Table of Contents

Overview

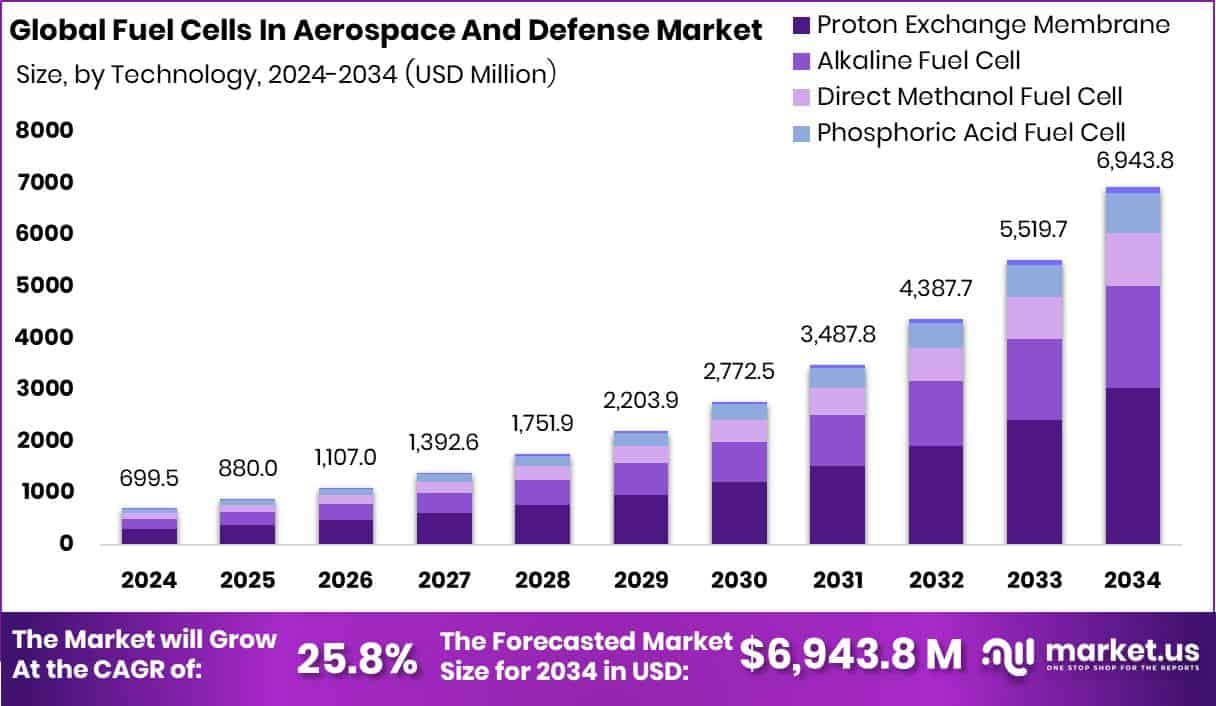

New York, NY – August 20, 2025 – The Global Fuel Cells in Aerospace and Defense Market is projected to grow significantly, reaching an estimated USD 6,943.8 million by 2034 from USD 699.5 million in 2024, with a robust CAGR of 25.8% from 2025 to 2034. North America leads the market, valued at USD 293.0 million, driven by substantial defense budgets and ongoing innovation.

Fuel cells are advanced energy systems that convert hydrogen or other fuels into electricity via electrochemical reactions. Their high efficiency, silent operation, low thermal signature, and minimal emissions make them ideal for military operations and next-generation aircraft. Unlike conventional combustion-based systems, fuel cells offer a cleaner, quieter alternative, supporting sustainability and stealth requirements in defense and aviation.

The market is propelled by a growing focus on clean energy and reducing fossil fuel dependency in aerospace and defense applications. Countries are prioritizing decarbonization in military and space programs, boosting fuel cell adoption for reliable onboard power. Their lightweight design and extended operational endurance compared to batteries make them ideal for unmanned systems, surveillance equipment, and auxiliary power units. Notably, Daimler Truck secured €226 million in government funding to advance fuel cell technology for trucks, highlighting broader investment trends.

Increasing demand for long-duration missions, where batteries are insufficient, is a key growth factor. Fuel cells provide continuous power for extended periods, making them suitable for remote or hostile environments. They also reduce logistical challenges by minimizing fuel transport needs. A £200 million hydrogen-from-waste facility in Thames Freeport exemplifies efforts to support fuel cell infrastructure.

