Table of Contents

Overview

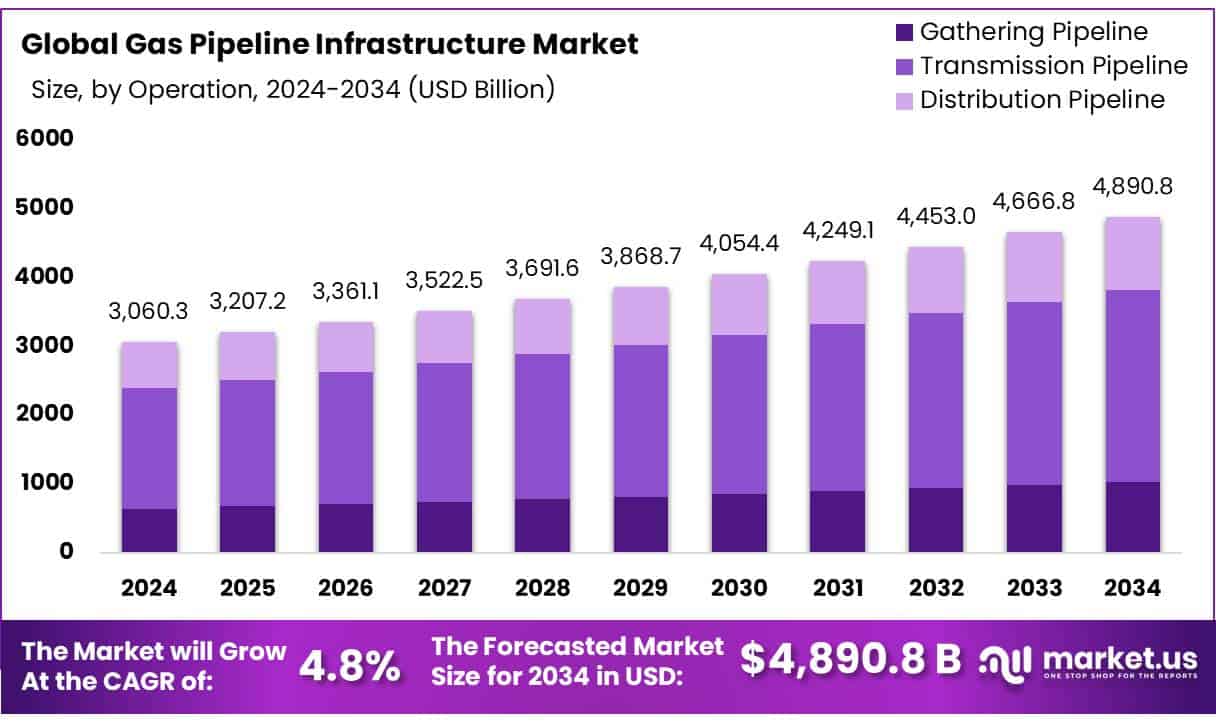

New York, NY – August 19, 2025 – The Global Gas Pipeline Infrastructure Market is projected to grow from USD 3,060.3 billion in 2024 to USD 4,890.8 billion by 2034, with a CAGR of 4.8% during the 2025–2034 forecast period. In 2024, North America led the market, holding a 48.3% share with USD 1,478.1 billion in revenue.

Gas pipeline infrastructure includes transmission and distribution systems that transport natural gas from production sites to end-use markets. This network consists of high-pressure, long-distance pipelines, compressors and metering stations, and cross-border interconnections. In the U.S., 2024 pipeline projects added about 6.5 billion cubic feet per day (Bcf/d) of takeaway capacity in regions like Appalachia, Haynesville, Permian, and Eagle Ford, with a total new capacity of 17.8 Bcf/d, including interstate and LNG export-linked pipelines, according to the U.S. Energy Information Administration.

Rising energy demand, especially in Asia and industrializing regions, is fueling infrastructure growth. Shell predicts global LNG demand will increase from 407 million tonnes in 2023 to 630–718 million tonnes, driven primarily by India and China. China’s gas consumption is expected to hit 425 billion cubic meters (bcm) in 2024, with imports (pipeline and LNG) up 17.4% year-on-year to 54.28 million tonnes in the first five months of 2024.

