Table of Contents

Overview

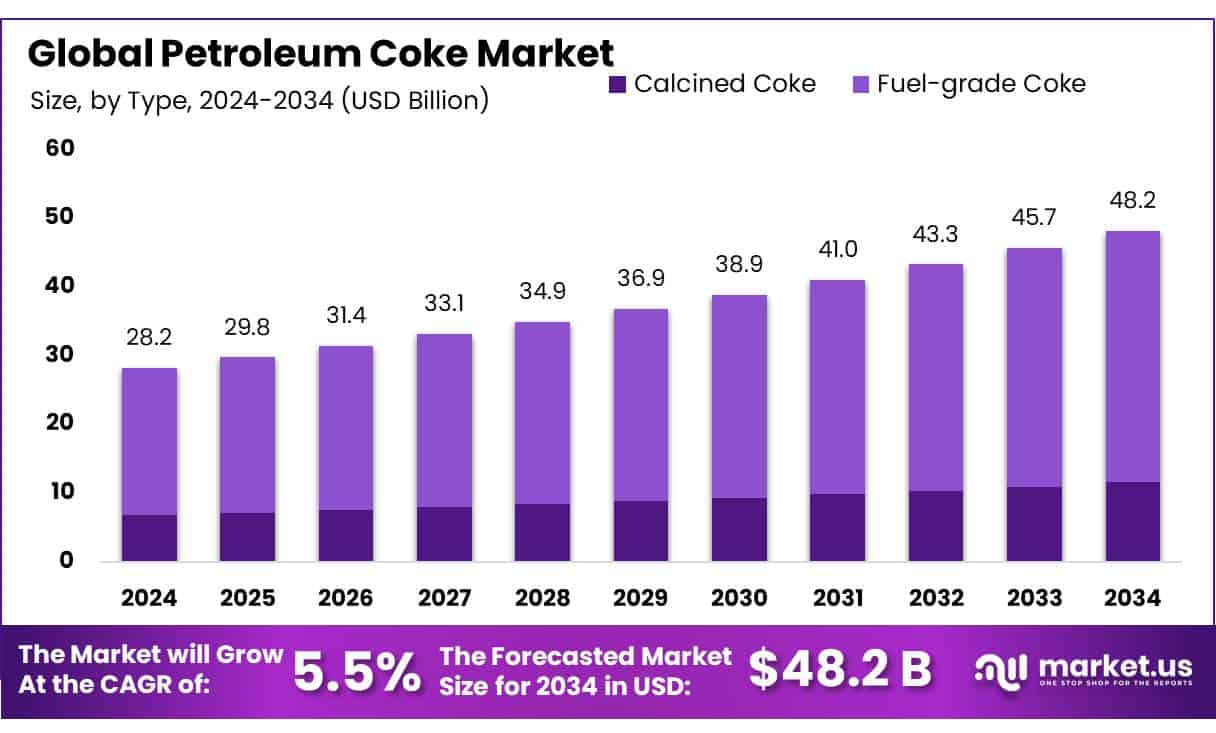

New York, NY – May 22, 2025 – The Global Petroleum Coke Market is experiencing strong growth, driven by rising demand across various industries. Valued at USD 28.2 billion in 2024, the market is projected to reach USD 48.2 billion by 2034, growing at a CAGR of 5.5% from 2025 to 2034.

Fuel-grade Coke leads the Petroleum Coke Market, commanding a 76.5% share in 2024 due to its high demand as an affordable, high-energy fuel. Delayed Coking holds a commanding 87.4% share of the Petroleum Coke Market in 2024, driven by its efficiency and widespread adoption. The Cement sector dominates the Petroleum Coke Market with a 38.4% share in 2024, driven by its extensive use as a cost-effective, high-energy fuel in cement production.

US Tariff Impact on Market

China’s retaliatory tariffs on US petroleum coke are set to disrupt bilateral trade as China seeks alternative sources to support its expanding battery material production. Global anode materials production is projected to reach 2.63 million metric tons in 2025, a 21% increase from 2024, with artificial anode materials comprising 89% of the total, requiring 3.2 million metric tons of petcoke.