Significant opportunities lie in integrating fuel cells into hybrid propulsion systems for both manned and unmanned aerial platforms. As space exploration and modern warfare evolve, fuel cells offer advantages in decentralized, lightweight, and scalable power systems. Industry developments, such as the University of Sheffield’s £1.5 million UK-backed initiative for Sustainable Aviation Fuel (SAF) and Turkey’s Akfen securing a €3.4 million grant for a mobile hydrogen refueling station, underscore the growing interest in fuel cell technology.

Key Takeaways

- The Global Fuel Cells in Aerospace and Defense Market is expected to be worth around USD 6,943.8 million by 2034, up from USD 699.5 million in 2024, and is projected to grow at a CAGR of 25.8% from 2025 to 2034.

- Proton Exchange Membrane technology dominates the market, capturing a 43.8% share in fuel cell systems.

- Fuel cells under 10 kW account for 36.2% of total installations in aerospace applications.

- Hydrogen remains the primary fuel source, representing 72.9% of total consumption in defense-related fuel cells.

- Auxiliary Power Units lead application-wise, contributing to 54.4% of total usage across the aerospace industry.

- Military end-users constitute 45.9% of the market, indicating strong adoption in defense and tactical operations.

- North America reached a market value of USD 293.0 million in 2024.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/fuel-cells-in-aerospace-and-defense-market/request-sample/

Report Scope

| Market Value (2024) | USD 699.5 Million |

| Forecast Revenue (2034) | USD 6,943.8 Million |

| CAGR (2025-2034) | 25.8% |

| Segments Covered | By Technology (Alkaline Fuel Cell, Direct Methanol Fuel Cell, Phosphoric Acid Fuel Cell, Proton Exchange Membrane, Solid Oxide Fuel Cell), By Power Rating (10 to 50 kW, 50 to 200 kW, Over 200 kW, Under 10 kW), By Fuel Type (Ammonia, Hydrogen, Methanol), By Application (Auxiliary Power Units, Backup Power, Primary Propulsion), By End User (Commercial Aerospace, Military, Space Agencies, Others) |

| Competitive Landscape | Advent Technologies, AFC Energy PLC, Australian Fuel Cells Pty Ltd., Ballard Power Systems, Inc., Bloom Energy Corporation, Cummins Inc., Doosan Fuel Cell Co., Ltd., ElringKlinger AG, FuelCell Energy, Inc., GenCell Ltd. |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=154782

Key Market Segments

By Technology Analysis

In 2024, Proton Exchange Membrane (PEM) fuel cells dominated the technology segment of the Fuel Cells in Aerospace and Defense Market, capturing a 43.8% share. PEM’s leadership stems from its high efficiency, compact design, and suitability for aerospace applications where weight and reliability are paramount. Operating at low temperatures with rapid start-up and high power density, PEM fuel cells are ideal for unmanned aerial vehicles (UAVs) and auxiliary power units (APUs) in military aircraft.

By Power Rating Analysis

In 2024, the under 10 kW segment led the power rating category with a 36.2% share. This dominance reflects the growing demand for compact, low-power fuel cells in lightweight applications like UAVs, small drones, and portable military equipment. The Under 10 kW range balances energy output and weight, offering mobility and efficiency for tactical scenarios requiring stealth and extended mission durations. The rise in electrification for aerospace missions and advanced surveillance systems further fuels demand.

By Fuel Type Analysis

Hydrogen fuel led the fuel type segment in 2024, commanding a 72.9% share. Its high energy density, clean combustion, and suitability for long-duration missions make it the preferred choice for aerospace and defense applications. Hydrogen’s zero-emission profile aligns with sustainability goals, supporting its use in UAVs, APUs, and other platforms. The significant market share reflects advancements in hydrogen storage and refueling infrastructure, enhancing practicality for military and aerospace use. Hydrogen’s scalability and efficiency solidify its role as the leading fuel type in mission-critical scenarios.

By Application Analysis

In 2024, APUs dominated the application segment with a 54.4% share, driven by their role as efficient, low-emission power sources for aircraft systems like lighting and avionics. Fuel cell-based APUs reduce reliance on main engines, offering quiet operation and low thermal signatures, which are critical for aerospace and defense. The focus on sustainability and compact, lightweight systems has accelerated their adoption. This segment’s dominance highlights fuel cells’ alignment with the demand for autonomous, clean energy solutions in modern aviation and military operations.

