Table of Contents

Overview

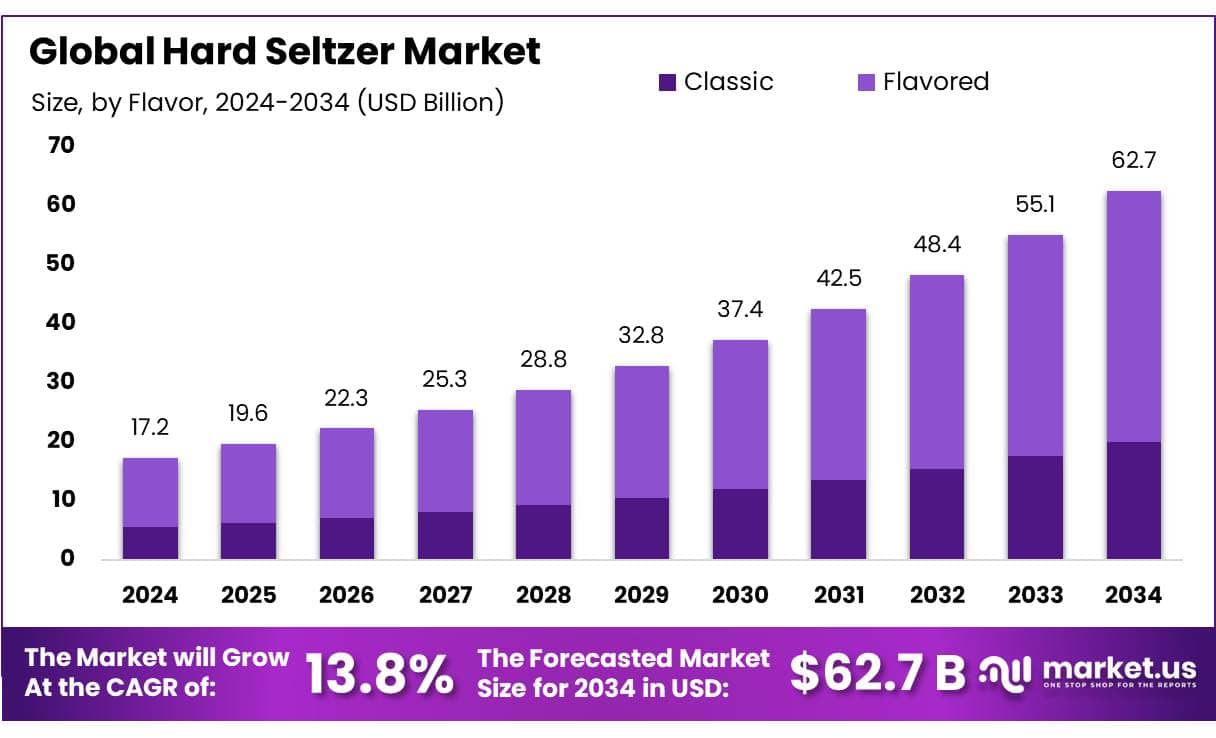

New York, NY – August 25, 2025 – The global hard seltzer market is projected to grow significantly, reaching an estimated USD 62.7 billion by 2034 from USD 17.2 billion in 2024, at a CAGR of 13.8% during the forecast period. Hard seltzer, a blend of carbonated water, alcohol, and fruit flavoring, has gained popularity for its low-calorie content and crisp, refreshing taste. Originally trending in the United States, this beverage category is now gaining global appeal, especially among health-conscious consumers looking for lighter alcoholic options.

The market’s rise is largely fueled by shifting consumer preferences toward healthier drinking alternatives. The United States continues to lead, with the Alcohol and Tobacco Tax and Trade Bureau reporting sales of over $4.5 billion in 2022 a 130% jump from 2020. This growth pattern is now reflected across Europe and Asia-Pacific, where demand for similar beverages is rising. Major beverage companies such as Anheuser-Busch InBev and Molson Coors are responding to the trend by diversifying their product lines with multiple hard seltzer offerings, accelerating the category’s momentum.

The market’s rise is largely fueled by shifting consumer preferences toward healthier drinking alternatives. The United States continues to lead, with the Alcohol and Tobacco Tax and Trade Bureau reporting sales of over $4.5 billion in 2022 a 130% jump from 2020. This growth pattern is now reflected across Europe and Asia-Pacific, where demand for similar beverages is rising. Major beverage companies such as Anheuser-Busch InBev and Molson Coors are responding to the trend by diversifying their product lines with multiple hard seltzer offerings, accelerating the category’s momentum.

