Table of Contents

Overview

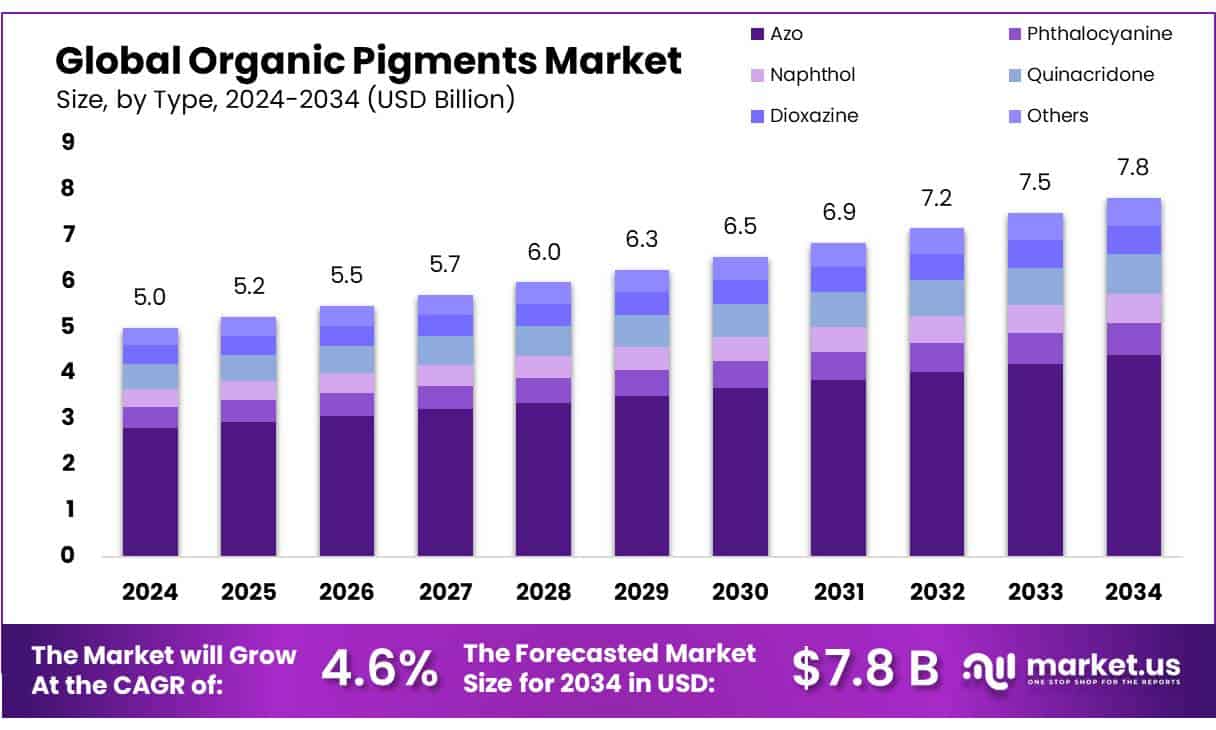

New York, NY – July 16, 2025 – The Global Organic Pigments Market is growing fast, driven by high demand from industries like paints, plastics, textiles, and printing inks. In 2024, the market was valued at USD 5.0 billion, and it is expected to reach USD 7.8 billion by 2034, expanding at a CAGR of 4.6% from 2025 to 2034.

Government initiatives are bolstering local production in India, with the Make in India policy driving domestic pigment manufacturing. The Production Linked Incentive (PLI) scheme allocates over INR 1.97 lakh crore (USD 28 billion) to the chemical and specialty sectors, providing performance-based subsidies to boost domestic sales and attract investment in chemical intermediates and pigment production.

This fosters raw material integration and value addition. Additionally, organic agriculture initiatives, with over 40% growth in certified organic farmland, enhance feedstock availability for natural organic pigments. On the supply side, the Mission Organic Value Chain Development in North East India (MOVCD-NER) supports organic agriculture—a key source of bio-based pigment feedstock—engaging 50,000 farmers across 50,000 hectares since 2015.

Similarly, the Paramparagat Krishi Vikas Yojana (PKVY) offers up to INR 20,000 per acre over three years to establish 500,000 acres of organic farming through 10,000 clusters. Aligned with the National Programme for Organic Production (NPOP), these programs strengthen the raw material supply chain, supporting “Make in India” and sustainability goals.

Key Takeaways

- Organic Pigments Market size is expected to be worth around USD 7.8 Bn by 2034, from USD 5.0 Bn in 2024, growing at a CAGR of 4.6%.

- Azo held a dominant market position, capturing more than a 56.2% share of the global organic pigments market.

- Printing Inks held a dominant market position, capturing more than a 46.1% share of the global organic pigments market.

- Asia-Pacific (APAC) region holds a dominant position in the global organic pigments market, capturing a significant share of 38.9%, which equates to approximately USD 1.9 billion.

How Growth is Impacting the Economy

The growth of India’s organic pigments market significantly impacts the economy by fostering job creation, enhancing export potential, and strengthening industrial ecosystems. The PLI scheme attracts investments in chemical intermediates, spurring innovation and value addition in sectors like paints, coatings, and printing inks.

