Table of Contents

Overview

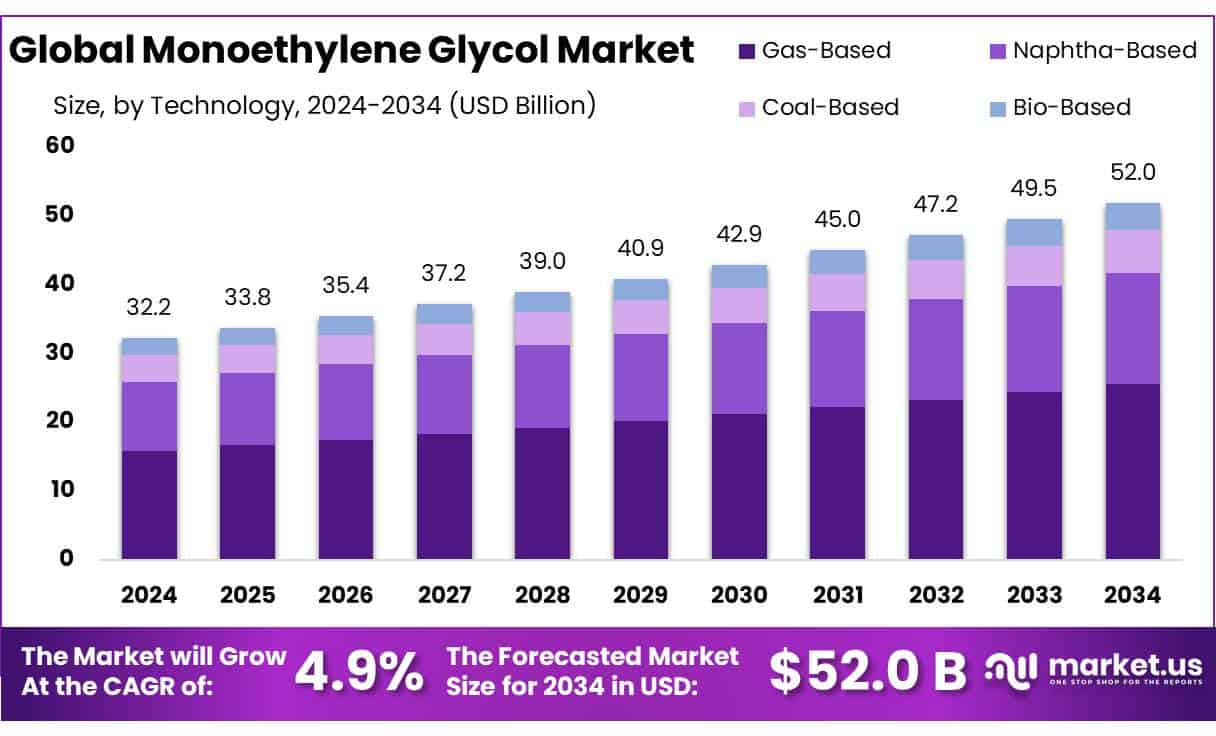

New York, NY – July 23, 2025 – The Global Monoethylene Glycol (MEG) Market is projected to grow significantly, reaching USD 52.0 billion by 2034, up from USD 32.2 billion in 2024, with a steady CAGR of 4.9% during 2025–2034.

Monoethylene glycol (MEG) is a critical component in the petrochemical industry, primarily used in producing polyester fibers, PET resins, and applications like antifreeze, solvents, and heat-transfer fluids. Its industrial production involves two main steps: ethylene oxidation to ethylene oxide, followed by hydration to MEG. The traditional hydration process yields up to 90%, while the advanced Shell OMEGA process, licensed from Mitsubishi Chemicals, achieves over 99% selectivity, minimizing byproducts and waste-heat requirements.

The U.S. Energy Information Administration (EIA) reported a 25% fluctuation in crude oil prices over six months in 2024, impacting ethylene and MEG production costs. In Europe, natural gas prices spiked by over 50% in 2024, adding pressure on ethylene-dependent industries like chemicals and plastics, making cost prediction and planning difficult for MEG producers.

