Table of Contents

Overview

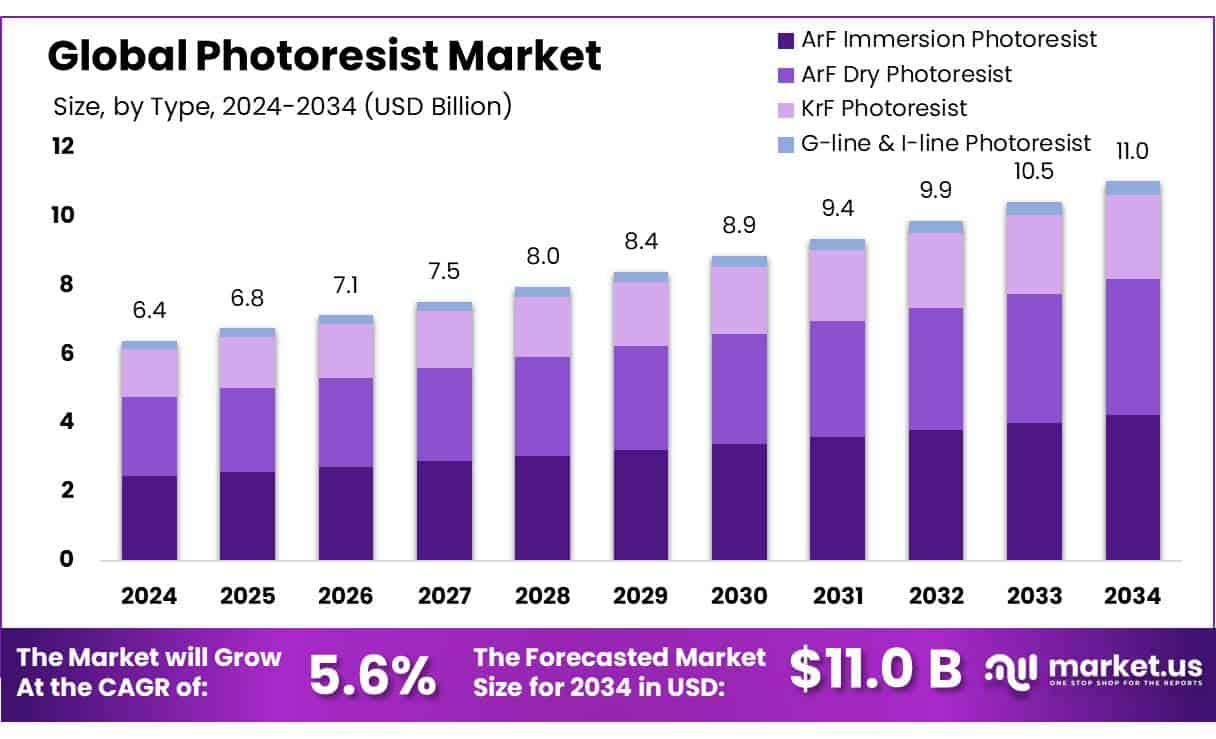

New York, NY – June 25, 2025 – The Global Photoresist Market is poised for significant expansion. Valued at USD 6.4 billion in 2024, the market is projected to reach USD 11.0 billion by 2034, driven by a robust CAGR of 5.6% from 2025 to 2034.

In 2024, ArF Immersion Photoresist led the market with a 38.4% share, driven by its exceptional resolution for advanced semiconductor manufacturing. Its use in immersion lithography, employing liquid between the lens and the wafer. Anti-reflective Coatings dominated in 2024, holding a 43.5% market share. These coatings reduce light reflections during photolithography, enhancing image accuracy and pattern precision on silicon wafers.

The Semiconductor & IC segment commanded a 63.6% share in 2024, fueled by global demand for consumer electronics, electric vehicles, and industrial automation. The Electronics segment led with a 68.1% share in 2024, driven by photoresist use in producing PCBs, displays, sensors, and microchips for consumer electronics like smartphones, laptops, OLED/LCD screens, and smartwatches.

Key Takeaways

- Photoresist Market size is expected to be worth around USD 11.0 billion by 2034, from USD 6.4 billion in 2024, growing at a CAGR of 5.6%.

- ArF Immersion Photoresist held a dominant market position, capturing more than a 38.4% share.

- Anti-reflective Coatings held a dominant market position, capturing more than a 43.5% share.

- Semiconductor & IC held a dominant market position, capturing more than a 63.6% share.

- Electronics held a dominant market position, capturing more than a 68.1% share.

- Asia-Pacific (APAC) region emerged as the dominant player in the global photoresist market, capturing a substantial 46.2% market share valued at approximately USD 2.9 billion.

How Growth is Impacting the Economy

- The Photoresist Market’s growth significantly impacts the global economy by fostering innovation and job creation in the semiconductor and electronics sectors. The rising demand for advanced chips, driven by 5G, IoT, and AI, fuels investments in manufacturing facilities, particularly in Asia-Pacific, which accounts for 46.2% of the market share.

- This expansion creates high-skill jobs, boosting local economies in countries like China and South Korea. Additionally, the market’s growth stimulates supply chains for raw materials and ancillary products, enhancing economic activity. However, high R&D costs and environmental regulations pose challenges, requiring sustainable practices to maintain economic benefits without compromising ecological standards.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/global-photoresist-market/request-sample/

Strategies for Businesses

- Businesses in the photoresist market should focus on innovation and sustainability to stay competitive. Investing in R&D for eco-friendly photoresist formulations can address stringent environmental regulations while meeting market demand. Strategic partnerships with chipmakers, as seen with DuPont’s collaborations, can enhance market reach.

