic resin imports from China and a 15% tariff on petrochemical feedstocks from the Middle East. This immediate cost increase for internationally sourced raw materials is driving manufacturers to focus on domestic sourcing or alternative suppliers.

➤ Get More Detailed Insights about US Tariff Impact @ – https://market.us/report/global-plasticizers-market/request-sample/

According to an American Chemistry Council report, manufacturers dependent on imports could face cost increases of 12-20%, depending on supply chain adjustments. Plastics disclosed that 60 plastic products exported from the EU to the U.S. could face retaliatory tariffs as a countermeasure to the 25% tariffs on steel and aluminum announced by Trump on March 12, 2025. The association projects that these EU tariffs could impact USD 5.9 billion in U.S. exports.

Key Takeaways

- Global Plasticizers Market is expected to be worth around USD 29.5 billion by 2034, up from USD 19.0 billion in 2024, and grow at a CAGR of 4.5% from 2025 to 2034.

- Phthalate plasticizers dominate the plasticizers market, capturing a strong 58.3% share due to versatile applications.

- Flooring and wall covering applications account for a 28.4% share, driven by rising infrastructure and renovation activities.

- The building and construction sector leads the plasticizers market with a 32.2% share, supporting large-scale urbanization projects worldwide.

- Asia-Pacific’s Plasticizers Market reached USD 8.6 Bn, capturing 45.3% global market share.

Report Scope

| Market Value (2024) | USD 19.0 Billion |

| Forecast Revenue (2034) | USD 29.5 Billion |

| CAGR (2025-2034) | 4.5% |

| Segments Covered | By Type (Phthalate Plasticizers (Diisodecyl phthalate (DIDP), Diisononyl phthalate (DINP), Diisobutyl phthalate (DIBP), Dipropyl Heptyl phthalate (DPHP), Dioctyl phthalate (DOP), Others), Non-Phthalate Plasticizers (Adipates, Trimellitates, Epoxies, Benzoates, Terephthalates, Others)), By Application (Flooring and Wall Covering, Wire and Cable, Coatings, Toys, Footwear, Film and Sheet, Medical Devices, Others), By End-use (Building and Construction, Automotive and Transportation, Electrical and Electronics, Consumer Goods, Textile, Packaging, Healthcare, Others) |

| Competitive Landscape | BASF SE, ExxonMobil, Evonik Industries AG, UPC Technology Corporation, Eastman Chemical Company, LG Chem, Aekyung Chemical Co., Ltd, Lanxess AG, Avient Corporation, Shandong Hongxin Chemical Co., Ltd., Nan Ya Plastics, DIC Corporation, Kao Corporation, KLJ Group, Mitsubishi Chemical Group Corporation, Other Key Players |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=147131

Key Market Segments

By Type Analysis

- Phthalate Plasticizers led the Plasticizers Market in 2024, capturing a 58.3% share globally. Their dominance is driven by extensive use in flexible PVC applications, including cables, flooring, and synthetic leather. Favored for their cost-effectiveness, polymer compatibility, and superior attributes like flexibility, durability, and low volatility, phthalates remain integral to industries such as construction and automotive, despite growing environmental concerns. In emerging economies with booming infrastructure and less stringent regulations, demand for phthalates remains robust.

By Application Analysis

- In 2024, Flooring and Wall Coverings accounted for 28.4% of the Plasticizers Market demand. This significant share reflects the high reliance on flexible PVC in residential, commercial, and industrial construction. Plasticizers enhance the flexibility, durability, and longevity of these materials, making them ideal for high-traffic areas and diverse environmental conditions. Rising urbanization and renovation activities, particularly in Asia-Pacific and the Middle East, drive demand for visually appealing, resilient flooring and wall solutions.

By End-use Analysis

- The Building and Construction sector dominated the Plasticizers Market in 2024, holding a 32.2% share of end-use consumption. Plasticizers are vital in construction materials like pipes, cables, flooring, roofing membranes, and wall coverings, enhancing flexibility, strength, and weather resistance in PVC products. Rapid urbanization, investments in smart cities, and demand for affordable housing have significantly increased plasticizer use in this sector.