Regulatory support has also played a crucial role in driving market growth. Government initiatives that promote the production of low-alcohol beverages, such as recent changes in excise duty structures within the European Union, have made it more cost-effective to produce these drinks. Additionally, U.S. government subsidies for small-scale brewers and incentives for sustainable manufacturing practices are encouraging new entrants into the market, further boosting innovation and expansion within the hard seltzer sector.

Key Takeaways

- The global hard seltzer market is projected to grow from USD 17.2 billion in 2024 to approximately USD 62.7 billion by 2034, expanding at a strong CAGR of 13.8%.

- Products with an alcohol by volume (ABV) between 2.9% and 4.9% held a dominant position, accounting for over 62.4% of the total market share.

- Metal cans stood out as the most popular packaging format, capturing more than 66.4% of the market.

- Flavored hard seltzers continued to lead in consumer preference, representing a significant 67.2% of the overall market.

- Off-trade distribution channels, such as supermarkets and retail stores, dominated the market with a share exceeding 73.4%.

- North America remained the largest regional market, contributing approximately 57.3% of global sales, equivalent to around USD 9.8 billion.

➤ For a deeper understanding, click on the sample report link: https://market.us/report/hard-seltzer-market/free-sample/

Report Scope

| Market Value (2024) | USD 17.2 Billion |

| Forecast Revenue (2034) | USD 62.7 Billion |

| CAGR (2025-2034) | 13.8% |

| Segments Covered | By ABV Content (Upto 2.9%, 2.9% to 4.9%, Above 4.9%), By Packaging Type (Glass Bottles, Metal Cans, Others), By Flavor (Classic, Flavored, Black Cherry, Lime, Ruby Grapefruit, Mango, Raspberry, Others), By Distribution Channel (Off-trade, On-trade) |

| Competitive Landscape | Brewery, Bud Light Seltzer, Carlsberg Group, Constellation Brands, Inc., Corona Seltzer, Heineken N.V., Henry’s, Kopparberg, Mark Anthony Brands International, Nauti Seltzer, Nutrl, Oskar Blues, Polar, San Juan Seltzer, Inc., Smirnoff, Spiked Seltzer, The Boston Beer Company, The Coca-Cola Company, Truly, Vizzy Hard Seltzer, White Claw |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=144767

Key Market Segments

1. By ABV Content

- In 2024, hard seltzers with an alcohol by volume (ABV) ranging from 2.9% to 4.9% led the market, accounting for over 62.4% of total sales. This strong performance reflects the rising demand for lighter alcoholic beverages that offer a smooth and enjoyable drinking experience without being too strong. These low-alcohol options are especially popular among health-conscious consumers who prefer moderation while still enjoying social and flavorful drinks. The growing focus on wellness and mindful drinking habits continues to drive this segment’s popularity, positioning it for steady growth into 2025.

2. By Packaging Type

- Metal cans emerged as the leading packaging format in the hard seltzer market in 2024, securing over 66.4% of the market share. Their dominance is tied to several practical advantages such as portability, recyclability, and freshness retention. These cans are lightweight, easy to carry, and ideal for on-the-go consumption, making them a favorite among active and eco-conscious consumers. With sustainability increasingly influencing purchasing behavior, metal cans are expected to maintain their position as the preferred packaging solution for hard seltzers.

3. By Flavor

- Flavored hard seltzers continued to dominate the market in 2024, holding a substantial 67.2% share. Their success stems from consumers’ desire for variety and the ability to choose from a wide range of unique and familiar flavor profiles. Whether it’s tropical fruits, citrus blends, or cocktail-inspired infusions, flavored options offer a customizable and exciting drinking experience. This ongoing demand for new and creative tastes encourages manufacturers to keep innovating, ensuring the segment remains a major driver of market growth.

4. By Distribution Channel

- Off-trade channels, such as supermarkets, liquor stores, and online platforms, captured over 73.4% of the hard seltzer market share in 2024. Their strong presence is fueled by the convenience and variety they offer, allowing consumers to easily purchase their favorite brands in bulk for at-home consumption. These channels also support discovery, enabling shoppers to try different flavors and brands at their own pace. As more people continue to enjoy hard seltzers in casual and private settings, off-trade distribution is expected to remain the dominant sales avenue.

Regional Analysis

- In 2024, North America held a dominant position in the global hard seltzer market, accounting for 57.3% of the total share, which translates to approximately $9.8 billion in sales. This stronghold is largely due to regional market dynamics and evolving consumer preferences that favor hard seltzers’ unique attributes.

- One of the primary factors driving this growth is the increasing demand for low-calorie, low-sugar alcoholic beverages—characteristics that hard seltzers naturally provide. These products are especially popular among health-conscious millennials and Gen Z consumers who value wellness while still enjoying social and recreational experiences. The widespread focus on healthier living in North America continues to significantly shape beverage consumption patterns.

