Table of Contents

Overview

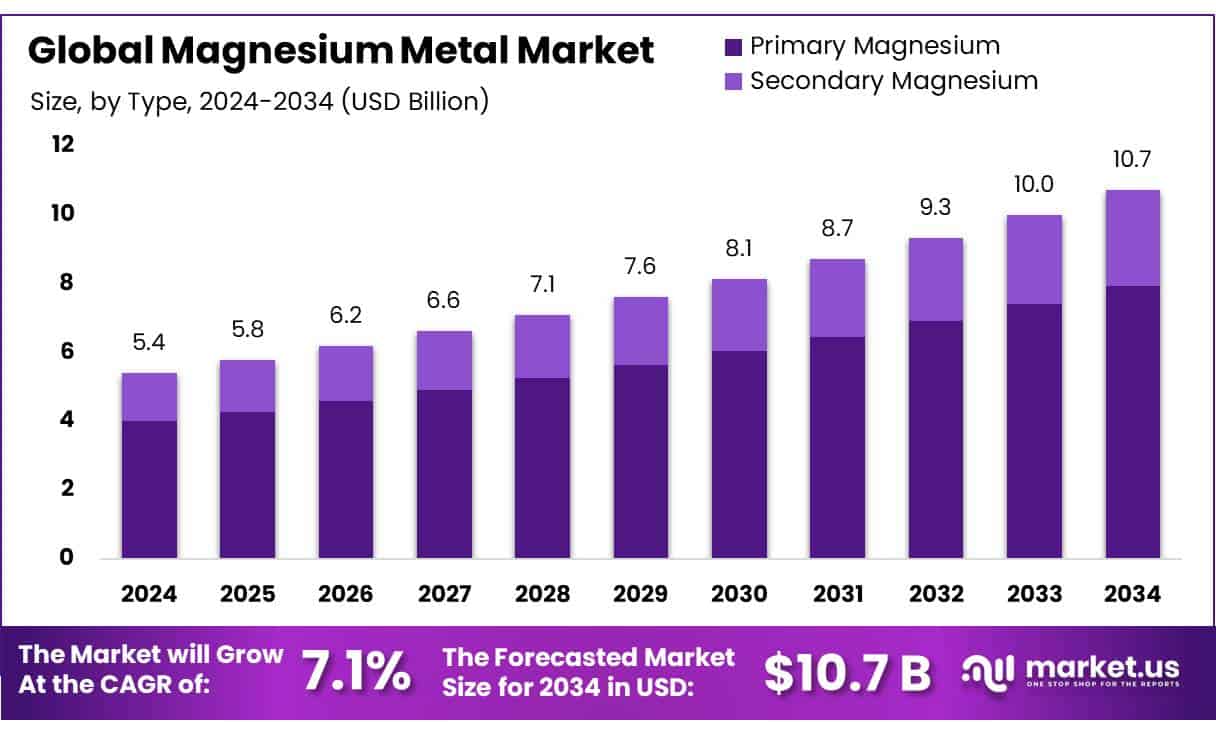

New York, NY – July 22, 2025 – The Global Magnesium Metal Market is set for strong growth, with its size expected to jump from USD 5.4 billion in 2024 to around USD 10.7 billion by 2034, growing at a CAGR of 7.1% from 2025 to 2034.

The European Union’s Critical Raw Materials Act, effective May 2024, classifies magnesium as a strategic material. It mandates that by 2030, the EU should domestically mine 10% of its critical mineral needs, process 40%, and recycle 15%. As part of this strategy, Romania awarded a mining concession to Verde Magnesium, a Bucharest-based company supported by U.S. investor Amerocap.

The company plans to invest $1 billion to revive a dormant magnesium mine near Oradea, targeting an annual production of 90,000 tonnes. This output would meet half of the EU’s magnesium demand, strengthening supply chain resilience and supporting the green transition. Global primary magnesium production in 2024 was approximately 940,000 tonnes, down 15% from 2022.

Key Takeaways

- Magnesium Metal Market size is expected to be worth around USD 10.7 Billion by 2034, from USD 5.4 Billion in 2024, growing at a CAGR of 7.1%.