The U.S. Environmental Protection Agency (EPA) reported a 29% recycling rate for PET bottles and jars in 2022, highlighting significant potential for recycled PET (rPET) growth. As rPET demand rises, so does the need for MEG, offering a key growth opportunity for the market. The U.S. Department of Energy notes that domestic ethane production, a key feedstock for ethylene, nearly doubled from 0.95 million barrels per day in 2013 to about 1.85 million b/d by early 2021, with exports also hitting record highs.

This growth in ethane supply is expected to sustain petrochemical demand, including for MEG, through at least 2023. Advancements in technology, such as improved catalysts, heat and CO2 integration, and bio- or waste-based production methods, are driving cost efficiencies and environmental benefits. For instance, pilot-scale models show high-yield MEG production from integrated ethylene-to-ethylene oxide and MEG plants with a capacity of 600,000 t/y.

Key Takeaways

- Monoethylene Glycol Market size is expected to be worth around USD 52.0 Billion by 2034, from USD 32.2 Billion in 2024, growing at a CAGR of 4.9%.

- Gas-Based technology held a dominant market position in the global monoethylene glycol (MEG) market, capturing more than a 49.3% share.

- Polyester Fibers held a dominant market position in the global monoethylene glycol (MEG) market, capturing more than a 59.1% share.

- Textile held a dominant market position in the global monoethylene glycol (MEG) market, capturing more than a 56.8% share.

- Asia-Pacific (APAC) region stands as the dominant force in the global Monoethylene Glycol (MEG) market, commanding a substantial share of 42.9%, equating to approximately USD 13.8 billion.

How Growth is Impacting the Economy

The MEG market’s expansion significantly influences the global economy. Rising demand for PET in food packaging creates jobs in manufacturing and recycling sectors. The U.S. ethane production surge bolsters petrochemical exports, strengthening trade balances. However, 2024’s crude oil price volatility and Europe’s natural gas price spike challenge cost stability, impacting profit margins. The PET recycling rate in 2022 highlights rPET’s growth potential, driving investments in sustainable technologies. These dynamics stimulate economic activity but require adaptive strategies to manage price fluctuations and environmental pressures.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/global-monoethylene-glycol-market/request-sample/

Strategies for Businesses

Businesses in the MEG market should adopt innovative technologies like the Shell OMEGA process to enhance yield and reduce waste. Investing in bio-based and waste-derived MEG production can lower costs and meet sustainability demands. Diversifying supply chains mitigates risks from crude oil and natural gas price volatility. Strengthening recycling partnerships to boost rPET production aligns with the PET recycling rate, capturing growing demand. Leveraging data-driven forecasting tools can improve cost management amid 2024’s Oil price swings, ensuring competitive pricing and stable margins.

Report Scope

| Market Value (2024) | USD 32.2 Billion |

| Forecast Revenue (2034) | USD 52.0 Billion |

| CAGR (2025-2034) | 4.9% |

| Segments Covered | By Technology (Gas-Based, Naphtha-Based, Coal-Based, Bio-Based), By Application (PET, Polyester Fibers, Antifreeze, Others), By End-use (Textile, Packaging, Automotive, Plastics, Other) |

| Competitive Landscape | Acuro Organics Ltd., Arham Petrochem Pvt. Ltd., BASF SE, Dow, Euro Industrial Chemicals, India Glycols Limited, Indian Oil Corporation Ltd., Ishtar Company, LLC, Kimia Pars Co., LyondellBasell N.V., MEGlobal, Mitsubishi Chemical Corporation, Nan Ya Plastics Corporation, Nouryon, Pon Pure Chemicals Group |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=151602

Key Market Segments

By Technology

In 2024, Gas-Based technology commanded a 49.3% share of the global monoethylene glycol (MEG) market, maintaining its dominance due to cost-effective production processes, particularly in regions rich in natural gas. This method offers lower feedstock costs and reduced carbon emissions compared to naphtha-based alternatives, appealing to manufacturers prioritizing efficiency and sustainability.

