Table of Contents

Overview

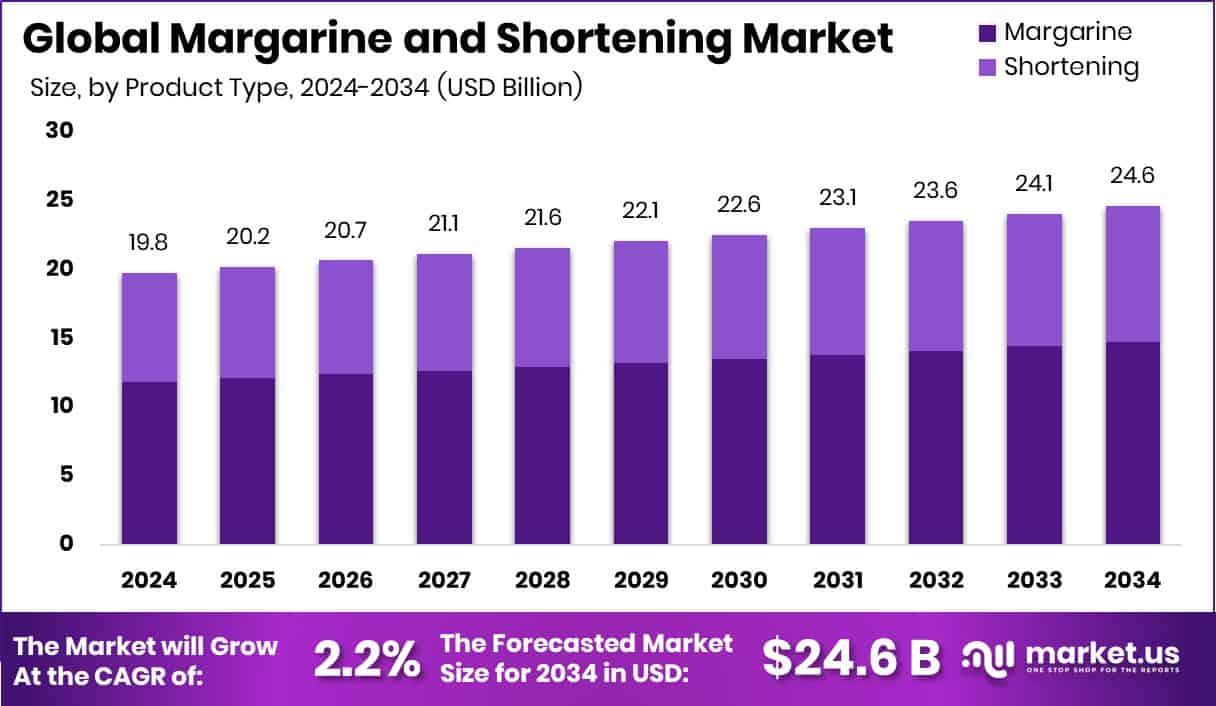

New York, NY – June 06, 2025 – The Global Margarine and Shortening Market is set to grow steadily, with an expected value of USD 24.6 billion by 2034, up from USD 19.8 billion in 2024, at a CAGR of 2.2% from 2025 to 2034. In 2024, Margarine dominated the product type segment of the margarine and shortening market, capturing a 59.9% share. Its widespread use in household and foodservice cooking and baking drives this lead.

Plant-based sources led the source segment in 2024, holding a 76.3% share of the margarine and shortening market. This reflects a global shift toward healthier, sustainable, and ethical food choices. Solid forms dominated the form segment in 2024, accounting for a 69.4% share of the margarine and shortening market. Their superior structural properties make them ideal for commercial and household baking, including dough, batters, and pastries.

Baking and pastry applications led the application segment in 2024, with a 56.1% share of the margarine and shortening market. Margarine and shortening are essential for achieving desired textures, flavors, and shelf stability in baked goods. Retail dominated the end-use segment in 2024, holding a 67.2% share of the margarine and shortening market. Household reliance on affordable, user-friendly, and shelf-stable margarine and shortening for daily cooking and baking drives this lead. Supermarkets and Hypermarkets led the distribution channel segment in 2024, capturing a 38.7% share of the margarine and shortening market.

Key Takeaways

- Global Margarine and Shortening Market is expected to be worth around USD 24.6 billion by 2034, up from USD 19.8 billion in 2024, and grow at a CAGR of 2.2% from 2025 to 2034.

- Margarine holds 59.9% market share by product type, showing a strong preference over traditional shortening options.

