Table of Contents

Overview

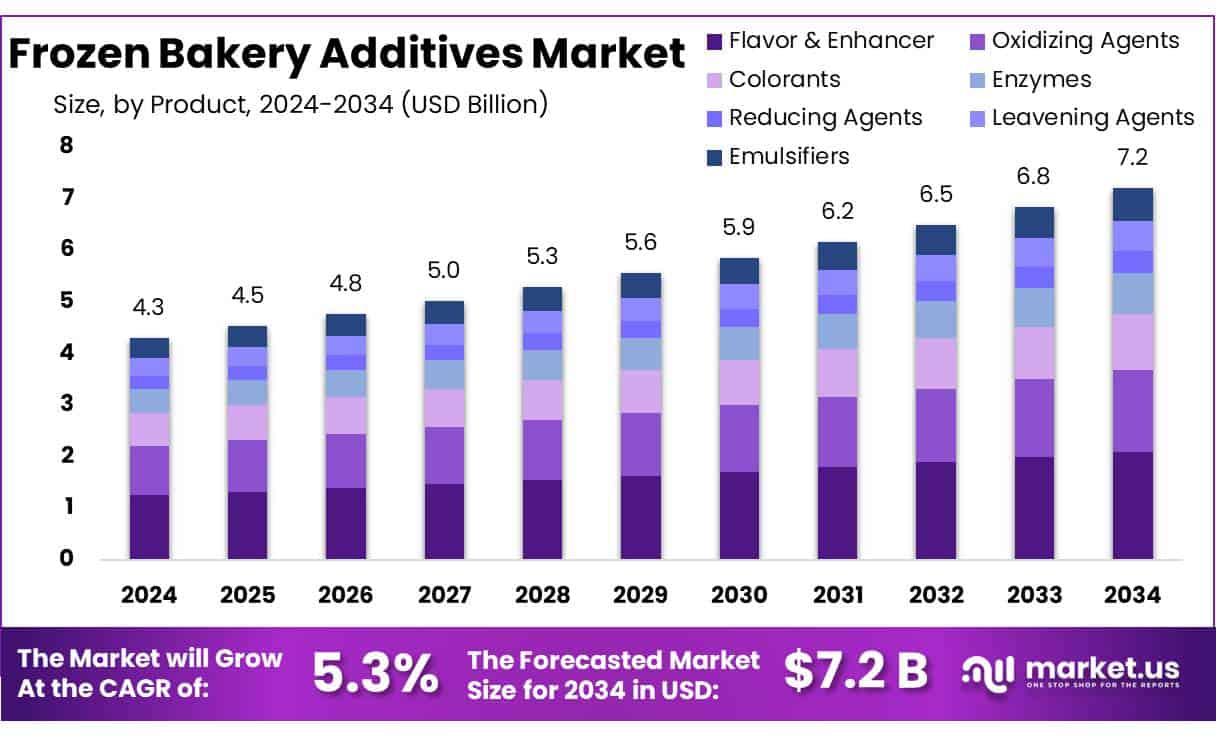

New York, NY – May 23, 2025 – The Global Frozen Bakery Additives Market is growing fast, driven by rising demand for convenient, ready-to-bake products. In 2024, the market was valued at USD 4.3 billion and is expected to reach USD 7.2 billion by 2034, growing at a 5.3% CAGR.

In 2024, Flavor Enhancers led the frozen bakery additives market, securing over 29.1% of the market share. This dominance stems from growing consumer demand for tastier frozen bakery products. Frozen Bread commanded over 29.4% of the frozen bakery additives market, reinforcing its strong market position. Its popularity is driven by consumer demand for convenient, consistent, and near-fresh bread options. Industrial Distribution channels dominated the frozen bakery additives market, capturing over 47.9% of the market share.

US Tariff Impact on Frozen Bakery Additives Market

U.S. trade policies have significantly disrupted supply chains for key baking ingredients. Tariffs on imports from Canada, Mexico, and China are projected to cost the industry USD 454 million in 2025, including USD 244 million from a 25% tariff on Canadian goods, USD 170 million from tariffs on Mexican imports, and USD 40 million from a 10% tariff on Chinese products. These tariffs are driving up costs for essentials like flour blends and sweeteners, straining businesses, workers, and consumers.

➤ Get More Detailed Insights about US Tariff Impact @ – https://market.us/report/global-frozen-bakery-additives-market/request-sample/

The situation intensified in early April 2025, when the Trump administration introduced a 125% tariff on certain Chinese imports to decrease reliance on foreign manufacturing. The Baking Industry is grappling with a critical labor shortage, projecting 53,500 unfilled roles in key sectors such as production, maintenance, engineering, equipment maintenance, and logistics. This deficit could result in severe economic impacts, including the loss of 148,000 jobs, USD 9.7 billion in wages, USD 36.2 billion in output, and USD 3.3 billion in tax revenues.

Key Takeaways

- Frozen Bakery Additives Market size is expected to be worth around USD 7.2 billion by 2034, from USD 4.3 billion in 2024, growing at a CAGR of 5.3%.

- Flavor enhancers in the frozen bakery additives market held a dominant position, capturing more than a 29.1% share.

- Frozen bread maintained a dominant market position in the frozen bakery additives sector, capturing more than a 29.4% share.

- Industrial distribution channel held a dominant market position in the frozen bakery additives market, capturing more than a 47.9% share.

- Europe dominated the frozen bakery additives market, capturing more than 46.2% of the global share, valued at approximately USD 1.9 billion.

Analyst Viewpoint

The Frozen Bakery Additives Market offers compelling investment opportunities alongside significant risks. Rising consumer demand for convenient, ready-to-eat foods, especially in urban areas with fast-paced lifestyles, drives market growth. Investors may find potential in companies prioritizing clean-label and natural additives, reflecting the shift toward health-conscious consumption.

Consumer trends highlight a preference for frozen bakery products that balance convenience with health and wellness. Demand is growing for items featuring natural ingredients, minimal processing, and enhanced nutritional value. Technological innovations, such as enzyme-based solutions and natural emulsifiers, improve product texture and shelf life, appealing to health-focused consumers.

Evolving regulatory frameworks, with stricter food additive guidelines, require manufacturers to invest in R&D for compliant, consumer-friendly solutions. While the market holds strong growth potential, success hinges on navigating regulatory complexities and aligning with consumer preferences for healthier, natural products.

Report Scope

| Market Value (2024) | USD 4.3 Billion |

| Forecast Revenue (2034) | USD 7.2 Billion |

| CAGR (2025-2034) | 5.3% |

| Segments Covered | By Product (Port Wine, Vermouth, Sherry, Marsala, Madeira, Others), By Alcohol Content (Below 15%, 15% to 20%, Above 20%), By Distribution Channel (Pub, Bars and Restaurants, Internet Retailing, Liquor Stores, Supermarkets, Others) |

| Competitive Landscape | Archer Daniels Midland Company, Ashland, Associated British Foods Plc, Avebe, Cargill, Corbion, DowDuPont, DSM, Kerry Group, Lesaffre, Novozymes A/S, Palsgaard, Puratos, Tate Lyle PLC |

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)