Table of Contents

Overview

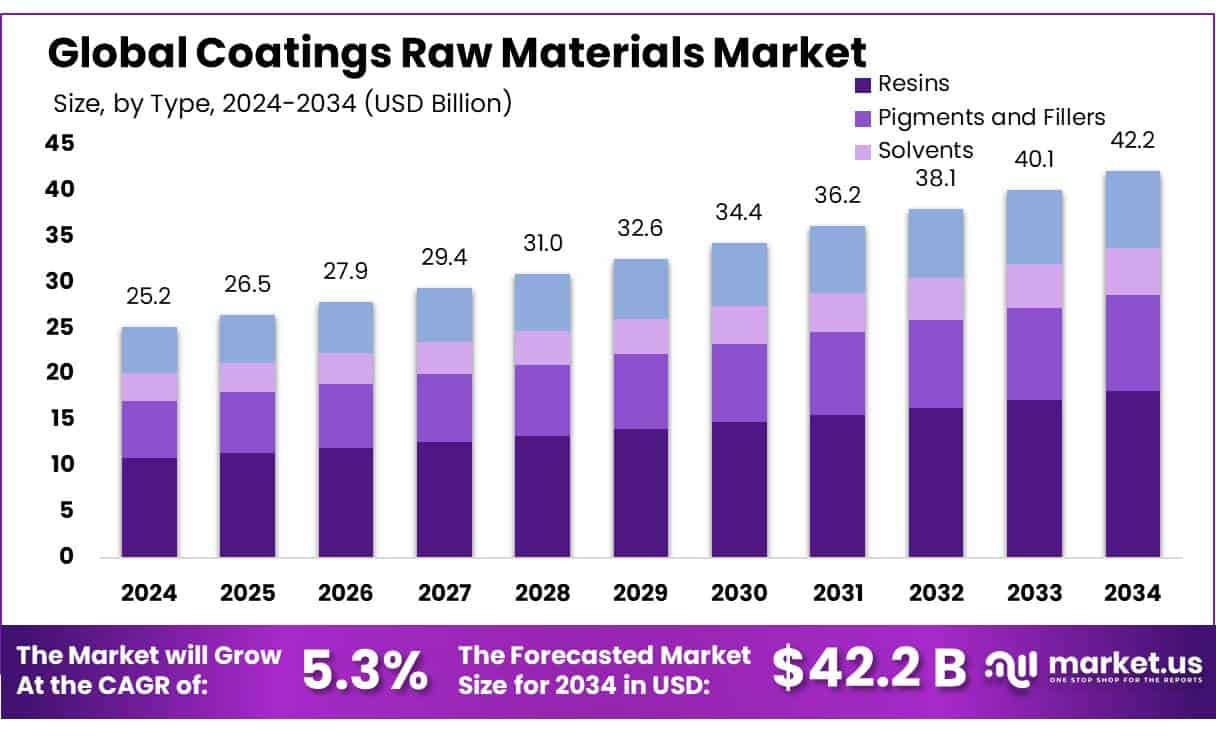

New York, NY – July 22, 2025 – The Global Coatings Raw Materials Market is set to grow significantly, reaching USD 42.2 billion by 2034, up from USD 25.2 billion in 2024, with a steady CAGR of 5.3% from 2025 to 2034.

The coatings raw materials market, valued at approximately USD 63.5 billion globally, supports a consumption volume of 34.3 million metric tons. Primary concentrate categories include synthetic polymer binders, pigment dispersions, and functional additives designed for viscosity control, adhesion, or biocidal properties.

These concentrates are formulated for later dilution by manufacturers to produce final paint and coating products. Key raw materials resins (e.g., acrylics, polyurethanes, alkyds), pigments (e.g., titanium dioxide), solvents (organic and water-based), and additives (e.g., rheology modifiers, UV stabilizers) are essential for coating performance, contributing to adhesion, durability, color, opacity, and application properties.

Fillers like calcium carbonate and talc further enhance texture and coverage. The coatings industry accounts for about 5% of the USD 4.5 trillion global chemicals market. Recent geopolitical and policy developments have significantly influenced both raw material and concentrate markets.

In March 2024, the U.S. Department of Energy invested USD 6 billion in industrial decarbonization, including chemical and materials processing, aiming to cut 14 million metric tons of CO2 emissions annually. In the European Union, the Critical Raw Materials Act targets strategic material self-sufficiency by 2030, mandating 10% domestic extraction, 40% processing, and 25% recycling of critical raw materials.

Key Takeaways

- Coatings Raw Materials Market size is expected to be worth around USD 42.2 Billion by 2034, from USD 25.2 Billion in 2024, growing at a CAGR of 5.3%.

- Resins held a dominant market position, capturing more than a 43.3% share in the global coatings raw materials market.

- Solvent-based held a dominant market position, capturing more than a 38.4% share in the coatings raw materials market.

- Building & Construction held a dominant market position, capturing more than a 28.3% share in the coatings raw materials market.

- Asia-Pacific (APAC) region held a dominant position in the global coatings raw materials market, accounting for more than 45.7% of the total share, with a market value of approximately USD 11.5 billion.

How Growth is Impacting the Economy

The Coatings Raw Materials Market’s growth significantly influences the global economy. The sector’s expansion, driven by demand in construction, automotive, and industrial applications, creates jobs, with the U.S. alone reporting employees in 2020. Infrastructure projects in emerging economies like China and India boost GDP, with China’s construction sector projected to grow.