- Expanding production facilities in high-growth regions like Asia-Pacific ensures proximity to key electronics hubs. Additionally, leveraging advanced technologies like EUV lithography can position companies as industry leaders. Diversifying product portfolios to include ancillaries like anti-reflective coatings will further strengthen market presence and revenue streams.

Report Scope

| Market Value (2024) | USD 6.4 Billion |

| Forecast Revenue (2034) | USD 11.0 Billion |

| CAGR (2025-2034) | 5.6% |

| Segments Covered | By Type (ArF Immersion Photoresist, ArF Dry Photoresist, KrF Photoresist, G-line and I-line Photoresist), By Product Type (Anti-reflective Coatings, Remover, Developer, Others), By Application (Semiconductor and IC, LCD, Printed Circuit Boards, Others), By End Use (Electronics, Automobile, Packaging, Others) |

| Competitive Landscape | ALLRESIST, DJ MicroLaminates, DuPont, Everlight Chemical Industrial Co., Fujifilm Corporation, JSR Corporation, LG Chem, Merck Group, Micro Resist Technology, Mitsui Chemicals Inc., Shin-Etsu Chemical Co., Ltd, Tokyo Ohka Kogyo Co., Ltd |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=150225

Key Market Segments

By Type

- In 2024, ArF Immersion Photoresist led the market with a 38.4% share, driven by its exceptional resolution for advanced semiconductor manufacturing. Its use in immersion lithography, employing liquid between the lens and the wafer, enables precise patterning for sub-10nm nodes, critical for cutting-edge chips in smartphones, processors, and memory devices. The adoption of 5nm and 3nm nodes by foundries like TSMC and Samsung sustained demand in 2024, bolstered by efforts in the U.S., Japan, and South Korea to localize advanced photolithography material sourcing.

By Product Type

- Anti-reflective Coatings dominated in 2024, holding a 43.5% market share. These coatings reduce light reflections during photolithography, enhancing image accuracy and pattern precision on silicon wafers. The surge in sub-10nm chip production for logic and memory devices amplified their importance, as even minor reflection distortions can cause defects. Leading foundries prioritized these coatings for consistent high-volume output in 2024.

By Application

- The Semiconductor & IC segment commanded a 63.6% share in 2024, fueled by global demand for consumer electronics, electric vehicles, and industrial automation. Photoresists were pivotal in fabricating integrated circuits and microprocessors, particularly for 5nm and 3nm nodes. Increased production by foundries and IDMs addressed prior supply shortages, while initiatives like the U.S. CHIPS Act and self-reliance programs in India and Europe boosted domestic chipmaking investments.

By End Use

- The Electronics segment led with a 68.1% share in 2024, driven by photoresist use in producing PCBs, displays, sensors, and microchips for consumer electronics like smartphones, laptops, OLED/LCD screens, and smartwatches. The rise of IoT devices and 5G infrastructure rollouts in countries like China, South Korea, and Taiwan further increased demand for miniaturized, high-performance components.

Regional Analysis

In 2024, the Asia-Pacific region held a 46.2% share of the global photoresist market, valued at approximately USD 2.9 billion. This dominance stems from major semiconductor hubs in China, Japan, South Korea, and Taiwan, which drive high photoresist consumption for advanced lithography. South Korea’s Samsung and SK Hynix led in memory chip production, while Taiwan’s TSMC invested over USD 30 billion in 2024, including EUV lithography upgrades. Japan’s expertise in high-purity photoresist materials further strengthened the region’s position. The APAC region is expected to continue leading in 2025, supported by ongoing fab expansions and material innovations.

Recent Developments

1. ALLRESIST

- ALLRESIST continues to expand its portfolio of high-resolution photoresists for microelectronics and MEMS applications. The company has introduced new epoxy-based negative photoresists with enhanced thermal stability, catering to advanced semiconductor packaging. Their latest products support higher aspect ratios for deep-etch lithography, meeting demand from the automotive and aerospace sectors.

2. DJ MicroLaminates

- DJ MicroLaminates has developed ultra-thin dry film photoresists for flexible electronics and PCB manufacturing. Their latest innovations include low-temperature curing resists, enabling compatibility with heat-sensitive substrates. The company is also collaborating with semiconductor firms to improve fine-line patterning for next-gen ICs.

3. DuPont

- DuPont has launched new extreme ultraviolet (EUV) photoresists to support advanced chipmaking at 3nm and below. Their Metal Oxide Photoresist (MOR) technology enhances resolution for high-NA EUV lithography. DuPont is also expanding production capacity in Asia to meet booming semiconductor demand.

4. Everlight Chemical Industrial Co.

- Everlight Chemical has introduced photosensitive polyimide (PSPI) resists for OLED and microLED displays, improving flexibility and durability. The company is also enhancing its color filter photoresists for 8K TVs and AR/VR devices. Everlight is investing in R&D for bio-based photoresists, aligning with green manufacturing trends.

5. Fujifilm Corporation

- Fujifilm has developed next-generation ArF immersion photoresists for cutting-edge logic and memory chips. Their new self-aligned quadruple patterning (SAQP) resists enable smaller transistor nodes. Fujifilm is also advancing nanoparticle photoresists for EUV applications and expanding its production facilities in the U.S. and Japan.

Conclusion

The Photoresist Market is on a strong growth path, driven by rising demand from the semiconductor, display, and PCB industries. With advancements in EUV and ArF lithography, manufacturers are developing higher-resolution photoresists to support cutting-edge chip production. The shift toward smaller, faster, and more efficient electronics is pushing innovation, while sustainability trends are encouraging eco-friendly photoresist formulations. Key regions like Asia-Pacific dominate due to booming semiconductor fabs, while North America and Europe focus on R&D for next-gen applications.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)