The tariffs have raised duties on US petcoke imports to 37%, including a prior 3% tariff. During former US President Donald Trump’s term, China’s tariffs on US petcoke peaked at 33% in September 2019, combining a 25% retaliatory tariff from 2018 and a 5% tariff from 2019, in response to US tariffs on Chinese goods. This led to a 24.4% year-on-year decline in US petcoke shipments to China, totaling 2.67 million metric tons in 2019. Tariffs were reduced to 30% in March 2020, boosting imports.

➤ Get More Detailed Insights about US Tariff Impact @ – https://market.us/report/petroleum-coke-market/request-sample/

In 2024, China imported 3.87 million metric tons of petcoke from the US, representing 28.5% of its total imports, with over 25% of its petcoke demand met through imports. Uncalcined needle coke (max 0.5% sulfur) was assessed at Yuan 6,350/mt (USD 865/mt) DDP Qingdao on April 8, up 21% since February. Platts assessments consider needle coke with max 5% moisture, min 1.35 g/cu cm true density, max 0.1% ash, and 4%-7% volatile matter.

Key Takeaways

- Petroleum Coke Market size is expected to be worth around USD 48.2 Bn by 2034, from USD 28.2 Bn in 2024, growing at a CAGR of 5.5%.

- Fuel-grade Coke held a dominant market position, capturing more than a 76.5% share.

- Delayed Coking held a dominant market position, capturing more than 87.4% share in the Petroleum Coke Market by Coking Process.

- Cement held a dominant market position, capturing more than a 38.4% share in the Petroleum Coke Market by Application.

- Asia-Pacific (APAC) region stands as the dominant force in the global petroleum coke market, holding a substantial market share of approximately 44.3%, which translates to a market value of USD 12.4 billion.

Report Scope

| Market Value (2024) | USD 28.2 Billion |

| Forecast Revenue (2034) | USD 48.2 Billion |

| CAGR (2025-2034) | 5.5% |

| Segments Covered | By Type (Calcined Coke, Fuel-grade Coke, Shot Coke, Sponge Coke), By Coking Process (Delayed Coking, Fluid Coking), By Application (Cement, Ceramic, Power Generation, Industrial Boilers, Aluminum and Other Metals, Carbon Products, Others) |

| Competitive Landscape | BP p.l.c., Chevron Corporation, Oxbow Corporation, The Phillips 66 Company, Aminco Resources LLC, Reliance Industries Ltd, HPCL-Mittal Energy Limited, Indian Oil Corporation Ltd, Marathon Petroleum Corporation, China Petrochemical Corporation, Bharat Petroleum Corporation Limited, Rain Carbon Inc, Repsol S.A., Valero Energy Corporation, Other Key Players |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=147096

Key Market Segments

By Type

- Fuel-grade Coke leads the Petroleum Coke Market, commanding a 76.5% share in 2024 due to its high demand as an affordable, high-energy fuel. Widely used in industries like cement, power generation, and steel production, its cost-effectiveness and superior calorific value drive its dominance. The growing reliance on economic thermal fuels in emerging economies further strengthens its position.

- In 2025, Fuel-grade Coke is expected to maintain its market leadership, fueled by expanding infrastructure projects in regions like Asia-Pacific and Latin America. Advances in combustion technologies to reduce emissions will support its continued use, ensuring Fuel-grade Coke remains the top choice despite environmental concerns.

By Coking Process

- Delayed Coking holds a commanding 87.4% share of the Petroleum Coke Market in 2024, driven by its efficiency and widespread adoption. This process efficiently transforms heavy residual oils into valuable petroleum coke and lighter products, offering flexibility and high yields across diverse feedstocks.

- In 2025, Delayed Coking is poised to retain its dominance, supported by increased heavy crude processing and refinery expansions in Asia-Pacific and the Middle East. Its reliability, economic advantages, and adaptability to stricter environmental standards solidify its position as the leading coking method in the industry.

By Application

- The Cement sector dominates the Petroleum Coke Market with a 38.4% share in 2024, driven by its extensive use as a cost-effective, high-energy fuel in cement production. Rapid infrastructure growth and construction projects in regions like Asia-Pacific and the Middle East fuel this demand.

