Table of Contents

Overview

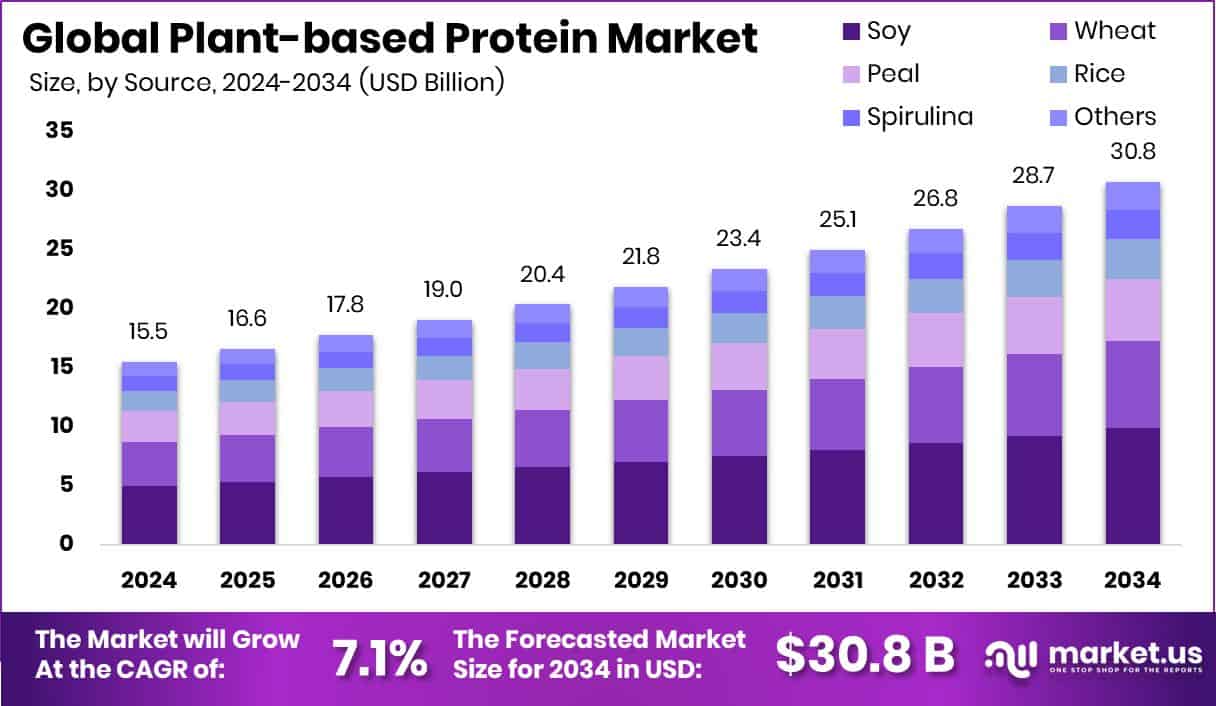

New York, NY – June 06, 2025 – The Global Plant-Based Protein Market is experiencing rapid growth, driven by increasing consumer demand for sustainable and healthy food alternatives. Valued at USD 15.5 billion in 2024, the market is projected to reach USD 30.8 billion by 2034, expanding at a CAGR of 7.1% from 2025 to 2034.

In 2024, Soy led the By Source segment of the Plant-based Protein Market, capturing a 32.2% share. Its dominance stems from soy’s robust nutritional profile, offering a complete amino acid spectrum and high digestibility, making it a top choice for plant-based protein product manufacturers. Isolates dominated the By Form segment of the Plant-based Protein Market with a 48.4% share.

Their high protein content, often exceeding 90%, makes them ideal for protein-enriched food and beverage formulations. Conventional plant-based proteins held an 82.3% share in the By Nature segment of the Plant-based Protein Market. Their dominance is driven by widespread availability, cost-effectiveness, and a well-established supply chain. Functional Foods led the By Application segment of the Plant-based Protein Market with a 35.7% share.

Key Takeaways

- Global Plant-based Protein Market is expected to be worth around USD 30.8 billion by 2034, up from USD 15.5 billion in 2024, and grow at a CAGR of 7.1% from 2025 to 2034.

- In the Plant-based Protein Market, soy accounted for a 32.2% share due to its protein-rich profile.