The shift to sustainable coatings aligns with environmental policies, reducing VOC emissions and fostering green innovation. However, volatile raw material prices, particularly for petroleum-based feedstocks, challenge profitability, impacting production costs. Strategic partnerships and investments in R&D enhance economic resilience, supporting market stability and regional development.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/coatings-raw-materials-market/request-sample/

Strategies for Businesses

Businesses in the coatings raw materials market should prioritize sustainability, investing in low-VOC and bio-based materials to meet regulatory demands and consumer preferences. Forming strategic partnerships with suppliers and research institutions can enhance innovation and market access. Expanding into emerging markets like Asia-Pacific, where construction and automotive sectors thrive, offers growth opportunities. Leveraging AI and IoT for process optimization can improve efficiency and reduce costs. Additionally, businesses should mitigate raw material price volatility by diversifying supply chains and exploring alternative sourcing to ensure competitiveness and long-term profitability in a dynamic market.

Report Scope

| Market Value (2024) | USD 25.2 Billion |

| Forecast Revenue (2034) | USD 42.2 Billion |

| CAGR (2025-2034) | 5.3% |

| Segments Covered | By Type (Resins, Pigments and Fillers, Solvents, Additives), By Application (Solvent-based, Water-based, Powder Coatings, Radiation Curable Coatings), By End-use (Building And Construction, Oil And Gas, Aerospace, Marine, Industrial, Power Generation, Mining, Automotive, Others) |

| Competitive Landscape | BASF SE, Celanese Corporation, Allnex, Dow, Eastman Chemical, Evonik Industries AG, Huntsman Corporation, Lanxess AG, Momentive Performance Materials, Inc., W.R. Grace, et al., Cathay Industries, Heubach Group, Arkema Inc., Covestro, DIC Corporation, Cabot Corporation, Matsuo Sangyo Co., Ltd., Altana AG, Nouryon, Other Key Players |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=151440

Key Market Segments

By Type

Resins led the global coatings raw materials market in 2024, commanding a 43.3% share due to their critical role in protective and decorative coatings. As essential binding agents, resins like acrylic, epoxy, alkyd, polyurethane, and polyester provide adhesion, durability, and chemical resistance. The surge in demand for water-based resins, driven by stricter low-VOC regulations in North America and Europe, further bolstered their dominance.

By Application

Solvent-based coatings held a 38.4% market share in 2024, excelling in heavy-duty applications due to their resistance to abrasion, chemicals, and extreme temperatures. Widely used in automotive, marine, metal fabrication, and heavy machinery, these coatings remain favored for their reliability despite VOC-related regulatory pressures. While water-based and powder coatings gain ground, solvent-based systems are projected to maintain strong demand in 2025, particularly in developing regions where cost and infrastructure constraints persist.

By End-Use

The Building & Construction sector captured a 28.3% share in 2024, fueled by global demand for protective and decorative coatings in infrastructure projects. Growth in residential and commercial developments, especially in emerging economies, and renovation activities in developed regions drove this dominance. Acrylic and epoxy resins, pigments, and additives were key, meeting needs for durability, UV resistance, and environmental compliance. Energy-efficient coatings, like heat-reflective and insulating options, also saw increased adoption.

Regional Analysis

Asia-Pacific (APAC) dominated the market in 2024 with a 45.7% share, valued at USD 11.5 billion, driven by rapid urbanization, infrastructure growth, and industrial expansion in countries like China, India, Japan, and South Korea. China’s robust real estate, shipbuilding, and automotive sectors were major contributors. Low production costs and high domestic consumption made APAC a key supplier of resins, solvents, and pigments.

Regulatory pushes in Japan and South Korea accelerated the shift toward eco-friendly, water-based coatings. With strong foreign investments and a growing supply chain, APAC is poised to maintain its leadership in 2025, supported by rising demand in automotive and construction, particularly in Southeast and South Asia.

Recent Developments

1. BASF SE

- BASF has introduced JONCRYL HPX, a new acrylic resin for high-performance industrial coatings, offering better durability and sustainability. They also expanded their bio-based raw materials portfolio to meet eco-friendly demands. BASF is focusing on low-VOC and water-based solutions to comply with global environmental regulations.

2. Celanese Corporation

- Celanese launched ECOSURF EH surfactants, enhancing the performance of waterborne coatings. They also expanded vinyl acetate-ethylene (VAE) emulsion production to support sustainable coatings. Their innovations aim to improve adhesion and scrub resistance in architectural paints.

3. Allnex

- Allnex developed EBECRYL, a new range of UV-curable resins for industrial and automotive coatings, reducing energy consumption. They also introduced waterborne alkyds for eco-friendly wood coatings, aligning with stricter VOC regulations.

4. Dow

- Dow launched DOWSIL 3037, a silicone additive improving weatherability in architectural coatings. They also partnered to advance recyclable packaging coatings, supporting circular economy goals. Their innovations focus on high-performance, sustainable solutions.

5. Eastman Chemical

- Eastman introduced Tritan Renew, a sustainable copolyester for coatings, made from recycled materials. They also expanded cellulose esters production for low-VOC coatings, enhancing performance in automotive and industrial applications.

Conclusion

The Coatings Raw Materials Market is poised for robust growth, driven by urbanization, automotive demand, and sustainability trends. Its economic impact is profound, fostering job creation and infrastructure development while navigating challenges like raw material volatility. Businesses adopting eco-friendly innovations and strategic expansions will thrive. As environmental regulations tighten, the shift toward sustainable coatings will shape the industry’s future, ensuring resilience and competitiveness, with significant contributions to global economic and environmental goals.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)