Table of Contents

Overview

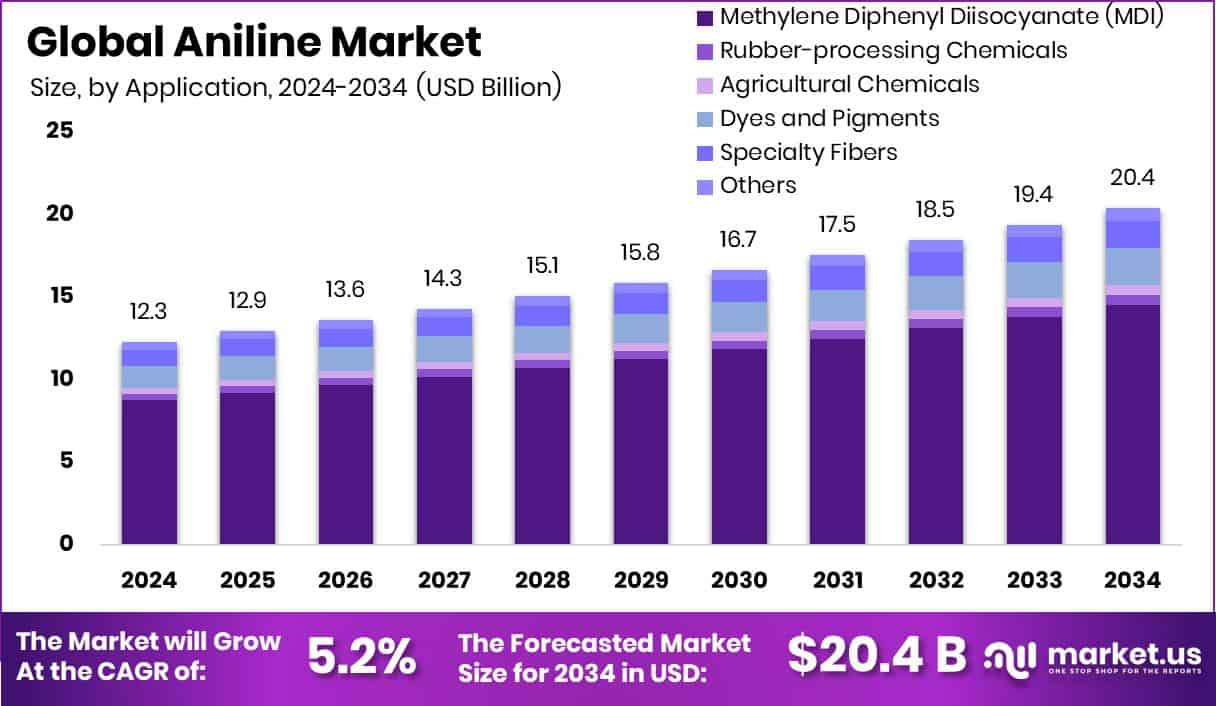

New York, NY – July 21, 2025 – The Global Aniline Market is projected to grow significantly, reaching USD 20.4 billion by 2034, up from USD 12.3 billion in 2024, with a steady CAGR of 5.2% from 2025 to 2034.

In 2024, Methylene Diphenyl Diisocyanate (MDI) commanded a 71.2% share in the By Application segment of the Aniline Market, driven by its critical role in producing polyurethane foams used in insulation, automotive seating, and furniture.

The Building and Construction sector led the By End-use segment of the Aniline Market with a 39.3% share, primarily due to the extensive use of aniline-derived MDI in rigid polyurethane foams for thermal insulation. Direct Sales dominated the By Distribution Channel segment of the Aniline Market with a 71.8% share. Large-scale industrial buyers, including chemical, automotive, and construction material producers.

Key Takeaways

- Global Aniline Market is expected to be worth around USD 20.4 billion by 2034, up from USD 12.3 billion in 2024, and grow at a CAGR of 5.2% from 2025 to 2034.

- The aniline market heavily relies on MDI production, which accounts for 71.2% of total application usage.

- The building and construction sector drives 39.3% of the aniline market demand through polyurethane-based insulation materials.

- Direct sales dominate the aniline market distribution, contributing 71.8% share due to bulk industrial procurement practices.

- Asia-Pacific accounted for a 44.2% share of the global Aniline Market in 2024.

How Growth is Impacting the Economy

The Aniline Market’s growth significantly influences the global economy, particularly in Asia-Pacific, where it supports industrial expansion. The surge in polyurethane production, driven by aniline, bolsters the construction and automotive sectors, creating jobs and increasing GDP contributions in countries like China and India. For instance, India’s textile sector budget increased, enhancing aniline demand.

However, price volatility and environmental regulations pose challenges, potentially raising production costs. Investments in infrastructure, such as Covestro’s bio-based aniline plant, stimulate economic activity while promoting sustainability. This growth fosters innovation, attracts foreign investment, and strengthens supply chains, though fluctuating raw material costs require strategic economic planning.

➤ Curious about the content? Explore a sample copy of this report – https://market.us/report/global-aniline-market/request-sample/

Strategies for Businesses

Businesses in the aniline market should prioritize sustainability by investing in bio-based production to meet environmental regulations and consumer demand. Forming strategic partnerships with R&D institutions can drive innovation in eco-friendly processes. Diversifying applications into pharmaceuticals and agrochemicals can capture emerging markets.

Companies should also optimize supply chains to mitigate raw material price volatility. Expanding production capacities in high-demand regions like Asia-Pacific, as seen with Sinochem’s increase, ensures market competitiveness. Leveraging data analytics for demand forecasting and adopting advanced catalytic processes will enhance efficiency and profitability, positioning firms to capitalize on the market’s projected growth.