- Isolates held the largest share at 48.4%, widely used in protein powders and fortified beverages.

- Conventional sources dominated with an 82.3% share, driven by established farming and lower production costs.

- Functional foods captured a 35.7% share, as health-conscious consumers prefer nutrition-packed meals and snacks.

- Plant-based protein demand surged in North America, reaching USD 7.1 billion in value.

How Growth is Impacting the Economy

- The Plant-Based Protein Market’s growth significantly impacts the global economy. It creates jobs in agriculture, manufacturing, and R&D, particularly in regions like North America and Europe. Investments in production facilities stimulate local economies. The shift to plant-based diets reduces environmental costs from livestock farming, lowering greenhouse gas emissions and resource use.

- This supports sustainable economic models, attracting government and private funding. However, challenges like high production costs and raw material price fluctuations can strain supply chains. Overall, the market’s expansion fosters innovation, employment, and sustainability, reshaping food industry economics.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/plant-based-protein-market/request-sample/

Strategies for Businesses

- Businesses can capitalize on the plant-based protein market by investing in R&D to innovate products like textured pea proteins for meat substitutes. Emphasizing clean-label, organic options and using microencapsulation to improve taste can attract health-conscious consumers. Strategic partnerships, such as Beyond Meat’s European expansion, enhance market reach.

- Leveraging eCommerce and retail collaborations ensures accessibility. Highlighting nutritional benefits, like high amino acid content, and obtaining certifications can build consumer trust. Sustainable sourcing and transparent supply chains address environmental concerns, while targeting emerging markets like South Asia, with its growing vegan population, offers untapped growth potential.

Report Scope

| Market Value (2024) | USD 15.5 Billion |

| Forecast Revenue (2034) | USD 30.8 Billion |

| CAGR (2025-2034) | 7.1% |

| Segments Covered | By Source (Soy, Wheat, Peal, Rice, Spirulina, Others), By Form (Isolates, Concentrates, Hydrolysates), By Nature (Organic, Conventional), By Application (Functional Foods, Snacks and Cereals, Dairy Alternatives, Bakery and Confectionery, Animal Feed, Sports Nutrition, Others) |

| Competitive Landscape | Tate & Lyle PLC, ADM, Ingredion, Glanbia plc, AGT Food and Ingredients, PURIS, Kerry Group PLC, Cargill Incorporated, Roquette Frères, Burcon NutraScience Corporation, COSUCRA, DSM Firmenich, International Flavors & Fragrances Inc., Wilmar International Ltd., Emsland Group |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=149082

Key Market Segments

By Source Analysis

- In 2024, Soy led the By Source segment of the Plant-based Protein Market, capturing a 32.2% share. Its dominance stems from soy’s robust nutritional profile, offering a complete amino acid spectrum and high digestibility, making it a top choice for plant-based protein product manufacturers.

- Soy’s widespread availability and versatility in applications like protein bars, meat substitutes, and beverages bolster its market position. Its consistent demand in functional foods, supplements, and dietary plans is driven by consumer familiarity and its cost-effectiveness compared to other plant sources. This affordability enhances its appeal in price-sensitive regions, while established soy processing infrastructure globally, particularly in vegetarian and vegan diets, sustains its market leadership.

By Form Analysis

- In 2024, Isolates dominated the By Form segment of the Plant-based Protein Market with a 48.4% share. Their high protein content, often exceeding 90%, makes them ideal for protein-enriched food and beverage formulations. Isolates’ neutral flavor, high digestibility, and excellent solubility appeal to health-conscious consumers, athletes, and manufacturers. Their widespread use in functional foods, driven by clean-label and high-protein trends, supports their market leadership.

- Isolates excel in applications like protein shakes, bars, dairy alternatives, and meal replacements due to their ability to replicate animal-based protein functionality. The growing popularity of plant-based diets and the convenience of isolates in ready-to-mix or ready-to-drink formats further fuel their dominance. Manufacturers continue to refine extraction technologies to enhance protein purity, meeting evolving dietary demands.

By Nature Analysis

- In 2024, Conventional plant-based proteins held an 82.3% share in the By Nature segment of the Plant-based Protein Market. Their dominance is driven by widespread availability, cost-effectiveness, and a well-established supply chain. Conventional sources like soy, peas, and wheat benefit from large-scale cultivation, ensuring a consistent supply and competitive pricing, making them ideal for mass-market food and beverage applications.