India’s “One Nation, One Gas Grid” initiative aims to expand the pipeline network to 34,500 kilometers by 2025, backed by a $67 billion investment in the natural gas sector over the next five to six years. Additionally, city gas distribution (CGD) projects are advancing. For example, in Coimbatore, Indian Oil Corporation Limited (IOCL) has laid 103 kilometers of underground pipelines, serving 4,000 residents with piped natural gas (PNG) and targeting 300,000 connections. In Chennai, THINK Gas is extending PNG to 20,000 homes, with efforts to streamline onboarding and lower costs.

Key Takeaways

- Gas Pipeline Infrastructure Market size is expected to be worth around USD 4890.8 Billion by 2034, from USD 3060.3 Billion in 2024, growing at a CAGR of 4.8%.

- Transmission Pipeline held a dominant market position, capturing more than a 57.2% share in the global gas pipeline infrastructure market.

- Large diameter pipelines (24 inches or more) held a dominant market position, capturing more than a 51.8% share in the global gas pipeline infrastructure market.

- High (above 500 psi) held a dominant market position, capturing more than a 56.6% share in the gas pipeline infrastructure market.

- Compressor Station held a dominant market position, capturing more than a 46.9% share in the gas pipeline infrastructure market.

- Onshore held a dominant market position, capturing more than an 82.4% share in the global gas pipeline infrastructure market.

- North America emerged as the leading region in the gas pipeline infrastructure market, accounting for approximately 48.3% of the total global market value, equivalent to US$1,478.1 billion.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/gas-pipeline-infrastructure-market/request-sample/

Report Scope

| Market Value (2024) | USD 3060.3 Billion |

| Forecast Revenue (2034) | USD 4890.8 Billion |

| CAGR (2025-2034) | 4.8% |

| Segments Covered | By Operation (Gathering Pipeline, Transmission Pipeline, Distribution Pipeline), By Diameter (Small (less than 12 inches), Medium (12 to 24 inches), Large (24 inches or more)), By Pressure (Low (less than 100 psi), Medium (100 to 500 psi), High (above 500 psi)), By Application (Compressor Station, Metering Station, Orthers), By Location (Onshore, Offshore) |

| Competitive Landscape | Enbridge Inc., Gazprom, TransCanada Pipelines Limited, Kinder Morgan, Pembina Gas Infrastructure, Saipem, Enagás S.A., Bechtel Corporation, Assam Gas Company Ltd., McDermott |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=154733

Key Market Segments

By Operation Analysis

In 2024, transmission pipelines commanded a 57.2% share of the global gas pipeline infrastructure market, driven by the critical need to transport natural gas over long distances from production basins to urban and industrial hubs. These high-capacity pipelines are the backbone of national and cross-border gas supply networks, ensuring energy security and facilitating global gas trade.

The expansion of LNG terminals and rising gas consumption in emerging economies amplified the demand for transmission systems in 2024. Projects like the Trans Adriatic Pipeline and Power of Siberia, coupled with strong policy support and investments from public and private sectors, further solidified their dominance. This trend is expected to continue into 2025 as infrastructure funding sustains growth.

By Diameter Analysis

Large diameter pipelines (24 inches or greater) captured a 51.8% share of the market in 2024, driven by their ability to transport large gas volumes over long distances efficiently. Used primarily in national trunk lines and cross-border projects, these pipelines reduce pressure loss and the need for frequent compressor stations, offering cost-effective solutions for long routes.

The surge in LNG import terminals and gas-fired power plants, particularly in North America, Europe, and the Asia-Pacific, boosted demand for large pipelines in 2024. As energy-intensive economies continue to expand infrastructure into 2025, large-diameter pipelines will remain central to meeting high-volume transmission demands.

By Pressure Analysis

High-pressure pipelines (above 500 psi) held a 56.6% share of the market in 2024, favored for their efficiency in transporting large gas volumes across vast distances with minimal compression needs. These pipelines are integral to major transmission networks, particularly for inter-regional and cross-border gas movement.

Their ability to maintain consistent flow and reduce transmission losses makes them ideal for national energy grids and large-scale distribution systems. Increased industrial gas demand and urban pipeline expansions in 2024 further drove their prominence. As the global gas trade and LNG distribution grow in 2025, high-pressure pipelines will remain critical for performance and safety.

By Application Analysis

Compressor stations captured a 46.9% share of the market in 2024, playing a vital role in maintaining gas pressure and flow across long-distance pipelines. These stations are crucial for ensuring efficient gas movement over hundreds or thousands of kilometers, counteracting natural pressure drops.

The global rise in high-capacity transmission pipelines in 2024 increased the need for compressor stations. As infrastructure upgrades and expansions continue into 2025 across both developed and developing regions, compressor stations will remain essential for operational efficiency in gas delivery networks.