By Application

In 2024, Polyester Fibers accounted for over 59.1% of the global monoethylene glycol (MEG) market, driven by strong demand for synthetic textiles in apparel, home furnishings, and industrial applications. As a critical component in polyester production, MEG consumption closely tracks the growth of polyester fiber manufacturing.

The textile industry’s expansion, particularly in Asia-Pacific nations like China, India, and Vietnam, significantly boosted MEG demand. The popularity of lightweight, wrinkle-resistant, and moisture-wicking fabrics further supported this segment. This trend is expected to continue into 2025, driven by urbanization and rising consumer spending on affordable fashion.

By End-Use

In 2024, the Textile industry captured over 56.8% of the global monoethylene glycol (MEG) market, largely due to its reliance on polyester fibers for clothing, upholstery, home textiles, and industrial fabrics. The global demand for affordable, durable, and lightweight synthetic fabrics has driven MEG consumption in textile manufacturing.

This trend, sustained into early 2025, is supported by increased textile exports from Asia-Pacific, advancements in fabric technology, and consumer preference for low-maintenance, quick-drying materials. The textile industry’s heavy dependence on polyester ensures MEG’s critical role in this sector.

Regional Analysis

The Asia-Pacific (APAC) region leads the global Monoethylene Glycol (MEG) market, holding a commanding 42.9% share, valued at approximately USD 13.8 billion. This dominance is driven by the region’s strong industrial foundation, particularly in China and India, which are key players in MEG production and consumption.

China’s robust manufacturing sector, especially in textiles and packaging, fuels significant MEG demand. Its textile industry, a primary consumer of MEG, continues to grow due to strong domestic and export markets. In India, the expanding textile and automotive sectors are driving MEG usage, with the latter increasingly relying on MEG-based antifreeze and coolant solutions. Government initiatives to support the automotive industry, including electric vehicle promotion, further boost MEG applications.

Additionally, APAC’s focus on sustainability is shaping market trends. The shift toward bio-based MEG production aligns with global environmental goals, with regional investments in green technologies and renewable resources. This transition meets the growing demand for eco-friendly products and establishes APAC as a pioneer in sustainable MEG production.

Recent Developments

1. Acuro Organics Ltd.

- Acuro Organics has expanded its MEG production capacity to meet rising demand from the textile and packaging industries. The company is focusing on sustainable production methods, including energy-efficient processes. They are also exploring bio-based MEG alternatives to align with global environmental regulations.

2. Arham Petrochem Pvt. Ltd.

- Arham Petrochem has strengthened its MEG supply chain to cater to growing polyester fiber demand in India. The company is investing in advanced purification technologies to enhance product quality. They are also expanding distribution networks in Southeast Asia and Africa.

3. BASF SE

- BASF is innovating in bio-based MEG production using renewable feedstocks. They recently partnered with a biotech firm to develop sustainable MEG for polyester applications. BASF is also optimizing MEG for electric vehicle coolants, supporting the automotive industry’s shift toward greener solutions.

4. Dow

- Dow has introduced a new high-purity MEG grade for PET bottle manufacturing, enhancing recyclability. The company is expanding MEG production in the U.S. and Asia to meet rising demand. Dow is also investing in carbon-neutral MEG production to reduce environmental impact.

5. Euro Industrial Chemicals

- Euro Industrial Chemicals has launched a new MEG formulation with improved stability for antifreeze applications. The company is increasing exports to Europe and the Middle East, focusing on high-growth markets. They are also adopting digital supply chain solutions for better efficiency.

Conclusion

The MEG market’s growth, driven by PET demand and ethane supply, presents economic opportunities but faces challenges from price volatility and sustainability pressures. Businesses adopting advanced technologies and recycling strategies can thrive. The push for rPET and innovative production methods signals a resilient future. Strategic adaptation will ensure MEG manufacturers capitalize on growth while addressing economic and environmental demands, fostering long-term stability.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)