Report Scope

| Market Value (2024) | USD 12.3 Billion |

| Forecast Revenue (2034) | USD 20.4 Billion |

| CAGR (2025-2034) | 5.2% |

| Segments Covered | By Application (Methylene Diphenyl Diisocyanate (MDI), Rubber-processing Chemicals, Agricultural Chemicals, Dyes and Pigments, Specialty Fibers, Others), By End-use (Building and Construction, Rubber, Consumer Goods, Automotive, Packaging, Agriculture, Others), By Distribution Channel (Direct Sales, Distributors/Wholesalers, Online Retailers, Specialty Stores, Chemical Supply Chains, Others) |

| Competitive Landscape | BASF Corporation, BONDALTI, Borsodchem Mchz, Covestro AG, Dow, GNFC, Huntsman International LLC, Jilin Connell Chemical Industry Co., Ltd., Mitsubishi Chemical, Mitsui Chemical, Petrochina Co. Ltd., Sabic, SP Chemicals Holdings Ltd., Sumika Bayer Urethane Co., Ltd., Sumitomo Chemical Co. Ltd., The Dow Chemical Company, Wanhua Chemical Group Co. Ltd. |

➤ Directly purchase a copy of the report – https://market.us/purchase-report/?report_id=151362

Key Market Segments

By Application Analysis

- In 2024, Methylene Diphenyl Diisocyanate (MDI) commanded a 71.2% share in the By Application segment of the Aniline Market, driven by its critical role in producing polyurethane foams used in insulation, automotive seating, and furniture. The expansion of the construction and automotive industries has significantly increased demand for MDI-based polyurethane, solidifying this segment’s dominance.

- The remaining 28.8% of the market comprises synthetic dyes, rubber processing chemicals, herbicide intermediates, and pharmaceutical precursors. While individually smaller, these segments collectively contribute significantly to aniline demand, supported by steady activity in the textile and agriculture sectors for dyes and herbicides.

- The MDI segment’s growth is fueled by rapid urbanization and infrastructure development, increasing the need for energy-efficient insulation materials. Additionally, the automotive sector’s shift toward lightweight, fuel-efficient vehicles further drives MDI applications.

By End-use Analysis

- In 2024, the Building and Construction sector led the By End-use segment of the Aniline Market with a 39.3% share, primarily due to the extensive use of aniline-derived MDI in rigid polyurethane foams for thermal insulation. Global surges in construction, fueled by urban development and energy-efficient building standards, have heightened demand for these foams.

- Polyurethane foams are favored in construction for their superior insulation, durability, and versatility in applications like walls, roofs, and piping. Growing emphasis on energy conservation and green building initiatives has further elevated aniline’s importance in this sector, with MDI-based materials playing a pivotal role in sustainable infrastructure.

By Distribution Channel Analysis

- In 2024, Direct Sales dominated the By Distribution Channel segment of the Aniline Market with a 71.8% share. Large-scale industrial buyers, including chemical, automotive, and construction material producers, prefer direct procurement from manufacturers to secure volume-based pricing, long-term contracts, and consistent product quality, particularly for aniline used in MDI production.

- Direct sales enable manufacturers to build strong customer relationships, offering customized logistics and enhanced service levels. This channel’s dominance reflects the market’s focus on industrial-scale applications and supply reliability.

Regional Analysis

In 2024, the Asia-Pacific region solidified its position as the leader in the global Aniline Market, capturing a 44.2% share with a market value of USD 5.4 billion. This dominance is fueled by robust industrial growth, booming construction, and strong demand from sectors like automotive, textiles, and agriculture. The increasing use of polyurethane foam for insulation and seating applications further bolsters the region’s market strength.

North America and Europe trail behind, leveraging their advanced chemical manufacturing capabilities. North America sustains consistent demand through its automotive and construction industries, while Europe emphasizes sustainable practices and regulatory compliance to promote greener aniline production.

The Middle East & Africa and Latin America are emerging markets with moderate growth, driven by infrastructure expansion and growing manufacturing sectors, though their contributions remain smaller compared to established markets. Asia-Pacific leads in both volume and revenue, supported by strong domestic consumption and export-driven production.

Recent Developments

1. BASF Corporation

- BASF has been focusing on sustainable aniline production using renewable energy and bio-based feedstocks. The company is investing in green aniline to reduce carbon emissions in polyurethane value chains. BASF’s Ludwigshafen plant is a key production hub, with ongoing R&D for eco-friendly processes.

2. BONDALTI

- Bondalti (part of José de Mello Group) is expanding its aniline derivatives portfolio for pharmaceuticals and agrochemicals. The company emphasizes high-purity aniline for specialty applications and has invested in process optimization for better efficiency.

3. BorsodChem MCHZ

- BorsodChem, under Wanhua Chemical, has increased aniline capacity in Hungary to support MDI production. The company is integrating circular economy principles by optimizing byproduct utilization in aniline synthesis.

4. Covestro AG

- Covestro is advancing aniline-based polyurethanes for the automotive and construction sectors. The company is piloting CO2-based aniline production as part of its sustainability goals, reducing reliance on fossil feedstocks.

5. Dow

- Dow is innovating in aniline derivatives for flexible foams and coatings. The company is collaborating on catalytic hydrogenation processes to enhance aniline yield and reduce environmental impact.

Conclusion

The Aniline Market’s growth reflects its vital role in industrial applications. Its economic impact, particularly in Asia-Pacific, drives job creation and innovation but faces challenges from price volatility and regulations. Businesses can thrive by adopting sustainable practices and expanding into new applications. Analysts foresee a bright future with technological advancements and green initiatives ensuring resilience. Stakeholders must navigate challenges strategically to leverage opportunities, ensuring the aniline market remains a cornerstone of industrial and economic progress.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)