- Additionally, the U.S. market, in particular, has seen a surge in breweries and beverage companies introducing a wide range of hard seltzer offerings. Innovations in flavor, organic ingredients, and sustainable packaging have helped brands meet the growing demand for environmentally friendly and health-forward products. Furthermore, North America’s extensive and efficient distribution network spanning supermarkets, convenience stores, and online platforms—ensures that consumers have easy and consistent access to a diverse selection of hard seltzers, reinforcing the region’s market leadership.

Top Use Cases

- Product Development & Innovation: Market research helps identify trends like low‑calorie, flavored seltzers or spirit‑based variants such as vodka or tequila seltzers. Brands can develop new beverage offerings matching consumer demand for wellness, taste variety, and novelty such as limited‑edition flavors or organic ingredients to capture attention and differentiate from competition.

- Packaging Strategy & Sustainability: By tracking packaging preferences such as the dominance of metal cans and growing interest in eco‑friendly formats companies can optimize packaging choices and messaging. Insights on recyclability, portability, and fresh taste retention guide packaging design and communication that align with values of environmentally conscious consumers.

- Distribution Channel Optimization: Data on off‑trade vs on‑trade sales helps brands allocate resources effectively. For example, stronger performance in supermarkets, liquor stores, and online retail may lead brands to boost retail shelf presence, promotions or direct‑to‑consumer options, while fine‑tuning on‑premise strategies for bars and events where visibility also matters.

- Marketing & Consumer Targeting: Insight into demographics such as health‑conscious millennials and Gen Z drinkers enables tailored marketing campaigns via social media, influencer partnerships, and content marketing. Messaging around “low‑sugar,” “mindful drinking,” and gender‑neutral branding attracts young, socially active consumers and supports deeper brand affinity.

- Market Entry & Regional Expansion: Analyzing regional consumption patterns—for instance, North America’s dominance guides expansion planning. Brands can prioritize regions with health trends and ready‑to‑drink infrastructure, adapt flavor or ABV offerings to local tastes, and select appropriate partners or distribution models during international launch phases.

- Competitive Benchmarking & Pricing: By comparing performance of major competitors (e.g. White Claw, Truly, High Noon) in terms of flavor variety, ABV levels, and pricing, companies can position their products strategically. Benchmarking enables informed pricing, feature differentiation, and positioning to compete on taste, health, and brand image.

Recent Developments

1. Brewery (Anheuser‑Busch / Bud Light Seltzer)

- In 2025, Anheuser‑Busch continues expanding its “beyond‑beer” capabilities, investing approximately $16 million in its Houston brewery. These upgrades enhance production of RTD beverages like Bud Light Seltzer and the vodka‑based NÜTRL, including scaling 25‑oz can output and improving water conservation and emissions controls

2. Bud Light Seltzer

- Bud Light Seltzer remains part of AB InBev’s strategic push into hard seltzer, supported by facility investments and capacity expansion to meet growing demand (especially for larger format cans and flavored variants) . AB InBev markets the product under its broader portfolio that includes RTD lines like Cutwater and NÜTRL.

3. Carlsberg Group

- In July 2024 Carlsberg acquired Britvic plc (completed January 17, 2025), forming Carlsberg Britvic in the UK. This unified entity spans beer and soft‑drink brands and supports future RTD and seltzer innovation through an expanded portfolio and supply chain. Carlsberg also has launched Nordic Hard Seltzer products in selected European markets, targeting health‑conscious consumers via low‑calorie, gluten‑free RTDs

4. Constellation Brands, Inc. (Corona Seltzer)

- Constellation added Corona Seltzer “Seltzerita”, a 6 % ABV limited‑edition variant (130 calories, 4 g carbs) to its Corona Hard Seltzer portfolio . A U.S. appeals court reaffirmed that Corona Hard Seltzer falls under Constellation’s brand licensing (not AB InBev’s), clearing legal doubts around its distribution rights

Conclusion

The hard seltzer market continues to show strong growth potential, driven by evolving consumer preferences and ongoing innovation from major beverage companies. Brands like Bud Light Seltzer are working to clearly position themselves in the market, emphasizing their identity as true hard seltzers. Constellation Brands is expanding its product line with unique offerings like Seltzerita, targeting consumers seeking bolder flavors. At the same time, companies like Anheuser-Busch are investing in vodka-based alternatives such as NÜTRL to diversify their ready-to-drink portfolios. These strategic moves, combined with a focus on health-conscious ingredients and convenient packaging, indicate that hard seltzers will remain a popular choice in the global beverage landscape.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)