By End User Analysis

The military sector held a 45.9% share of the end-user segment in 2024, reflecting the growing integration of fuel cells in defense applications. Fuel cells power APUs, UAVs, and portable soldier systems, providing energy independence, reduced signatures, and extended mission endurance. The emphasis on clean energy and operational flexibility in remote or hostile environments drives adoption. This dominance underscores fuel cells’ strategic value in enhancing mission efficiency and sustainability in modern warfare.

Regional Analysis

In 2024, North America led the global market with a 41.9% share, valued at USD 293.0 million. This dominance is driven by advanced defense infrastructure, significant government funding for clean energy, and widespread adoption of fuel cells in military and aerospace applications. The region’s focus on long-endurance unmanned systems and technological innovation strengthens its position.

Europe shows growing interest in fuel cells for emission reduction and operational efficiency, while the Asia Pacific sees gradual adoption with rising defense budgets. The Middle East & Africa and Latin America are emerging markets with growth potential, but North America remains the global leader, setting the standard for fuel cell integration.

Top Use Cases

Powering Unmanned Aerial Vehicles (UAVs): Fuel cells provide long-lasting power for drones, enabling extended flight times for surveillance and reconnaissance. Their lightweight design and silent operation enhance stealth, making them ideal for military missions in remote areas where traditional batteries fall short.

Auxiliary Power Units (APUs) in Aircraft: Fuel cells power aircraft systems like lighting and avionics without relying on main engines. They offer quiet, low-emission energy, reducing environmental impact and improving efficiency for both military and commercial planes.

Portable Soldier Power Systems: Fuel cells supply lightweight, reliable energy for soldiers’ gear, such as radios and GPS devices. Their high energy density and reduced logistical needs make them perfect for long missions in challenging environments.

Silent Propulsion for Military Vehicles: Fuel cells enable quiet, low-heat propulsion for ground vehicles and drones, improving stealth in defense operations. This reduces detection risks and supports missions requiring minimal noise and thermal signatures.

Spacecraft Power Systems: Fuel cells provide efficient, continuous electricity for spacecraft, supporting critical systems in space exploration. Their eco-friendly nature and ability to use stored hydrogen make them a sustainable choice for long-duration missions.

Recent Developments

1. Advent Technologies

Advent Technologies is advancing its High-Temperature Proton Exchange Membrane (HT-PEM) fuel cells for unmanned aerial vehicles (UAVs) and defense applications. The company collaborates with the U.S. Department of Defense (DoD) to develop lightweight, durable fuel cell systems for extended mission durations. Advent’s M-Series fuel cells offer high efficiency and operate in extreme conditions, making them ideal for military use.

2. AFC Energy PLC

AFC Energy is focusing on hydrogen fuel cells for portable and off-grid power in defense. The company partnered with Extreme E to deploy fuel cells in harsh environments, demonstrating military potential. AFC’s S-Power systems provide silent, emissions-free power for field operations, reducing reliance on diesel generators. The UK Ministry of Defence is evaluating AFC’s technology for battlefield energy solutions.

3. Australian Fuel Cells Pty Ltd.

Australian Fuel Cells (AFCP) is developing solid oxide fuel cells (SOFCs) for aerospace auxiliary power units (APUs). Their Gennex technology offers high energy density for UAVs and electric aircraft. AFCP collaborates with defense agencies to integrate fuel cells into hybrid-electric propulsion systems, enhancing endurance and reducing emissions. Recent tests show promising results for long-endurance missions.

4. Ballard Power Systems, Inc.

Ballard is a leader in proton exchange membrane (PEM) fuel cells for aerospace and defense. The company supplies fuel cells for zero-emission UAVs and military ground vehicles. Ballard’s FCair system powers Airbus’ ZEROe hydrogen aircraft concept. The U.S. Army is testing Ballard’s HD PEM fuel cells for silent watch and reconnaissance missions.

5. Bloom Energy Corporation

Bloom Energy’s solid oxide fuel cells (SOFCs) are being adapted for aerospace applications, including electric aircraft and space missions. The company partnered with NASA to explore fuel cells for lunar and Martian habitats. Bloom’s Energy Servers provide resilient, off-grid power for military bases, reducing carbon footprints. The U.S. Air Force is testing Bloom’s systems for forward operating bases.

Conclusion

The Fuel Cells in Aerospace and Defense Market is rapidly growing due to the demand for clean, efficient, and stealthy energy solutions. Fuel cells offer long endurance, low emissions, and silent operation, making them ideal for UAVs, APUs, soldier systems, military vehicles, and spacecraft. Despite high costs and infrastructure challenges, ongoing innovations and government support are driving adoption, ensuring a sustainable future for aerospace and defense applications.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)