- In 2025, the Cement segment is expected to maintain its lead, supported by ongoing global housing, road, and industrial developments. Upgrades in cement plants to enhance petcoke efficiency while addressing emissions will ensure its continued prominence as a vital fuel source in the sector.

Regional Analysis

- The Asia-Pacific (APAC) region leads the global petroleum coke market, commanding a significant 44.3% share, valued at approximately USD 12.4 billion. This dominance is driven by robust industrial activity in key economies like China and India, where petroleum coke is a vital fuel for energy production and a key raw material in aluminum and steel manufacturing.

- China, the region’s top consumer, fuels demand through its massive aluminum and steel industries, which support extensive urbanization and infrastructure projects. The need for aluminum in construction and steel in manufacturing and automotive sectors significantly boosts petroleum coke consumption. India, following closely, relies on petroleum coke to meet its growing energy demands, spurred by rapid economic expansion and increasing power requirements.

Top Use Cases

- Cement Production: Petcoke is a key fuel in cement kilns due to its high calorific value and cost efficiency. It helps reduce energy costs for manufacturers, especially in developing countries. However, its high sulfur content raises environmental concerns, pushing some plants to adopt cleaner alternatives or emission control technologies.

- Power Generation: In countries with lax emissions regulations, petcoke is used in power plants as a cheaper alternative to coal. Its high energy density makes it attractive, but carbon-intensive burning limits its use in regions with strict climate policies. Some plants blend it with biomass to lower emissions.

- Steel & Aluminum Industry: Petcoke serves as a carbon source in anode production for aluminum smelting. Steel plants also use it in blast furnaces for heat and carbon injection. Demand remains stable, but the shift toward green steel could reduce long-term reliance on petcoke.

- Refinery Byproduct Utilization: Refineries produce petcoke as a residue from crude oil processing. Selling it generates additional revenue, but environmental pressures are pushing refiners to explore carbon capture or alternative uses, such as synthetic graphite production.

- Export & Global Trade: Asia and Latin America are major importers of petcoke due to lower environmental restrictions. The U.S. and Saudi Arabia are top exporters. Trade dynamics depend on energy demand, regulations, and competition from alternative fuels like natural gas and renewables.

Recent Developments

1. BP p.l.c.

- BP has been focusing on reducing its carbon footprint, including petcoke production. The company aims to align with net-zero goals by cutting fossil fuel investments. BP’s latest sustainability report highlights a decline in petcoke output as it shifts toward renewable energy. However, it still supplies petcoke to industrial users while exploring carbon capture solutions.

2. Chevron Corporation

- Chevron continues petcoke production but is investing in carbon capture and hydrogen projects to offset emissions. The company’s Pascagoula refinery produces petcoke, and Chevron is exploring ways to reduce its environmental impact. Recent reports indicate a focus on cleaner refining processes.

3. Oxbow Corporation

- Oxbow, a major petcoke trader, remains active in global markets, supplying fuel-grade petcoke to the cement and power industries. The company has faced environmental scrutiny but emphasizes compliance with regulations. Recent deals include supplying Asian markets with U.S.-sourced petcoke.

4. Phillips 66

- Phillips 66 produces petcoke as a byproduct and has been optimizing refinery operations to balance output with environmental concerns. The company’s latest investor report mentions petcoke sales but highlights a shift toward renewable diesel and sustainable aviation fuel.

5. Aminco Resources LLC

- Aminco Resources specializes in petcoke trading and logistics, particularly in Latin America and Asia. Recent updates show expanded partnerships with refineries and industrial buyers. The company emphasizes efficient supply chain solutions for petcoke distribution.

Conclusion

The Petroleum Coke (Petcoke) Market remains steady, driven by demand from cement, power, and steel industries, especially in emerging economies. However, environmental concerns and stricter carbon regulations are pushing major players like BP and Chevron to reduce production and invest in cleaner alternatives. Companies like Phillips 66 are balancing petcoke sales with renewable fuel projects, while traders like Oxbow and Aminco Resources continue supplying global markets, particularly in Asia and Latin America.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)