Organic agriculture initiatives, such as MOVCD-NER and PKVY, engage thousands of farmers, boosting rural economies and increasing disposable incomes. India’s global market share grows, reducing import dependency. This aligns with sustainability trends, enhancing India’s reputation as a hub for eco-friendly products, further driving economic resilience and industrial growth.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/global-organic-pigments-market/request-sample/

Strategies for Businesses

Businesses should capitalize on government incentives like the PLI scheme to invest in advanced manufacturing facilities for organic pigments. Leveraging MOVCD-NER and PKVY, companies can secure reliable bio-based feedstock through partnerships with organic farmers. Adopting eco-friendly production processes and aligning with clean-label trends in food and cosmetics will meet rising consumer demand. Expanding into high-growth applications like printing inks and sustainable packaging, while ensuring compliance with NPOP certification, can enhance market competitiveness. Strategic collaborations with FPOs and investment in R&D for high-performance pigments will drive innovation and market share.

Report Scope

| Market Value (2024) | USD 5.0 Billion |

| Forecast Revenue (2034) | USD 7.8 Billion |

| CAGR (2025-2034) | 4.6% |

| Segments Covered | By Type (Azo, Phthalocyanine, Naphthol, Quinacridone, Dioxazine, Others), By Application (Printing Inks, Paints and Coatings, Plastics, Textile Dyeing, Art Supplies, Cosmetics and Personal Care, Electronic Displays, Others) |

| Competitive Landscape | Anshan Hifichem Co., Ltd., Atul Ltd, Dainichiseika Color & Chemicals Mfg. Co., Ltd., DIC Corporation, Ferro Corporation, Heubach GmbH, Huntsman Corporation, Kemira, Lanxess, Lily Group Co. Ltd., Meghmani Organics Ltd., Sudarshan Chemical Industries Ltd, Sun Chemical, Sunlour Pigment Co., Ltd., Artience Co., Ltd. |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=151195

Key Market Segments

By Type

- In 2024, Azo pigments commanded a leading 56.2% share of the global organic pigments market, driven by their extensive use in industries like plastics, coatings, textiles, and printing inks. Their popularity stems from vibrant colors, excellent dispersibility, and cost-efficient production, making them ideal for high-volume applications. Compatible with both solvent- and water-based systems, Azo pigments continue to be a top choice for manufacturers. This trend is projected to persist into 2025, with Azo pigments retaining their dominance due to their affordability and performance in diverse applications.

By Application

- In 2024, the Printing Inks segment held a commanding 46.1% share of the global organic pigments market, driven by widespread use in flexographic, gravure, and digital printing, particularly for packaging, labels, and commercial publishing. The shift toward eco-friendly inks and the growing need for vibrant, durable colors in sustainable packaging have boosted demand for organic pigments in this sector. This dominance is expected to continue in 2025, supported by the global expansion of the packaging and labeling industry, especially in food, beverage, and consumer goods.

Regional Analysis

The Asia-Pacific (APAC) region dominates the global organic pigments market, holding a 38.9% share, equivalent to approximately USD 1.9 billion in 2024. This growth is fueled by increasing demand for natural colorants in industries such as food and beverages, cosmetics, and textiles. Countries like China, India, and Japan, with their robust manufacturing bases, drive this market leadership.

The region’s large consumer base is increasingly favoring clean-label and organic products, further boosting demand for organic pigments. Notably, China’s food and beverage sector has seen significant growth, with a 20% rise in demand for natural colorants in organic food products, according to the Food and Agriculture Organization (FAO). Rising health and wellness awareness, particularly among urban middle-class populations, continues to propel the shift toward organic pigments in APAC.

Recent Developments

1. Anshan Hifichem Co., Ltd.

- Anshan Hifichem has expanded its production capacity for high-performance organic pigments, focusing on eco-friendly solutions for coatings and plastics. The company is investing in R&D to develop pigments with improved heat stability and lightfastness. Their latest innovations target the automotive and packaging industries.

2. Atul Ltd

- Atul Ltd has introduced new sustainable pigment ranges under its “Colourants” division, complying with global environmental standards. The company is strengthening its presence in Europe and North America, with a focus on water-based and low-VOC pigments for inks and coatings.

3. Dainichiseika Color & Chemicals Mfg. Co., Ltd.

- Dainichiseika has developed advanced organic pigments for digital printing and LCD color filters. The company is collaborating with tech firms to enhance pigment performance in electronics and automotive applications.

4. DIC Corporation

- DIC Corporation has launched new phthalocyanine and azo pigments with enhanced durability for packaging and textiles. The company is also focusing on bio-based pigments to meet sustainability goals.

5. Ferro Corporation

- Ferro (now part of Prince International) has expanded its Vibrantz pigment portfolio, offering high-color-strength solutions for coatings and plastics. The company is investing in nanotechnology for next-gen pigment applications.

Conclusion

India’s organic pigments market is on a dynamic growth trajectory, fueled by government initiatives like Make in India and organic farming schemes. These efforts enhance economic growth, create jobs, and boost exports while aligning with global sustainability trends. Businesses can thrive by leveraging incentives, innovating, and targeting high-demand sectors. With a strong outlook driven by policy support and consumer demand, the market is set to solidify India’s position as a global leader in organic pigments, contributing to a sustainable and economically vibrant future.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)