By Location Analysis

Onshore pipelines held an 82.4% share of the market in 2024, attributed to their cost-effective installation and maintenance compared to offshore systems. These pipelines form the backbone of domestic gas transmission and distribution, connecting production sites to cities, industrial zones, and power plants.

Their accessibility facilitates easier monitoring, repairs, and integration with existing infrastructure. In 2024, the expansion of regional and interstate transmission corridors, particularly in North America, Asia, and Europe, reinforced onshore pipelines’ dominance. As energy demand grows and infrastructure projects advance in 2025, onshore pipelines will continue to lead global gas delivery.

Regional Analysis

In 2024, North America dominated the global gas pipeline infrastructure market, holding a 48.3% share valued at USD 1,478.1 billion. This leadership stems from the region’s extensive pipeline network, particularly in the U.S. and Canada, which spans over 305,000 miles of interstate and intrastate pipelines.

Major operators like TC Energy, managing over 91,900 km of pipelines and transporting 25% of North America’s daily gas demand, and Enbridge, operating 38,375 km of pipelines delivering 16.2 billion cubic feet per day, underpin the region’s robust infrastructure. The mature and dense transmission and distribution systems continue to drive North America’s market dominance into 2025.

Top Use Cases

- Energy Supply for Urban Areas: Gas pipelines deliver natural gas to cities for heating, cooking, and electricity. They connect production sites to urban centers, ensuring a steady energy supply. With rising urban demand, pipelines support reliable access to clean energy, reducing dependence on coal and oil, and meeting residential and commercial needs efficiently.

- Industrial Power Generation: Pipelines transport natural gas to industries and power plants for electricity production. As a cleaner fuel, gas supports industrial growth while lowering emissions. Pipelines ensure a consistent supply to high-demand sectors like manufacturing and fertilizers, driving efficiency and sustainability in industrial operations across regions.

- LNG Export and Import: Gas pipelines link LNG terminals to global markets, enabling efficient export and import of liquefied natural gas. They connect production hubs to coastal terminals, supporting cross-border trade. This infrastructure is vital for energy security, especially in regions like the Asia-Pacific, where LNG demand is surging rapidly.

- Cross-Border Energy Trade: Pipelines facilitate international gas trade by connecting gas-rich regions to high-demand markets. Projects like the Trans Adriatic Pipeline enhance energy security by diversifying supply sources. These networks support stable gas flow across borders, fostering economic cooperation and meeting growing energy needs in multiple countries.

- Integration of Renewable Gases: Pipelines are being adapted to transport renewable gases like hydrogen and biogas. This supports the shift to cleaner energy by blending sustainable fuels into existing networks. Infrastructure upgrades enable pipelines to handle these gases, aligning with global decarbonization goals and enhancing the sustainability of gas distribution systems.

Recent Developments

1. Enbridge Inc.

Enbridge is advancing its BC Pipeline Expansion to enhance natural gas delivery in British Columbia, supporting LNG exports. The company is also investing in renewable natural gas (RNG) projects and hydrogen blending trials. Additionally, Enbridge secured regulatory approval for the T-South Expansion, increasing capacity.

2. Gazprom

Gazprom is focusing on the Power of Siberia 2 pipeline to supply China with 50 Bcm/year of gas, amid declining European demand due to geopolitical tensions. The company is also expanding its TurkStream pipeline to strengthen supply to Southern Europe and Turkey.

3. TC Energy (formerly TransCanada Pipelines)

TC Energy is progressing with its NGTL System Expansion in Alberta. The company also secured approval for the GTN XPress Project to upgrade pipelines in the U.S. Pacific Northwest. Additionally, TC Energy is exploring hydrogen-ready pipeline designs.

4. Kinder Morgan

Kinder Morgan is expanding its Tennessee Gas Pipeline (TGP) with the Evangeline Pass Project. The company is also investing in carbon capture and storage (CCS) alongside pipeline operations.

5. Pembina Pipeline Corporation

Pembina is advancing the Phase VIII Expansion of its Peace Pipeline system, increasing capacity. The company is also partnering on low-carbon LNG projects and exploring hydrogen integration in its infrastructure.

Conclusion

The Gas Pipeline Infrastructure Market is growing due to rising energy demand, cleaner fuel adoption, and technological advancements. Pipelines ensure reliable gas delivery for urban, industrial, and global trade needs while supporting renewable gas integration. As investments in onshore and transmission systems increase, the market will play a key role in energy security and sustainability.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)