- Primary Magnesium held a dominant market position, capturing more than a 73.3% share of the global magnesium metal market.

- Pidgeon held a dominant market position, capturing more than a 76.4% share of the global magnesium metal market.

- Aluminum Alloys held a dominant market position, capturing more than a 48.2% share of the global magnesium metal market.

- Automotive held a dominant market position, capturing more than a 42.2% share of the global magnesium metal market.

- Asia-Pacific (APAC) region held a dominant position in the global magnesium metal market, accounting for 47.2% of total market share, which translated to a valuation of approximately USD 2.5 billion.

How Growth is Impacting the Economy

The Magnesium Metal Market’s growth significantly influences the global economy. Its rising demand in automotive and aerospace sectors, particularly for lightweight components, boosts manufacturing in countries like China and India, enhancing industrial output and job creation. In 2024, the market supported economic activity by increasing production capacities, with companies like Nanjing Yunhai expanding through acquisitions.

The shift toward electric vehicles amplifies magnesium’s role, reducing vehicle weight and improving fuel efficiency, which aligns with emission regulations. Sustainable production methods reduce environmental costs, fostering economic stability. However, high corrosion rates and mining concerns pose challenges, potentially increasing costs and affecting economic scalability. Overall, the market drives innovation, infrastructure development, and economic growth in emerging economies.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/magnesium-metal-market/request-sample/

Strategies for Businesses

Businesses in the magnesium metal market should focus on strategic partnerships with automotive and aerospace manufacturers to develop innovative alloys, enhancing product applications. Investing in R&D for sustainable extraction and recycling technologies can reduce costs and meet environmental regulations. Vertical integration across the supply chain ensures cost control and supply security. Expanding into emerging markets like India and China, where infrastructure growth is rapid, offers significant opportunities.

Report Scope

| Market Value (2024) | USD 5.4 Billion |

| Forecast Revenue (2034) | USD 10.7 Billion |

| CAGR (2025-2034) | 7.1% |

| Segments Covered | By Type (Primary Magnesium, Secondary Magnesium), By Process (Pidgeon, Electrolytic, Recycling), By Application (Aluminum Alloys, Die Casting, Iron And Steel Making, Metal Reduction, Others), By End-use (Automotive, Aerospace And Defense, Building And Construction, Packaging, Medical And Healthcare, Electronics, Heavy Industry, Others) |

| Competitive Landscape | Shanxi Yinguang Huasheng Magnesium Industry, US Magnesium LLC, Tongxiang Magnesium (Shanghai), Dead Sea Magnesium [DSM], Latrobe Magnesium Limited, VSMPO-AVISMA, RIMA Industrial, Shanxi Bada Magnesium, Esan, Western Magnesium Corporation, Southern Magnesium & Chemicals Limited (SMCL), OJSC SMZ, Baowu Magnesium, West High Yield Resources, Other Key Players |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=151502

Key Market Segments

By Type

In 2024, primary magnesium dominated the global magnesium metal market, securing a 73.3% share. Its widespread use in structural alloys, die casting, and aluminum alloying fuels this lead, driven by the need for high-purity inputs. Produced from raw materials like dolomite or magnesite via energy-intensive methods such as the Pidgeon process or electrolytic reduction, primary magnesium is heavily supplied by China, the global leader in production.

The automotive industry relies on it for lightweight components to enhance fuel efficiency, while aerospace benefits from its superior strength-to-weight ratio. With increasing global focus on lightweight materials and stricter regulations on fuel efficiency and emissions, demand for primary magnesium remained robust in 2024 and is projected to grow into 2025.

By Process

The Pidgeon process led the global magnesium metal market in 2024 with a 76.4% share, primarily due to its widespread adoption in China, which accounts for over 85% of global magnesium output. This thermal reduction method, using dolomite and ferrosilicon in a vacuum, is favored for its low setup costs, accessible technology, and abundant raw material availability.

Despite its high energy consumption and carbon emissions—approximately 37 kg of CO₂ per kg of magnesium produced it remains dominant in regions with lenient environmental regulations. While global pressure for sustainable manufacturing grows, the Pidgeon process’s cost efficiency and established infrastructure sustained its market leadership in 2024, though cleaner alternatives may gain traction in the future.