- Plant-based variants dominate the source category with 76.3%, reflecting rising demand for vegan-friendly fat alternatives.

- Solid form products account for 69.4% of the market and are preferred for stability in baking applications.

- Baking and pastry lead the application segment with 56.1%, driven by the bakery industry’s growing global presence.

- Retail dominates end-use at 67.2%, showing margarine and shortening’s strong penetration in household cooking routines.

- Supermarkets and hypermarkets capture 38.7% share, serving as primary access points for mass consumer distribution.

- North America dominates the Margarine and Shortening Market with 38.9% regional share.

How Growth is Impacting the Economy

- The growth of the margarine and shortening market significantly impacts the global economy. Increased demand for plant-based products supports agricultural economies, boosting vegetable oil industries like soybean and palm. Companies like Wilmar International and Bunge Limited drive economic activity through investments in facilities and innovation, enhancing supply chains.

- The shift to healthier, low-trans-fat formulations aligns with consumer trends, increasing sales in supermarkets, which capture 38.7% of distribution. However, health concerns over saturated fats challenge growth, pushing firms to invest in R&D for cleaner-label products. This fosters economic resilience by encouraging sustainable practices and meeting regulatory demands, while emerging markets like Asia-Pacific contribute to global trade through rising disposable incomes and urbanization.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/global-margarine-and-shortening-market/request-sample/

Strategies for Businesses

- Businesses in the margarine and shortening market should focus on innovation, emphasizing plant-based, low-trans-fat, and clean-label products to meet health-conscious consumer demands. Investing in sustainable sourcing, like non-GMO oils, enhances brand appeal. Strategic partnerships, such as Associated British Foods’ collaboration with Stratas Foods, can strengthen market presence.

- Leveraging technology for advanced processing, like SPX Flow, improves efficiency and product quality. Targeting emerging markets like Asia-Pacific, driven by urbanization, and offering premium, artisanal products can capture new consumer segments and drive revenue growth.

Report Scope

| Market Value (2024) | USD 19.8 Billion |

| Forecast Revenue (2034) | USD 24.6 Billion |

| CAGR (2025-2034) | 2.2% |

| Segments Covered | By Product Type (Margarine, Shortening), By Source (Plant-based, Animal-based), By Form (Solid, Liquid), By Application (Baking and Pastry, Cooking and Frying, Spreads and Toppings, Others), By End Use (Retail, Food Service, Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Others) |

| Competitive Landscape | AAK AB, Associated British Foods PLC, Bunge Limited, Cargill Incorporated, Conagra Brands Inc., Dairy Farmers of America, Fediol, Fuji Oil Co., Ltd., J.M. Smucker Company, NMGK Group, Premium Vegetable Oils Sdn Bhd, Puratos Group, Richardson International Limited, Unilever, Vandemoortele, Wilmar International Ltd. |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=149066

Key Market Segments

By Product Type Analysis

- In 2024, margarine dominated the product type segment of the margarine and shortening market, capturing a 59.9% share. Its widespread use in household and foodservice cooking and baking drives this lead. Margarine’s affordability, shelf stability, and plant-based appeal make it a popular butter alternative, particularly in health-conscious regions.

- Its versatility in spreads, pastries, and sauces ensures its relevance in both home and industrial kitchens. Innovations in margarine formulations, such as added vitamins and improved flavors, along with consumer preference for lower cholesterol and trans-fat options, bolster its market strength. Retail promotions, private-label growth, and favorable margins for manufacturers further solidify margarine’s dominance.

By Source Analysis

- Plant-based sources led the source segment in 2024, holding a 76.3% share of the margarine and shortening market. This reflects a global shift toward healthier, sustainable, and ethical food choices. Plant-based margarine and shortening, derived from oils like soybean, sunflower, canola, and palm, are favored for their lower saturated fat and cholesterol content.

- They appeal to health-conscious consumers, vegetarians, and those with dietary restrictions. Stable supply chains and cost-effective sourcing enhance their dominance, while food processors value their formulation flexibility. Retail and foodservice sectors increasingly offer vegan-friendly, clean-label products, supported by government initiatives promoting sustainable agriculture, ensuring plant-based sources maintain their market leadership.

By Form Analysis

- Solid forms dominated the form segment in 2024, accounting for a 69.4% share of the margarine and shortening market. Their superior structural properties make them ideal for commercial and household baking, including dough, batters, and pastries.