Regional Analysis

- Asia-Pacific dominated the Plasticizers Market, securing a 45.3% share valued at USD 8.6 billion. This leadership stems from rapid industrialization, booming construction, and expanding automotive production in countries like China, India, and Southeast Asia. The region’s high demand for flexible PVC in infrastructure and consumer goods significantly drives plasticizer consumption.

- North America exhibited steady growth, fueled by strong demand for automotive interiors and renovation projects. Europe held a notable market presence, supported by sustainability efforts and increasing use of bio-based plasticizers in packaging and construction. The Middle East & Africa saw moderate growth, propelled by infrastructure development and urban expansion in nations like Saudi Arabia and the UAE. Latin America maintained a stable market, driven by construction activities in Brazil and Mexico.

Top Use Cases

- Flexible PVC for Construction: Plasticizers make PVC flexible for construction materials like pipes, cables, and flooring. They enhance durability and weather resistance, ideal for modern buildings. High demand in Asia-Pacific, especially China and India, drives their use in infrastructure projects, ensuring cost-effective, long-lasting solutions for urban development.

- Automotive Interiors: Plasticizers are used in car interiors for dashboards, seats, and upholstery. They provide flexibility and durability to PVC components, meeting automotive performance standards. North America and Asia-Pacific see strong demand due to growing vehicle production and consumer preference for comfortable, stylish interiors.

- Flooring and Wall Coverings: Plasticizers improve PVC flexibility in flooring and wall coverings, making them resilient for high-traffic areas. Their use in residential and commercial spaces, especially in Asia-Pacific and the Middle East, supports aesthetic and durable designs, fueled by urbanization and renovation trends.

- Packaging Materials: Plasticizers are key in flexible packaging, like food wraps and containers. They ensure PVC is soft, durable, and safe for consumer goods. Europe’s shift to bio-based plasticizers boosts their use in sustainable packaging, meeting regulatory and consumer demands for eco-friendly solutions.

- Medical Devices: Plasticizers are used in medical tubing, bags, and IV lines, making PVC flexible and safe for healthcare. Their biocompatibility ensures patient safety, with growing demand in North America and Europe for high-quality medical equipment in hospitals and clinics.

Recent Developments

1. BASF SE

- BASF has been focusing on sustainable plasticizers, expanding its Hexamoll DINCH range, a non-phthalate alternative widely used in food packaging and medical devices. The company is investing in R&D to enhance eco-friendly solutions, aligning with global regulatory trends. BASF also partnered with manufacturers to improve PVC applications in automotive and construction.

2. ExxonMobil

- ExxonMobil introduced Jayflex 218 plasticizer, designed for high-performance PVC applications like wires and flooring. The company emphasizes low volatility and durability, catering to the automotive and construction sectors. ExxonMobil is also optimizing supply chains to meet rising Asian demand.

3. Evonik Industries AG

- Evonik launched VESTINOL 9, a next-gen non-phthalate plasticizer for sensitive applications like toys and healthcare. The company is expanding production capacity in Asia to support growing demand. Evonik also focuses on bio-based plasticizers to meet sustainability goals.

4. UPC Technology Corporation

- UPC Technology is strengthening its position in Asia by increasing DOP (Dioctyl Phthalate) production. The company is investing in new facilities to meet regional PVC demand, particularly in China and Southeast Asia. UPC also explores eco-friendly alternatives to comply with regulations.

5. Eastman Chemical Company

- Eastman introduced Eastman 168, a non-phthalate plasticizer for food-contact materials and automotive interiors. The company is expanding its Tritan copolyester-based plasticizers, targeting packaging and consumer goods. Eastman also emphasizes circular economy initiatives.

Conclusion

The Plasticizers Market thrives due to strong demand in construction, automotive, and packaging, with Asia-Pacific leading at a 45.3% share. Phthalates dominate, but bio-based alternatives are gaining traction due to environmental concerns. Rapid urbanization, infrastructure growth, and sustainable innovations will drive future expansion, ensuring plasticizers remain vital for flexible, durable, and cost-effective materials across industries.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)