By Application

In 2024, aluminum alloys captured a 48.2% share of the global magnesium metal market, driven by magnesium’s role as an alloying element to enhance aluminum’s strength, corrosion resistance, and machinability. These alloys are critical in transportation, construction, and packaging, particularly in automotive and aerospace sectors, where they reduce weight while maintaining structural integrity.

The shift toward electric vehicles and lightweight mobility solutions has amplified demand, as has the construction industry’s use of aluminum-magnesium alloys in cladding, roofing, and structural frames. With global infrastructure growth and stringent fuel efficiency standards, aluminum alloys maintained their lead in 2024 and are expected to remain vital into 2025.

By End-Use

The automotive industry led the global magnesium metal market in 2024, holding a 42.2% share. Magnesium’s low density 33% lighter than aluminum makes it ideal for lightweight components like gearboxes, steering wheels, seat frames, engine blocks, and transmission cases, improving fuel economy and extending electric vehicle battery range.

Stricter global emission and efficiency regulations, combined with the rise in electric vehicle adoption, have driven magnesium use among both traditional automakers and EV startups. This trend, fueled by the demand for cleaner and more efficient mobility solutions, kept the automotive sector at the forefront in 2024 and is expected to continue into 2025.

Regional Analysis

In 2024, the Asia-Pacific region dominated the global magnesium metal market, accounting for a 47.2% share, valued at approximately USD 2.5 billion. China, the world’s top producer and exporter, supplies over 85% of global primary magnesium, leveraging abundant raw materials, cost-effective labor, and extensive smelting infrastructure, primarily through the Pidgeon process.

Countries like India, Japan, and South Korea further drive growth, using magnesium in automotive, aerospace, electronics, and construction. Japan and South Korea, in particular, rely on magnesium for die casting in lightweight vehicles and electronic components. Rising electric vehicle demand and energy-efficient transport, alongside government support for decarbonization, bolstered the region’s market leadership in 2024.

Recent Developments

1. Shanxi Yinguang Huasheng Magnesium Industry Co., LTD

- Shanxi Yinguang Huasheng, a leading Chinese magnesium producer, has expanded its production capacity to meet growing global demand. The company focuses on high-purity magnesium for aerospace and automotive industries, investing in eco-friendly smelting technologies to reduce carbon emissions. Recent partnerships with European automakers aim to supply lightweight magnesium alloys for electric vehicles (EVs).

2. US Magnesium LLC

- US Magnesium, the sole U.S. producer of primary magnesium, has increased output to support domestic supply chains amid rising demand. The company is investing in renewable energy to power its operations, aligning with sustainability goals. Recent contracts with defense and aerospace firms highlight its role in securing critical materials for national security applications.

3. Tongxiang Magnesium (Shanghai) Co., Ltd.

- Tongxiang Magnesium has introduced new high-performance magnesium alloys for 3D printing and electronics, targeting the EV and consumer electronics markets. The company recently secured patents for corrosion-resistant magnesium coatings, enhancing durability in automotive parts. Expansion into Southeast Asia aims to capture growing industrial demand.

4. Dead Sea Magnesium [DSM] Ltd

- DSM, an Israel-based producer, has launched a new recycling initiative to recover magnesium from industrial waste, reducing environmental impact. The company is collaborating with European battery manufacturers to develop magnesium-based energy storage solutions. Upgraded production facilities have boosted output.

5. Latrobe Magnesium Limited

- Australia’s Latrobe Magnesium is pioneering a low-emission extraction process from fly ash, a byproduct of coal power plants. A recent pilot plant success has attracted government funding for full-scale production.

Conclusion

The Magnesium Metal Market’s growth, driven by demand for lightweight materials and sustainable practices, is reshaping industries and economies. It offers opportunities for innovation and expansion, particularly in Asia-Pacific. Businesses leveraging strategic partnerships and advanced technologies can thrive in this dynamic market. However, challenges like corrosion and mining impacts must be addressed to ensure sustained growth.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)