- Solid margarine and shortening offer consistency, stability, and ease of measurement, making them preferred in bakeries, foodservice, and packaged food manufacturing. Their longer shelf life and reduced spoilage risk enhance cost-efficiency in commercial settings. Available in retail and bulk packaging, solid forms meet diverse needs, reinforcing their strong market position.

By Application Analysis

- Baking and pastry applications led the application segment in 2024, with a 56.1% share of the margarine and shortening market. Margarine and shortening are essential for achieving desired textures, flavors, and shelf stability in baked goods.

- Their cost-effectiveness compared to butter drives adoption in both artisanal and industrial baking, particularly for lamination, creaming, and frying. Demand from cafés, quick-service restaurants, and packaged food brands further fuels growth. Solid forms, valued for their temperature stability, are especially critical in pastry production, cementing this segment’s dominance.

By End Use Analysis

- Retail dominated the end-use segment in 2024, holding a 67.2% share of the margarine and shortening market. Household reliance on affordable, user-friendly, and shelf-stable margarine and shortening for daily cooking and baking drives this lead. These products are staples in grocery baskets, particularly for budget-conscious and health-aware consumers seeking plant-based options.

- Strong distribution through supermarkets, hypermarkets, and local stores ensures accessibility. Private-label brands and innovations like cholesterol-free or vitamin-fortified margarines, amplified by cooking shows and online recipes, boost retail appeal and sustain this segment’s dominance.

By Distribution Channel Analysis

- Supermarkets and hypermarkets led the distribution channel segment in 2024, capturing a 38.7% share of the margarine and shortening market. These large-format stores are the primary purchase point due to their convenience, product variety, and competitive pricing.

- Urban and semi-urban locations, significant shelf space for cooking fats, and promotional activities like sampling and loyalty programs drive sales. Efficient cold storage and supply chains ensure the consistent availability of perishable margarine products. As organized retail grows in emerging markets, supermarkets and hypermarkets maintain their position as the leading distribution channel.

Regional Analysis

- In 2024, North America held a 38.9% share of the global margarine and shortening market, valued at USD 7.7 billion. Its leadership stems from a robust food processing industry, high bakery product demand, and preference for plant-based fats. Europe follows, driven by traditional margarine use in baking and growing demand for dairy-free, health-focused products.

- Asia Pacific sees rapid growth due to urbanization and rising incomes, though its share lags behind North America and Europe. The Middle East & Africa show gradual adoption, fueled by expanding foodservice and margarine’s affordability. Latin America, while smaller, grows steadily with interest in cost-effective bakery fats. North America remains the top region, supported by high consumption and integration across food sectors.

Recent Developments

1. AAK AB

- AAK has focused on sustainable and plant-based margarine solutions, leveraging its expertise in vegetable oils. The company recently launched a new range of non-hydrogenated margarines with reduced saturated fats, catering to health-conscious consumers. AAK emphasizes clean-label ingredients and partnerships with food manufacturers to innovate in bakery and dairy alternatives.

2. Associated British Foods PLC (ABF)

- ABF, through its subsidiary AB Mauri, has expanded its bakery fats portfolio, including margarine and shortening with improved functionality for industrial baking. Recent innovations focus on reducing trans fats and enhancing shelf stability. ABF also invests in sustainable palm oil sourcing to meet environmental standards.

3. Bunge Limited

- Bunge has introduced high-performance shortening and margarine solutions for foodservice and bakery sectors, emphasizing zero trans fats and non-GMO ingredients. The company recently partnered with food manufacturers to develop customized fat systems for plant-based alternatives, supporting the shift toward sustainable diets.

4. Cargill Incorporated

- Cargill has launched Clear Valley high-stability shortening and margarine, designed for extended fry life and better texture in baked goods. The company is also innovating in plant-based margarines, using sustainable oils like canola and sunflower. Cargill’s R&D focuses on reducing saturated fats while maintaining performance.

5. Conagra Brands Inc.

- Conagra, known for brands like Blue Bonnet and Fleischmann’s, has reformulated its margarine products to remove artificial trans fats and hydrogenated oils. Recent efforts include introducing plant-based butter alternatives and portion-controlled margarine options for health-focused consumers.

Conclusion

The Margarine and Shortening Market is driven by health trends and bakery demand. Plant-based products and retail dominance fuel economic contributions through job creation and agricultural support. Businesses must innovate and target emerging markets to stay competitive. With strong regional growth, particularly in North America and Asia-Pacific, the market is poised for sustained expansion, meeting evolving consumer needs.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)