- Their versatility, stability in large-scale processing, and strong consumer acceptance in products like meat alternatives, protein powders, and dairy-free beverages reinforce their market position. Unlike organic options, conventional proteins face fewer regulatory hurdles and offer faster production cycles, enhancing their commercial viability. While organic proteins gain traction in niche markets, conventional variants remain the preferred choice for affordability and familiarity, particularly in emerging economies.

By Application Analysis

- In 2024, Functional Foods led the By Application segment of the Plant-based Protein Market with a 35.7% share. This reflects a consumer shift toward nutrition-focused diets, where functional foods like protein bars, meal replacement drinks, and dairy alternatives deliver both health benefits and taste. These products cater to diverse groups, including fitness enthusiasts, older adults, and those adopting plant-based diets, supporting muscle health, weight management, and overall wellness.

- The integration of high-protein ingredients like isolates aligns with the demand for clean-label, high-protein products. Functional foods’ convenient formats suit busy lifestyles, while widespread retail availability and ongoing product innovation drive their market leadership. As health-conscious eating grows, functional foods are poised to maintain their dominance.

Regional Analysis

- In 2024, North America dominated the Plant-based Protein Market, holding a 46.3% share and generating USD 7.1 billion in revenue. This leadership is fueled by heightened health awareness, growing vegan and flexitarian lifestyles, and widespread product availability in retail and foodservice channels. Europe saw steady growth due to demand for sustainable protein sources and clean-label products.

- The Asia Pacific region showed significant interest, driven by urbanization and changing dietary habits in countries like India, China, and Japan. Latin America and the Middle East & Africa are gradually adopting plant-based proteins, supported by awareness campaigns and global dietary trends, though their market penetration remains lower. North America’s dominance is reinforced by continued investments in product innovation and expanded plant-based offerings in supermarkets and online platforms, solidifying its position as the leading regional market.

Recent Developments

1. Tate & Lyle PLC

- Tate & Lyle has expanded its plant-based protein portfolio by launching Tate & Lyle Protex, a textured pea protein for meat alternatives. The company is focusing on improving texture and nutrition in plant-based foods. Collaborations with food tech startups aim to enhance clean-label solutions. Tate & Lyle is also investing in R&D to optimize protein extraction from pulses.

2. ADM (Archer Daniels Midland)

- ADM has introduced ProFam 580, a pea protein isolate for dairy-free beverages and snacks. The company is expanding its plant-based protein production in Europe and partnering with food brands to develop sustainable alternatives. ADM’s Bursting Beans technology improves the sensory profile of plant proteins. They also launched a fermentation-derived protein, ProDiem, for allergen-free applications.

3. Ingredion

- Ingredion launched Vitessence Pulse 1803, a high-purity pea protein for meat and dairy alternatives. The company is investing in fava bean and chickpea protein production to diversify its plant-based portfolio. Ingredion’s VERSAFLEX textured pea protein enhances meat-like textures. They also partnered with PURIS to expand non-GMO and organic protein offerings.

4. Glanbia plc

- Glanbia’s Glanbia Nutritionals division introduced OptiSol 1000, a plant-based protein blend for beverages and bars. The company is expanding its pea and rice protein capabilities to meet demand for clean-label sports nutrition. Glanbia also invested in plant-based cheese alternatives through its joint venture, Levanta.

5. AGT Food and Ingredients

- AGT Food and Ingredients is scaling up production of pulse-based proteins, including pea and lentil isolates, for global markets. The company partnered with Roquette to enhance plant protein supply chains. AGT’s AI-powered processing improves protein yield and sustainability. They also launched high-fiber pea protein ingredients for functional foods.

Conclusion

The Plant-Based Protein Market is growing fast as more people choose healthier and eco-friendly food options. With rising demand for vegan and flexitarian diets, companies are creating new products like meat substitutes, dairy alternatives, and protein-packed snacks to meet consumer needs. The market is expected to keep expanding due to growing awareness of health benefits, sustainability concerns, and innovations in taste and texture. Businesses that focus on clean labels, diverse protein sources, and affordable pricing will likely lead the way in this exciting and dynamic market.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)